Traditional search has evolved and changed. In 2025, the growth of generative AI, conversational interfaces, and multimodal tools is changing how people find and interact with information.

Legacy search engines are being challenged, not just by each other, but by AI-native platforms that answer questions directly, personalize results, and pull data straight from the web and internal systems.

This report explores the core trends driving this shift: from chat-based search to retrieval-augmented generation (RAG), and from enterprise knowledge tools to on-device assistants.

It also examines the emerging business models, regulatory pressures, and the growing role of AI in both consumer and enterprise search.

AI Search Industry Report: Key Trends and Innovations

1. Generative AI in Search

Search is just getting smarter. Microsoft’s Copilot Search (Apr 2025) combines web results with AI-generated summaries and source citations. Marketers are increasingly using ChatGPT SEO prompts to test content visibility and understand how their brand appears in AI-generated responses.

Google’s SGE, built on Gemini and tested in Search Labs, does the same.

Both companies have the same pitch: why make people click through five different websites when you can just give them the answer upfront?

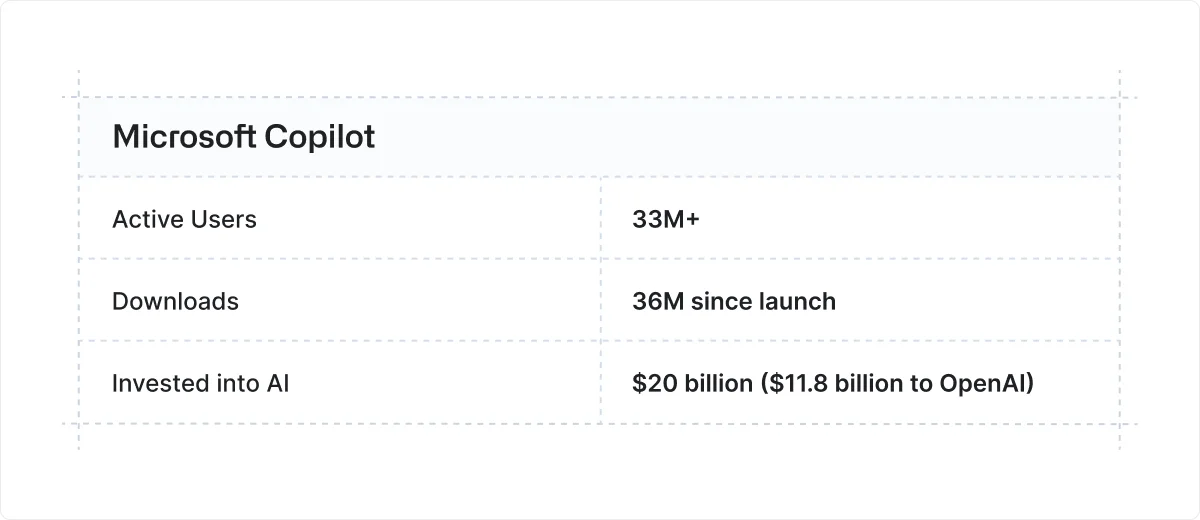

Here's where Microsoft stands right now:

The data on AI Overviews tells a story that's equal parts fascinating and terrifying for anyone who runs a website. Recent studies show AI Overviews are reducing click-through rates significantly.

Ahrefs reported a 34.5% drop in position 1 CTR when AI Overviews appear, while Amsive found an average 15.49% decline.

BrightEdge data reveals search impressions jumped 49% year-over-year, but click-through rates dropped 30%; users are getting answers without clicking through to original sources.

Think about that for a second. You could rank #1 in Google, and still watch your traffic evaporate because Google decided to answer the question for you.

Via Malte Landwehr, CTR is reduced by 37-40% when AI Overviews are present (showed by multiple studies from different SEO tools from January 2024 - May 2025)

However, AI Overviews are expanding rapidly, triggered for 6.49% of queries in January 2025, climbing to 7.64% by February (an 18% monthly increase).

The percentage continued to grow, hitting 13.14% by March (72% growth from the previous month).

