This report reviews the fintech industry across ten dimensions: major media events, structural trends, market leaders, fastest-growing companies and categories, investment and M&A activity, geographic segmentation, and marketing strategy. All data and analysis are drawn exclusively from 2025 industry reports, company filings, and primary research.

Biggest Media News in the Fintech Industry in 2025

1. US Passes First Comprehensive Crypto Law: The GENIUS Act

On July 17, the United States enacted the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, its first-ever federal law governing cryptocurrencies. This landmark legislation provided a clear legal framework for stablecoin issuers, requiring them to be regulated institutions and hold 1:1 reserves, a move that immediately catalyzed institutional investment.

2. EU’s MiCA Regulation Goes Live, Triggering Bank Entry into Crypto

The European Union’s Markets in Crypto-Assets Regulation (MiCA) came into full effect at the start of the year, creating a harmonized, pan-European regulatory landscape. The clarity prompted the immediate entry of major European banks into the crypto market, with over 90 firms receiving licenses by year-end.

3. The Fintech IPO Window Reopens with Circle’s Landmark Debut

After a multi-year drought, the fintech IPO market roared back to life, led by the landmark public offering of USDC-issuer Circle, which raised $1.2 billion. The successful,

oversubscribed IPO was a major signal of renewed investor confidence in the digital asset space.

4. Klarna Goes Public in the Most Anticipated Fintech IPO of the Year

Klarna debuted on the New York Stock Exchange at a $19.65 billion valuation, raising $1.37 billion. The IPO was the most anticipated fintech listing in years, and its success validated the profitability of the BNPL model at scale.

5. Chime’s Successful IPO Validates the Neobank Model

In a major win for the consumer fintech sector, Chime went public in a successful IPO that raised $864 million. The offering was seen as a critical validation of the digital banking model at scale, proving its viability to public market investors.

6. Global Payments Acquires Worldpay for $24.25 Billion

In a deal that fundamentally reshaped the payments landscape, Global Payments announced its acquisition of competitor Worldpay for $24.25 billion. The move created a

pure-play merchant solutions powerhouse and was the defining M&A transaction of the year in the payments sector.