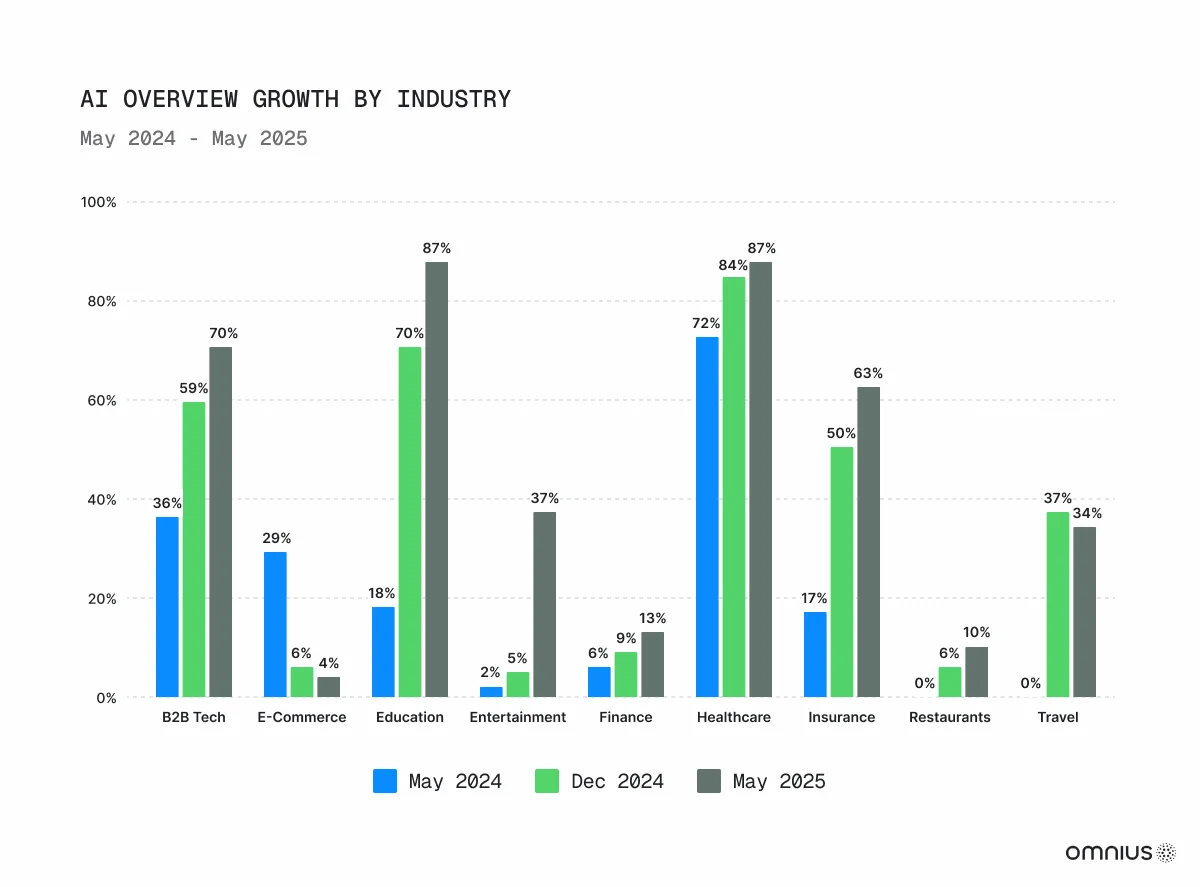

Here, you can see the AI Overview growth separated by industry (May 2024-May 2025):

This shift creates both challenges and opportunities: content creators face reduced traffic, but those who adapt their strategies to appear in AI citations can capture new visibility channels.

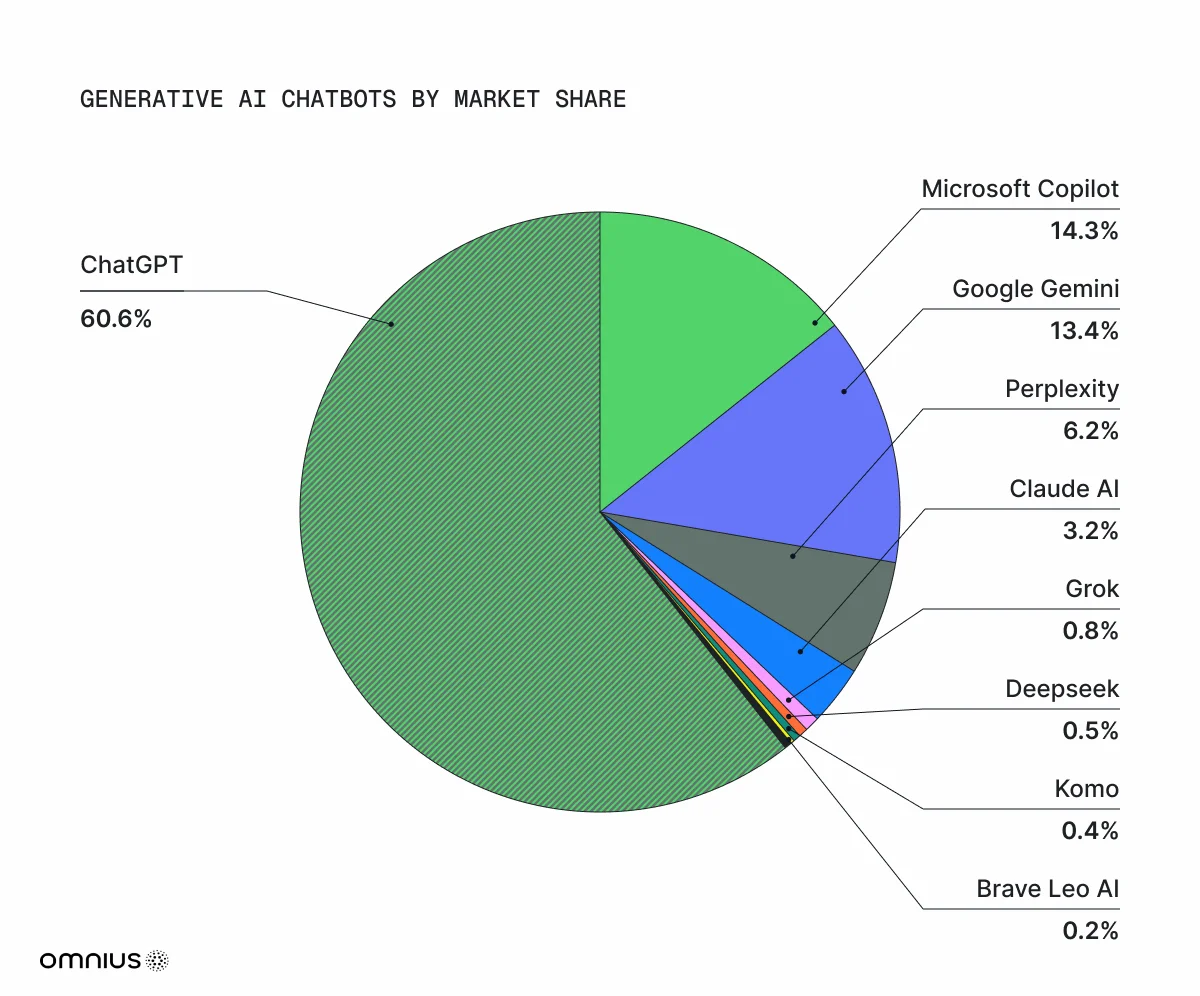

2. AI Chatbots as Search Tools

Search isn't just getting smarter, it's getting chatty. By late 2024, ChatGPT dominated with around 59 % of the generative chatbot market, while Microsoft Copilot and Google Gemini shared roughly 13-14 % each.