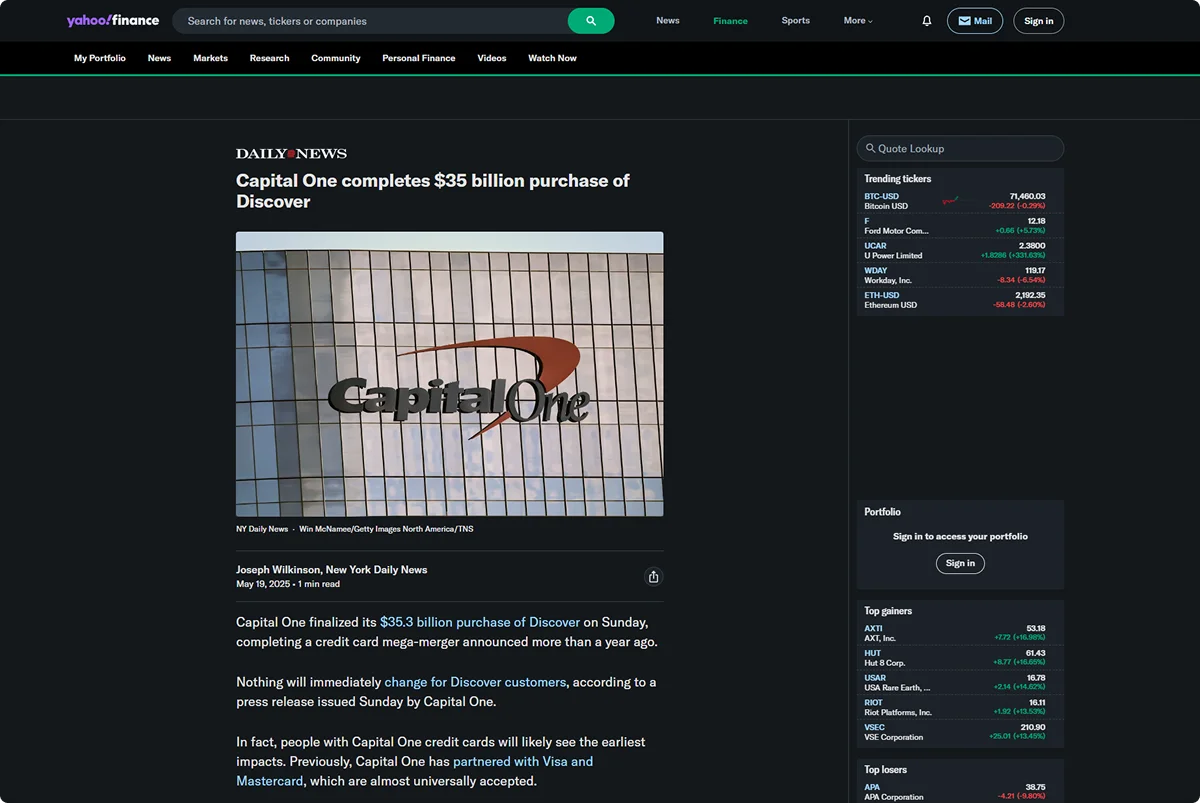

7. Capital One Completes $35.3 Billion Acquisition of Discover

The banking world was reshaped by the completion of Capital One’s $35.3 billion acquisition of the Discover payment network. The deal was the largest US bank merger in over a decade and positions a retail bank to compete directly with Visa and Mastercard for the first time.

8. Revolut Secures Full UK Banking License

After a multi-year application process, European fintech giant Revolut was finally granted its full UK banking license. The news was a pivotal moment for the neobank sector, transforming one of its largest players into a fully chartered bank and signaling a new era of competition with incumbents.

9. Binance Secures Record-Breaking $2 Billion Investment

In the largest single investment ever made in a crypto company, Binance secured a $2 billion funding round from Abu Dhabi’s MGX. The deal was a massive vote of confidence in the world’s largest crypto exchange and in the digital asset market as a whole.

10. PayPal Files for US National Bank Charter

Signaling a major strategic shift, PayPal officially filed an application for a US national bank charter. This move, if approved, would transform the payments giant into a regulated banking institution, further blurring the lines between fintech and traditional finance.

11. Deutsche Bank Joint Venture Launches First MiCA-Compliant Stablecoin

A consortium including Deutsche Bank’s DWS launched AllUnity, the first euro-denominated stablecoin to be approved under the EU’s new MiCA framework. The event marked a significant milestone for the institutional adoption of tokenized assets in Europe.

General Trends of the Fintech Industry in 2025

If the period from 2022 to 2023 was a time of reckoning for the fintech industry, marked by valuation resets and business model stress tests, then 2025 was a year of rehabilitation and maturation. The industry demonstrated it could grow profitably, operate under serious regulation, and integrate meaningfully with the broader financial system. This section details the key structural trends that defined this transformative year.

1. The Primacy of Profitability

The most consequential, if least glamorous, trend of 2025 was the industry-wide pivot from a “growth-at-all-costs” mindset to a focus on sustainable profitability. After the evaporation of cheap venture capital, profitability became the primary mechanism for sustaining growth. This was reflected in a notable decrease in cash burn for VC-backed fintechs and a higher revenue bar for companies raising capital. The successful IPOs of newly profitable companies like SoFi and the eightfold profit increase reported by UK neobank Monzo were landmark events that underscored this shift. The clear message from the market was that proven unit economics had replaced speculative potential as the price of admission for growth capital.

2. The Operationalization of Agentic AI

In 2025, artificial intelligence graduated from a product feature to the operational backbone of the industry. The defining technological transition was the move from generative AI as a simple chat interface to agentic AI as an end-to-end workflow engine. Enterprise spending on generative AI alone reached $37 billion, a more than threefold increase from 2024, with a clear focus on acquiring ready-made solutions. In a significant market shift, Anthropic emerged as the new enterprise leader, capturing 40% of enterprise LLM spend. These systems were deployed for loan underwriting, real-time fraud detection, and automated compliance checks, creating a structural cost advantage for early adopters.