These tools now answer complex queries directly, often with source citations. Meanwhile, niche bots are carving out their own space:

Perplexity AI (≈ 5.5 %) prioritises concise factual answers, and Claude AI (≈ 2.8 %) delivers structured outputs tailored for business users. The chart below shows the data for June 2025:

3. Multimodal and Contextual Search

Google and Samsung are bringing multimodal AI to Galaxy devices. Models like Gemini Pro and Imagen 2 now power on-device features: image-based search, live camera queries, and summarization. Google’s SGE accepts image inputs and pulls real-time data, while context from user history personalizes results.

Text, voice, and image are converging; search is becoming more human.

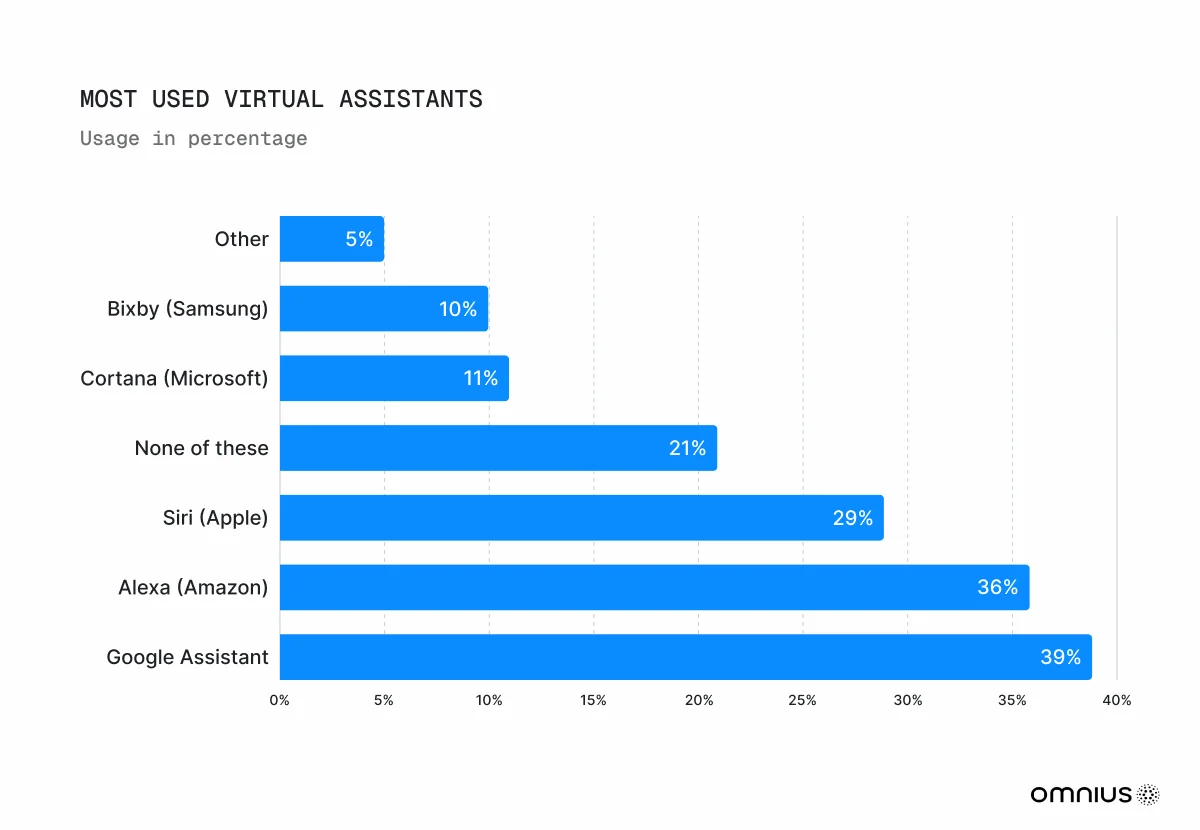

4. Voice and Conversational Interfaces

AI voice assistants are booming. By mid-2024, roughly 20 % of internet users were performing voice-based searches, and around 8.4 billion voice-enabled devices, smart speakers, phones, and cars, were in use globally, outnumbering people.

Smart speakers remain a growth engine - the market is projected to hit about $19 billion in 2025, up from $14.4 billion in 2024.

Systems like Siri, Alexa, and Google Assistant now use advanced language understanding to handle natural questions.

The rapid expansion of both usage and devices shows voice search has become a seamless part of daily life, reducing the need to even look at the screen.

The chart below shows that Google Assistant is the most used virtual assistant, just above the Alexa:

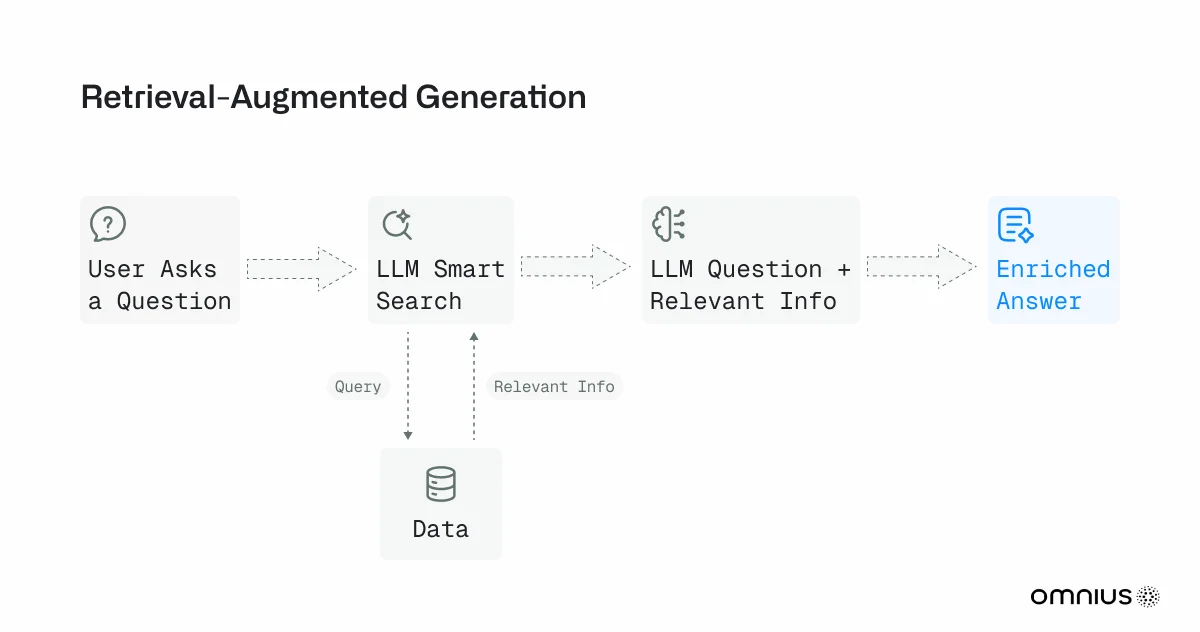

5. Retrieval-Augmented Generation (RAG)

A game-changer in AI search is Retrieval-Augmented Generation (RAG); LLMs first pull in real-time data, then generate answers grounded in up-to-date documents.

That solves the “knowledge cut-off” issue of standalone LLMs and enables transparent, source‑cited responses. When combined with in-app file keyword search for PDFs and spreadsheets, teams can access answers directly in one workspace while maintaining verification speed.

In enterprise settings, RAG powers AI agents to fetch internal policies, reports, and proprietary data on demand, dramatically reducing hallucinations and boosting reliability.

The result? Faster, more accurate answers rooted in real, verifiable sources.

Where the Market Stands - and Where It’s Headed

Search Engine Market Share

AI usage in both the US and Europe increased from Q1 2024 to Q1 2025, with ChatGPT being the most popular of the major AI platforms.

However, Google still dominates general search, claiming around 89.6% of global queries by May 2025, with Bing at ~4%, and Yandex, Yahoo, DuckDuckGo, Baidu, etc., making up the rest.

Its scale (default on Android, Chrome, and Workspace) keeps it ahead even as AI tools emerge.

What's interesting is that digital marketing and SEO-related topics may start driving more visitors from AI search to websites than from traditional search by early 2028, according to Semrush.

As search evolves, Google’s dominance isn’t disappearing, but it’s navigating new AI-driven terrain.

In the video below, you can see how some of the best AI companies drive growth:

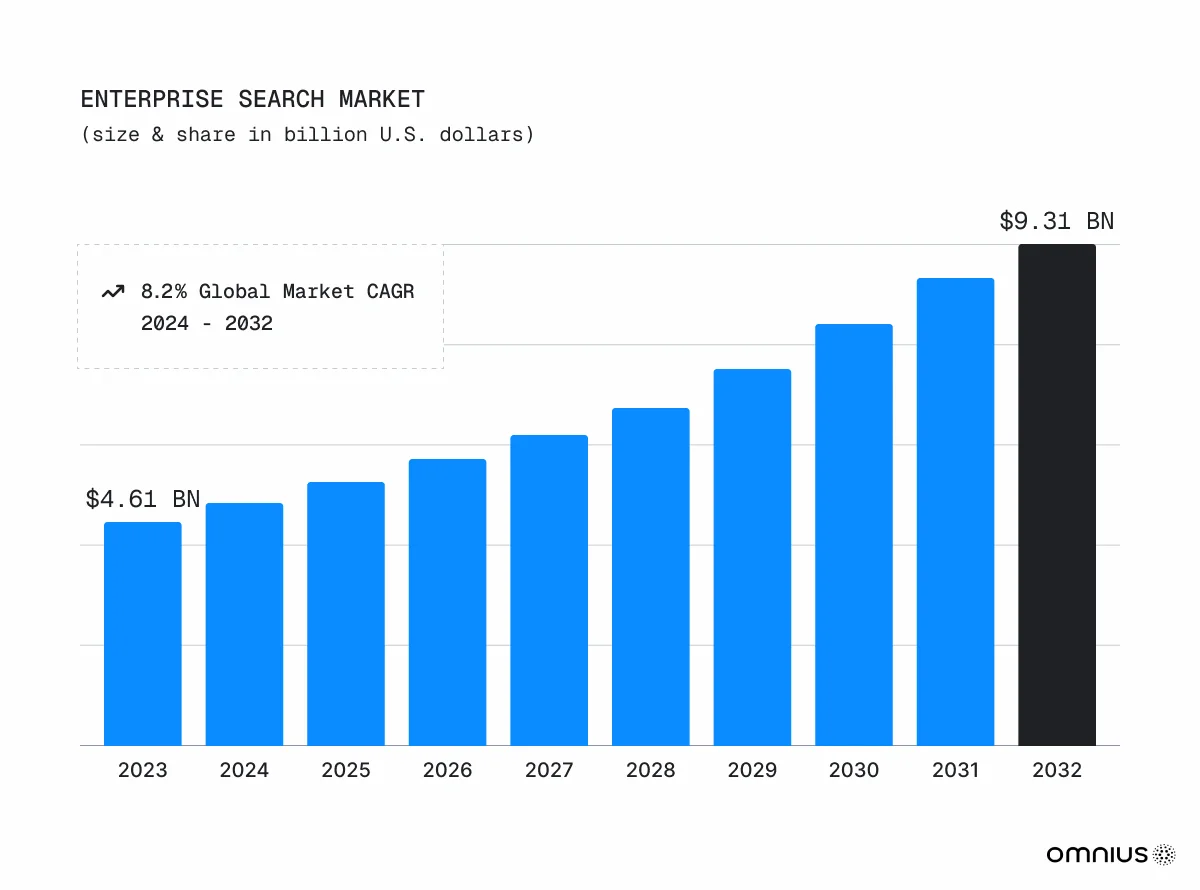

Enterprise AI Search Market

The enterprise search market, tools for internal document and knowledge discovery, is accelerating under AI. Valued at US $4.61 billion in 2023, it's projected to hit $9.31 billion by 2032, growing at a compound annual rate of about 8.2 %.

These platforms increasingly leverage AI/ML, including NLP and RAG (retrieval-augmented generation), to help teams locate reports and insights faster.

What this means is faster access to the right information.

Voice and Assistant Growth

The voice-assistant wave isn’t slowing. As of 2024, 149.8 million Americans used voice assistants, a number that grew about 2.5% year-over-year, and is projected to reach 153.5 million by 2025.

This supports investment in conversational AI search on mobile and smart-home platforms.

Also, we can already see some implementations, from AI voiceovers at the top of blog posts (like those created with ElevenLabs) to hands-free search in cars or Android-based home hubs.

Brands are starting to design “spoken UX” where searching, navigating, and even purchasing are triggered by voice.

Investment and Adoption

Venture capital is flooding into AI-driven search startups.

You.com raised $50 million in a Series B round in 2024, bringing its total funding to $99 million.

Perplexity AI soared to a $9 billion valuation after a $500 million round in December 2024, and is reportedly targeting an $18 billion valuation by 2025.

On the enterprise side, many large companies are piloting or deploying AI search tools built on RAG to streamline internal knowledge discovery, though only about 30 % of AI prototypes reach production.

And broader forecasts suggest the generative AI market could hit tens of billions by mid-decade.

In short: cash, innovation, and real-world rollout are all converging in AI search.

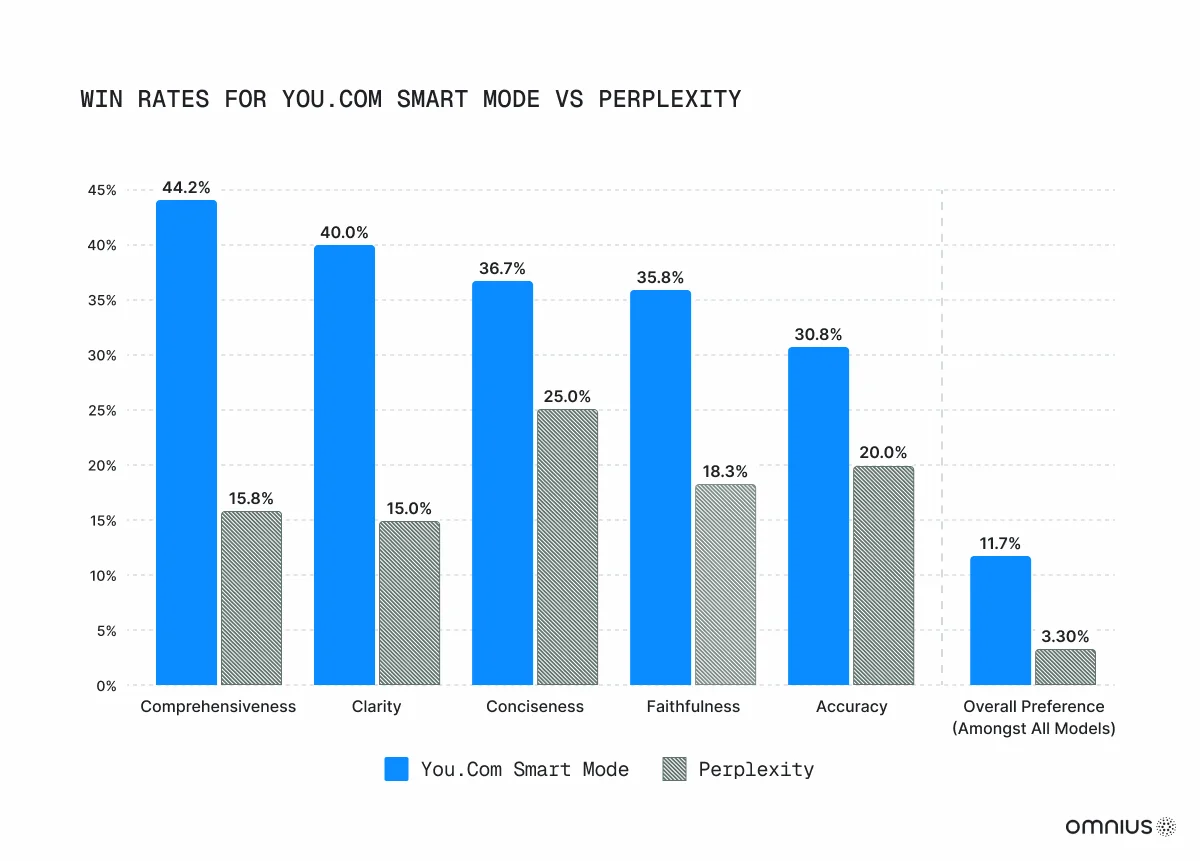

The graph below from You.com resources (2024) shows that their Smart Mode outperforms Perplexity across all evaluation metrics:

Inside the AI Search Race

Major Players – Tech Giants

Google and Microsoft remain the cornerstones of AI-powered search. Google is heavily investing in Gemini and its SGE experience, integrating its LLMs (Bard/Gemini) across Search, Cloud, and Workspace.