3. The Maturation of Embedded Finance

Embedded finance, the delivery of financial services within non-financial products, crossed the threshold from pilot programs to a dominant platform strategy in 2025. The market for embedded banking revenue surpassed 230 billion, with B2B embedded payments projected to hit 2.6 trillion in transaction value in 2026. A key development was the “ERP invasion,” where enterprise software began offering embedded financial services, creating a severe competitive threat to standalone fintech lenders. However, the trend was not without its challenges; the underlying BaaS layer showed signs of stress, with providers like Railsr and Solaris facing financial and regulatory difficulties, adding a cautionary note to the sector’s rapid growth.

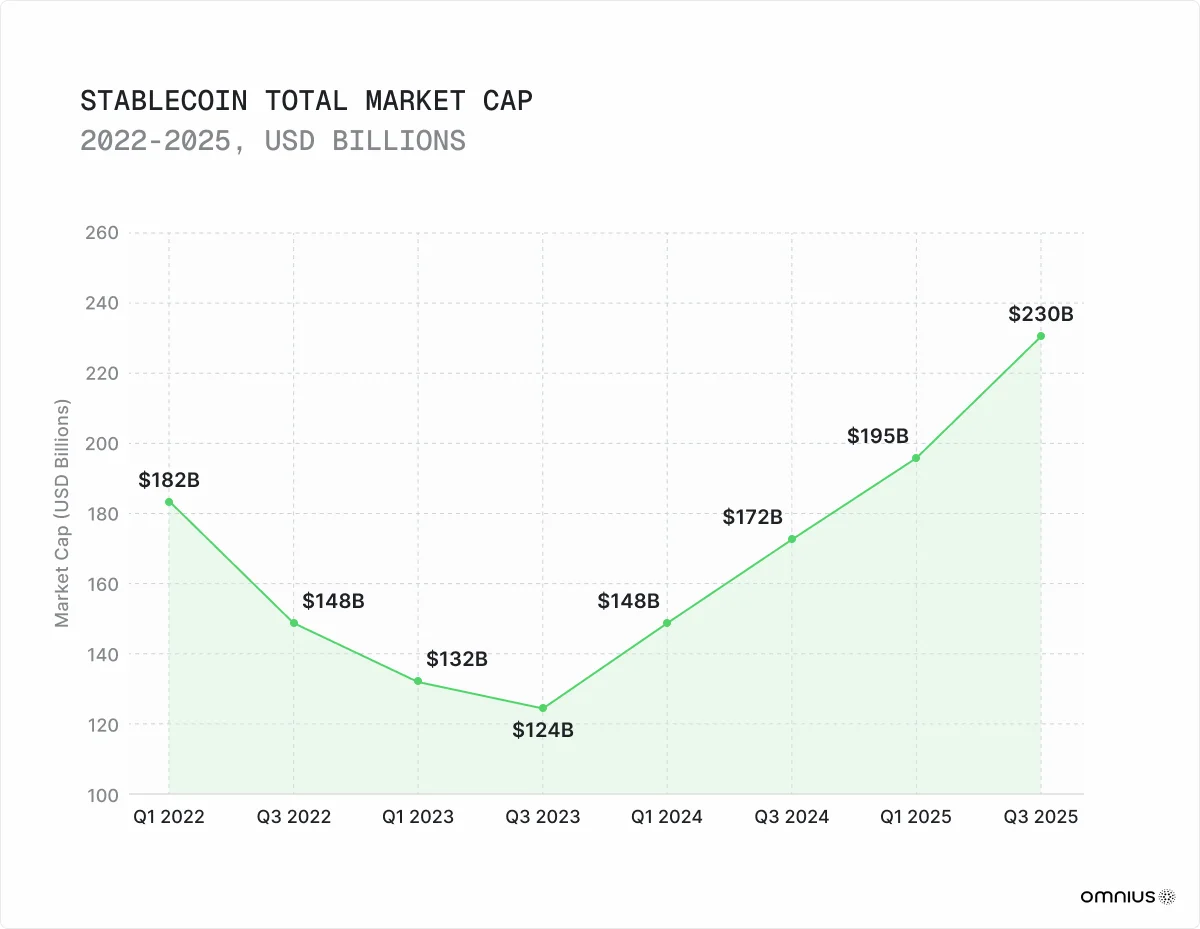

4. Stablecoins as a Core Settlement Layer

The narrative surrounding stablecoins fundamentally shifted in 2025, from a crypto-native speculative tool to institutional-grade financial infrastructure. This was driven by the establishment of clear regulatory frameworks in the US (GENIUS Act) and the EU (MiCA). With a market capitalization reaching 306 billion daily transaction volumes reaching approximately 30 billion, stablecoins demonstrated their utility as a real-world settlement layer.

The decision by payments giant Stripe to support stablecoin rails across more than 100 countries was a clear signal that the asset class had arrived as a foundational element of modern payments.

5. The Globalization of Real-Time Payments

Instant payment infrastructure expanded significantly in 2025, becoming the baseline expectation globally. Over 70 countries implemented real-time payment systems, and the full migration to the ISO 20022 standard for international wires was completed. The Clearing House’s RTP network in the US reported a 405% increase in transaction value, a striking indicator of adoption. A key innovation was the rise of Request for Payment (RfP), a feature making account-to-account (A2A) payments as seamless as card transactions, posing a significant long-term challenge to the interchange-fee-based models of traditional card networks.

6. The Convergence of Fintech Platforms