Microsoft, through its OpenAI partnership, has baked GPT‑4/ChatGPT into Bing (Copilot Search), Microsoft 365, and Azure.

Both giants leverage vast data and infrastructure to power their AI search offerings.

In Asia, regional players are following suit; China’s Baidu with ERNIE Bot and South Korea’s Naver with CLOVA AI/HyperCLOVA X are building out local generative search services.

AI-First Search Startups

New entrants are reshaping AI-powered search.

ChatGPT acts as an “answer engine” within Microsoft’s ecosystem, while Perplexity , handling hundreds of millions of monthly queries (780 M in May 2025), prioritizes accuracy and commands a high valuation. Many users now look for an alternative of ChatGPT to improve their AI workflow.

You.com labels itself as a productivity engine, not just links. Anthropic’s Claude 3, aimed at enterprise users, has added web search capabilities across all plans.

Niche players are gaining traction too: Phind focuses on code, Andi delivers simple answers, and embedding‑search startups are emerging.

In some corners, observers even see Perplexity and ChatGPT as Google’s biggest challengers.

Enterprise Search Vendors

In the business segment, traditional search/platform companies are integrating AI. Firms like Algolia, Coveo, Elastic, and Lucidworks are all weaving in AI capabilities.

Startups like Glean and Squirro focus on RAG and knowledge‑graph approaches to power internal knowledge discovery. Legacy systems (including Oracle Endeca, IBM Watson Discovery, and Google Cloud Search) have been modernized with NLP and ML.

A standout move: Snowflake acquired Neeva in May 2023 for about $150 million, aiming to inject AI search into its data cloud.

Long story short: across platforms old and new, AI is turning enterprise search into smarter, faster knowledge engines.

Consumer and Enterprise Applications

Consumer Web & Mobile Search

Every day, users encounter AI-enhanced search interfaces. In Google and Bing, AI-generated summaries (like “AI Overviews” and Copilot snippets) now top the results page, with traditional links below.

Most smartphones now ship with built‑in AI assistants. Samsung’s Galaxy S24 introduced “Galaxy AI,” powered by Google’s Gemini, offering on‑device summarization, image, and voice search via features like Circle to Search, Browsing Assist, and Live Translate.

Meanwhile, chatbots like ChatGPT and Gemini are doubling as search portals; users type queries and receive paragraph answers with sources. Even e‑commerce and content platforms now embed AI suggestions and Q&A bots in their search UIs.

Enterprise Knowledge Management

Employees spend ~1.8 hours per day (≈9.3 hours/week) searching for internal information, meaning nearly 20% of their work hours are spent looking for answers.

RAG-powered “search assistants” are transforming how companies tap into internal data. These systems let employees pose natural-language queries (like “current capital requirements”) and receive answers drawn from up-to-date documents, complete with citations for clarity and trust.

Platforms such as Microsoft 365 Copilot and Salesforce Einstein GPT connect directly to corporate sources, SharePoint, CRM, Slack, grounding responses in real enterprise knowledge.

The result: faster, more accurate, and reliable internal search that seriously cuts down your time lost chasing answers.

Customer Support and CRM

Around 90% of customers expect instant support, according to HubSpot.

AI chatbots now dominate customer service, using semantic search to pull from FAQs and manuals for instant support. Modern bots maintain conversational context, and companies rely on generative AI to draft knowledge-base articles and summarize support tickets.

The result: faster resolutions, smarter bots, and leaner support workflows.

Vertical Search Solutions

Specialized AI search applications are emerging in fields like legal, medical, and tech.

For example, Phind is tailored for developers, delivering rich, interactive answers and code snippets on technical queries; Neeva (now under Snowflake) was aimed at providing ad-free personalized search for professionals; and services like Amazon Alexa for shopping use natural-language understanding to guide purchases. Enterprises in R&D and pharma employ AI agents to mine scientific literature.

These vertical tools often combine search, Q&A, and AI summarization to streamline research workflows.