The traditional, vertically-defined categories of fintech became obsolete in 2025 as the dominant companies in each sector expanded horizontally to create multi-product “super apps.” Payments processors like Stripe and Adyen moved into banking and lending, while neobanks like Revolut expanded into asset management and insurance. This convergence has led to increased competition and margin compression in every vertical, as platforms with direct customer relationships and rich behavioral data can acquire new customers for adjacent services at virtually zero cost.

7. Financial Inclusion in Emerging Markets

Fintech continued to be a powerful engine for financial inclusion in emerging markets, where AI and mobile money drove unprecedented access to credit for underbanked populations. AI-driven ecosystems allowed these markets to bypass traditional financial infrastructures, offering scalable solutions for mobile-first users. This led to explosive growth, with Nigeria’s fintech industry growing by 70% in 2024 and Indonesia seeing a 226% surge in digital transaction volume.

8. The Rise of AI-Driven Cybersecurity

The year 2025 marked a turning point in the fight against financial crime, as the exponential rise of AI-driven deepfake fraud rendered human detection ineffective. With the volume of deepfake files projected to surge to 8 million, financial institutions were forced to shift rapidly towards advanced AI-powered defenses and robust biometric authentication. Liveness detection and voice biometrics became critical tools, and the remote identity verification (IDV) and Know Your Customer (KYC) processes at the digital front door became the primary battleground against increasingly sophisticated fraud attempts.

Biggest Players and Fintech Market Division in 2025

The global fintech market demonstrated robust growth and dynamic shifts in 2025, reaching 320 billion and a valuation between 395 billion, with projections of a 15-18% compound annual growth rate (CAGR) that would see it surpass $1.1 trillion by 2032. Serving over 2.5 billion users worldwide, the industry has firmly transitioned from a disruptive challenger to foundational infrastructure for global commerce and finance. The competitive landscape in 2025 was characterized by the continued dominance of established financial and technology giants, the rapid ascent of innovative startups, and a significant wave of consolidation and strategic partnerships.

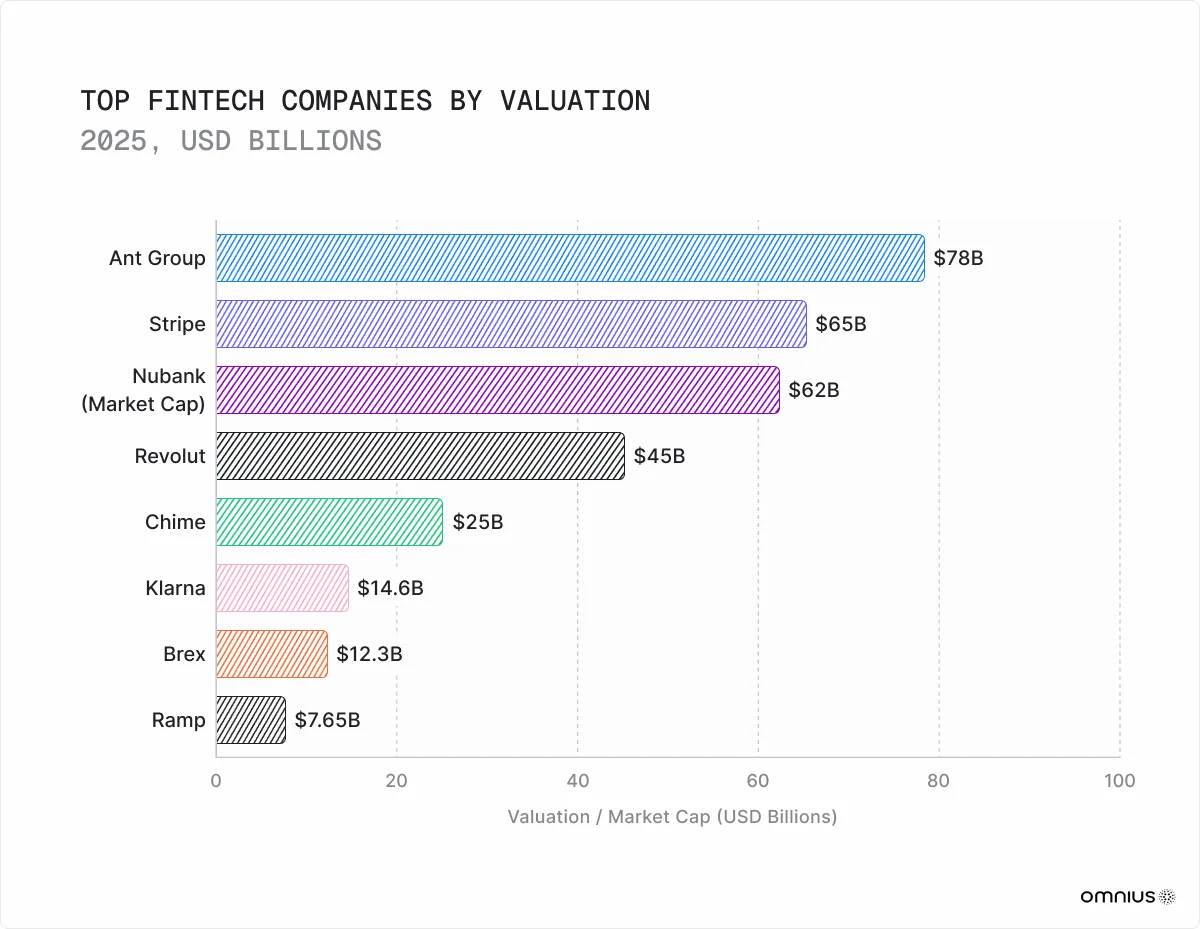

The Titans of Fintech: 2025’s Leading Companies

The year was dominated by a mix of publicly traded giants and high-growth private companies. US and Chinese firms collectively held nine of the ten most valuable fintech positions globally. The following table presents a synthesized list of the top 15 players who defined the industry in 2025.