Challenges and Opportunities

1. Hallucinations & Accuracy

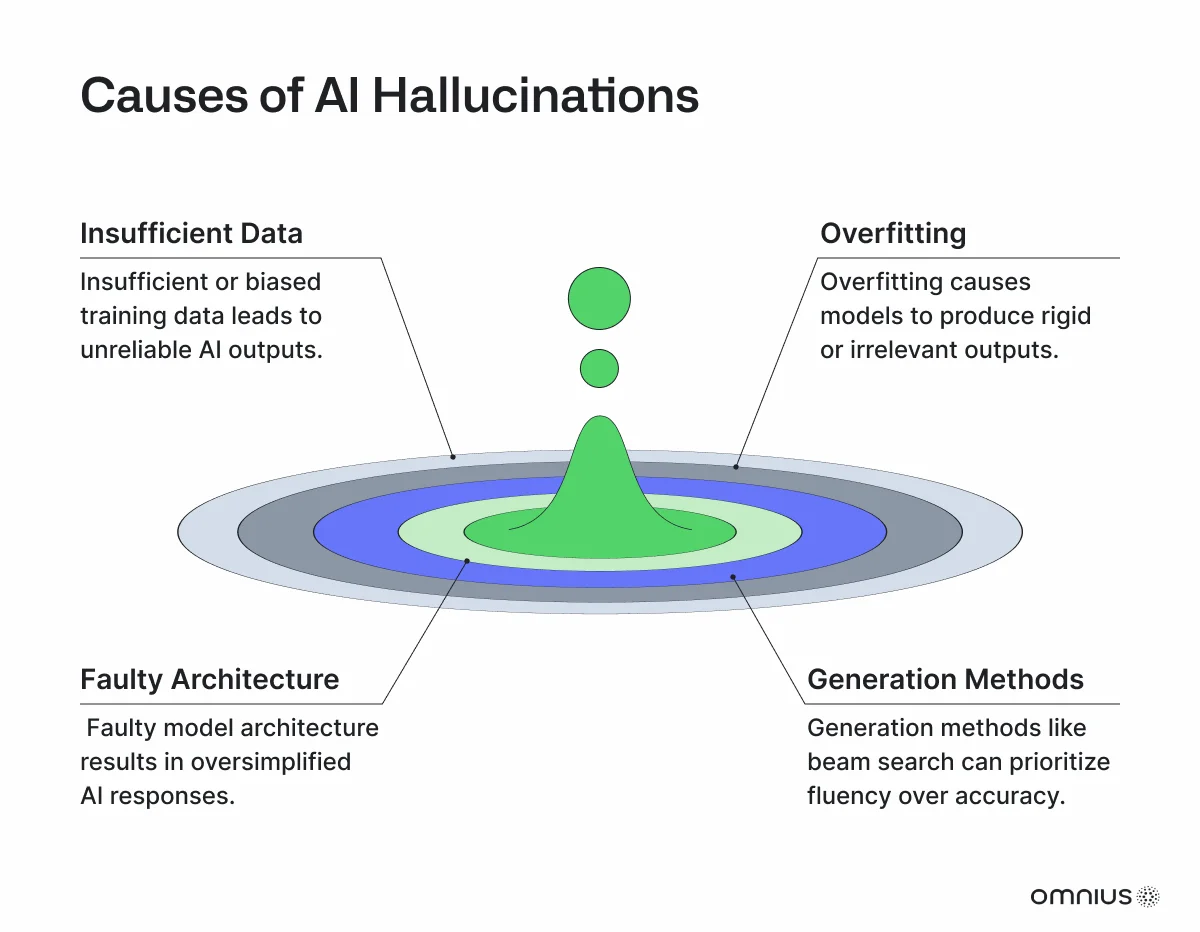

Now this is a problem. Generative search can “hallucinate”, confidently producing incorrect or misleading information.

Ensuring factual reliability is a major concern. Companies are experimenting with citation tracing and fact-checking layers.

The need for human oversight remains in critical domains.

This challenge also represents an opportunity: improving source attribution (as in Bing Copilot’s cited answers) can build user trust.

2. Bias and Fairness

AI models inherit biases from training data, risking discriminatory or harmful outputs.

Ethical deployment demands guardrails (technical, procedural, and regulatory) to detect and correct bias.

Regulators (like the FTC and lawmakers behind AI civil‑rights proposals) are pressing for accountability and fairness .

At the same time, companies are funding bias‑mitigation research, making model audits, fairness constraints, and post‑training checks standard practice.

In short, bias is real, but it’s now one of the most actively addressed challenges in AI search.

3. Privacy and Data Use

Generative AI demands massive data, and that exposes a serious privacy weak spot.

In December 2024, Italy’s data protection authority hit OpenAI with a €15 million fine for processing personal data without consent and failing to verify user age, marking one of the first major GDPR enforcement actions against a generative AI developer.

Compliance with GDPR and other privacy laws remains a key hurdle, and companies face increasing pressure to secure and manage user data from personalized search.

The overshare risk isn’t just legal, it's a make-or-break trust issue in AI adoption.

4. Regulatory & Legal Issues

Governments are entering the AI search market.

In the U.S., the Justice Department sued Google for search monopolization; in August 2024, a judge ruled Google illegally exploited its dominance.

Meanwhile, Europe is preparing its heavy artillery: the EU AI Act, effective 2026, will force providers to disclose when users interact with AI, label deepfakes, and add transparency layers to generated content.

These regulations aren't minor tweaks; they may reshape how AI search features are shown, used, and monetized.

5. Monetization Strategies

Search has always been driven by ads, but how that translates into AI-powered interfaces is still unfolding.

Microsoft already embeds Bing ads directly into Copilot chat responses, displaying relevant sponsored content even within conversational replies, and is now fine-tuning when and how those ads appear based on user context .

Startups like You.com and Perplexity have launched freemium tiers; free access with optional paid upgrades (~$20/month) and team or enterprise plans.

On top of that, platforms like Microsoft are bundling “AI services” into enterprise suites like Copilot for M365 and Azure.

The real question: how to monetize and rank on AI search without eroding trust, or turning every answer into an ad puppet.

6. Infrastructure & Cost

Cloud-scale AI search demands massive compute power, and major cloud providers (AWS, Azure, Google Cloud) are racing to deploy LLM-optimized hardware and lower inferencing costs by partnering with chip leaders like NVIDIA .

These alliances unlock access to powerful GPU instances (e.g., NVIDIA Blackwell chips) hosted in data centers, easing the cost burden of running AI at scale.