Market Division: A Segment-by-Segment Analysis

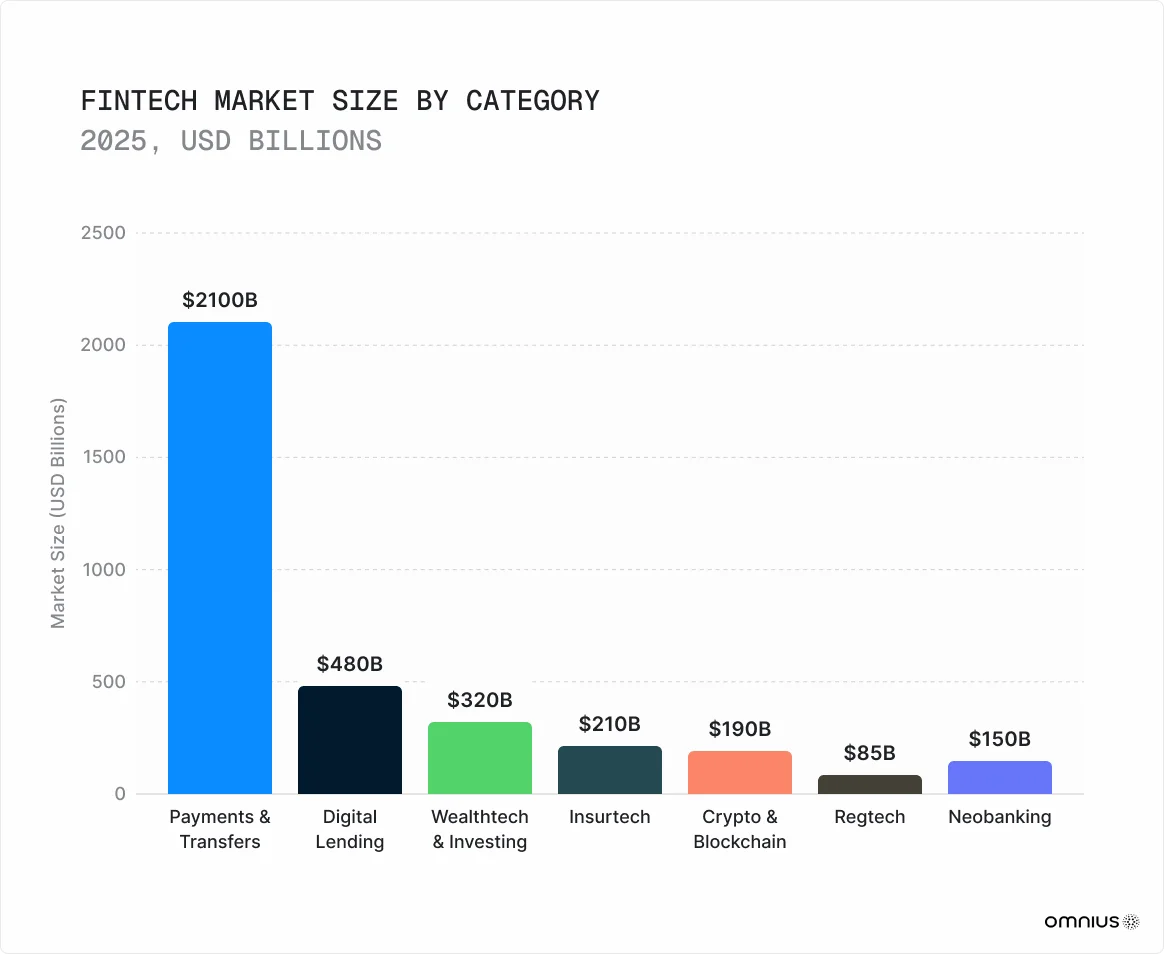

Digital Payments and Payment Processing remained the cornerstone of the fintech industry, accounting for over 45% of global revenue. The scale is immense, with Visa processing 15.7 trillion, Mastercard over 9 trillion, and PayPal $1.68 trillion in annual transaction volumes.