Beyond cloud, innovation is pushing models on-device to slash latency and enable offline experiences, while inference-only, serverless platforms reduce idle GPU waste and lower barriers for startups. For those looking to manage costs, many cloud providers offer incentives, and you can often find a good deal with an AWS credits promo code.

The bottom line: fuel for generative search comes at scale, requires heavy compute, new hardware stacks, and smarter deployment strategies.

Competitive Dynamics

The AI search space is heating up across partnerships, acquisitions, product launches, and market movement, with incumbents and challengers all staking their claims.

Partnerships

- Google + Samsung: Gemini AI now powers on-device features across Galaxy phones, bringing image and voice search straight to users' pockets.

- Microsoft + OpenAI: Deep integration of ChatGPT/GPT‑4 across Bing, Office, and Azure continues to strengthen Microsoft’s AI search foothold.

- Enterprise data platforms: Companies like Databricks and Snowflake are integrating AI search into their ecosystems (e.g. collaborating with Voyage AI in 2025), signaling a push toward AI‑native data tools.

Acquisitions

- Shopify acquired Vantage Discovery in March 2025 to strengthen its e‑commerce search via AI, part of a broader spree of small AI acquisitions.

- Rumors swirl around Big Tech interest in startups like You.com and Perplexity, though no public deals have closed.

Product Launches

- Microsoft’s Copilot Search went live in April 2025, blending generative answers with clear source citations.

- Google rolled out AI Overviews and continues to test new SGE capabilities in Search Labs.

- Anthropic updated Claude early in 2025 to include web-search integration.

- Niche players like Phind and Perplexity launched high-precision developer and enterprise search APIs in the same period.

- OpenAI plans to release its own AI-powered web browser.

Market Share Shifts

- While Google remains the dominant force, AI chat usage is nudging user behavior. Bing saw modest share increases after ChatGPT integration.

- AI-powered tools currently claim around 6% of search traffic, with projections suggesting this could surpass 10-14% by 2028.

- High-interest events (like the 2024 U.S. elections) trigger spikes in AI search activity, testing both capacity and relevance.

- At Google’s I/O 2025, new Gemini and Workspace AI updates highlighted how legacy search products are evolving in response. Google's I/O 2025 revealed that AI Overviews now reach 1.5 billion monthly users across 200 countries, making it the largest generative AI deployment globally. The company launched several key search innovations: AI Mode rolled out nationwide in the US, replacing traditional web results with computer-generated answers for complex queries, while new agentic capabilities arrived in Chrome and Search, including Agent Mode in the Gemini app. Google also integrated Imagen 4 and Veo 3 across its search ecosystem, pushing multimodal capabilities deeper into everyday queries. These moves signal Google's recognition that search is shifting toward conversational, AI-first experiences, even as competitors like ChatGPT and Perplexity gain ground.

Search Behavior Tracking: Beyond Traditional Metrics

Companies are discovering that standard search metrics: clicks, bounce rates, and session duration, need complete rethinking in an AI-first world.

For questions triggering AI Overviews, organic CTR dropped, forcing businesses to track new signals: citation rates in AI responses, brand mentions within generated summaries, and user satisfaction with AI-provided answers.

Forward-thinking organizations are measuring "answer attribution", how often their content appears as sources in AI responses, alongside traditional search rankings.

The shift requires new analytics frameworks that account for value delivered through AI citations rather than direct website visits.

The evolution extends beyond basic metrics into specialized optimization disciplines:

- AEO (Answer Engine Optimization) services helps content appear in featured snippets and voice searches.

- GEO (Generative Engine Optimization) services ensures content gets cited in AI responses, and

- AIO (AI Overviews) optimization targets Google's generative search results.

Analysis of 8,000 AI citations reveals that AI engines favor specific, deep pages over homepages, with 82.5% of citations linking to deeply nested content. Product-related content dominates AI citations, making up 46% to 70% of all sources referenced across AI search engines.

To understand data coming from LLM search engines, try Atomic.

With Atomic, you can track the behaviour of users coming from ChatGPT, Perplexity, and other generative engines, and analyze which pages capture AI traffic and how it converts.

The Future of LLMs and AI Search

With GPT-5, OpenAI emphasized that the next generation of large language models is built around retrieval and reasoning rather than pure memorization. Instead of depending solely on what they were trained on, modern systems like ChatGPT, Perplexity, and Gemini are designed to incorporate external information, verify it, and ground their responses in reliable sources.

That makes SEO more critical than ever.

If your content isn’t crawlable, structured, and trusted, reasoning models simply won’t find it. The future of visibility now depends on how well your website communicates meaning to both humans and machines.

In this video, we explain how the move to reasoning-first AI changes discovery, credibility, and visibility - and why SEO becomes the foundation of the reasoning web.

Conclusion

As search starts being shaped by AI, voice, and contextual intelligence, the road ahead is filled with both complexity and promise. Established players are retooling their platforms, startups are racing to redefine user experience, and enterprises are rethinking how knowledge flows within their organizations.

The opportunity is massive: companies that master AI-driven search early will capture better insights, streamline operations, and bypass competitors in serving both users and customers. But winning requires more than just new tools; it demands strategic thinking, flawless execution, and deep knowledge of what's actually changing.

That’s where Omnius comes in. We help companies navigate the evolving search ecosystem with content strategies designed for impact, backed by data, tailored to your audience, and built to scale.

Contact us to explore how we can help you stay ahead in 2025 and beyond, with tailored strategies that turn emerging search trends into real results.

Keep Learning

Fintech Industry Report 2024: Trends, Insights & Market Analysis

SaaS Industry Trends Report 2024: A Comprehensive Overview

GEO Industry Report 2025: Trends in AI, LLM Optimization & Regional Search Growth

.png)

.svg)

.svg)