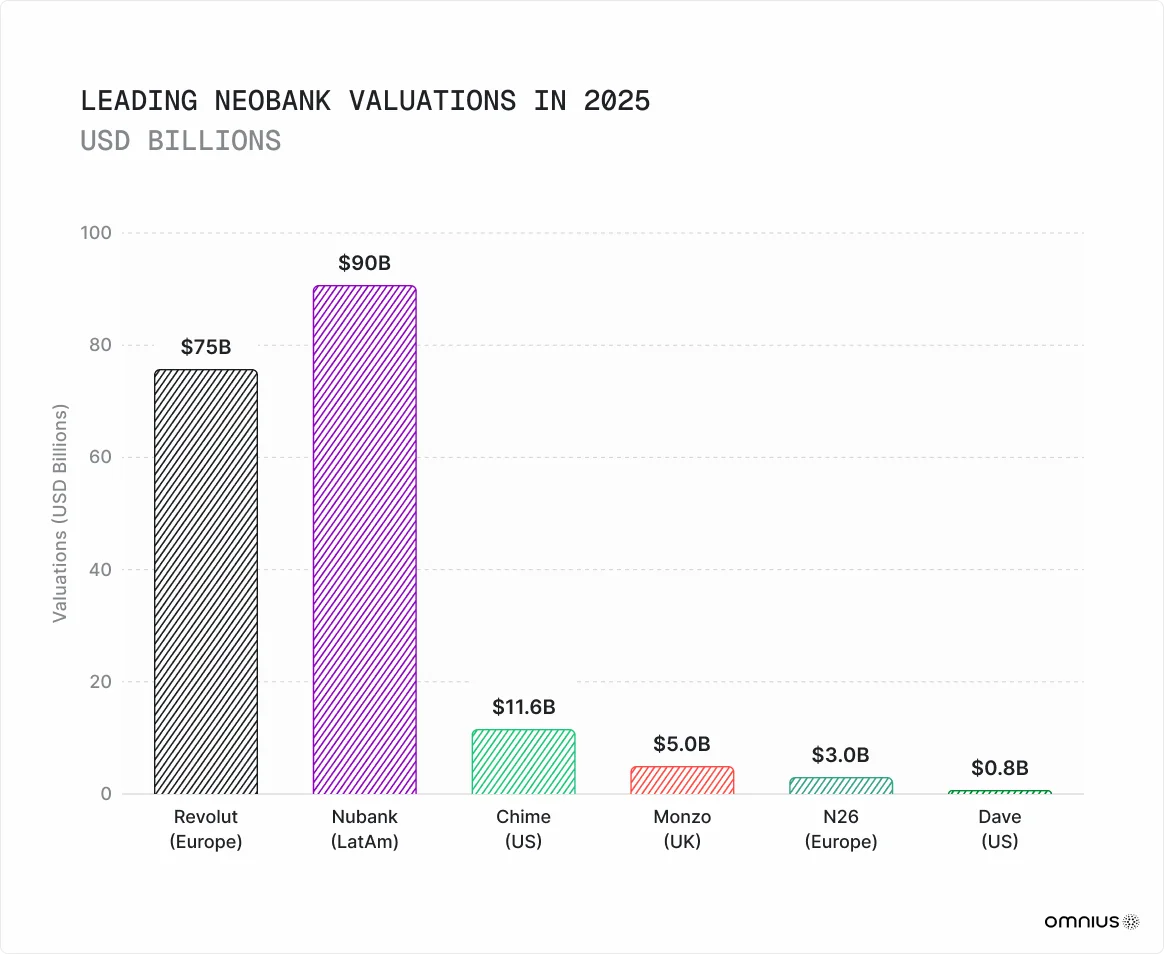

Neobanks and Digital Banking, with a market size of over 230 billion and a projected CAGR of over 1875B valuation leads in Europe, Nubank (90B valuation) dominates Latin America, and Chime (11.6B post-IPO valuation) leads in the US.

Cryptocurrency Exchanges and Digital Asset Platforms were defined by intense competition and significant institutional adoption. Binance remained the undisputed leader, processing $7.3 trillion in volume and commanding nearly 40% of the market share.

Buy Now, Pay Later (BNPL) reached a size of 560 billion. Klarna maintained its position as the global leader with over 118 million active consumers and nearly 128 billion in GMV.

Regtech and Compliance Technology reached nearly $19 billion, driven by increasing regulatory complexity from frameworks like DORA and MiCA.

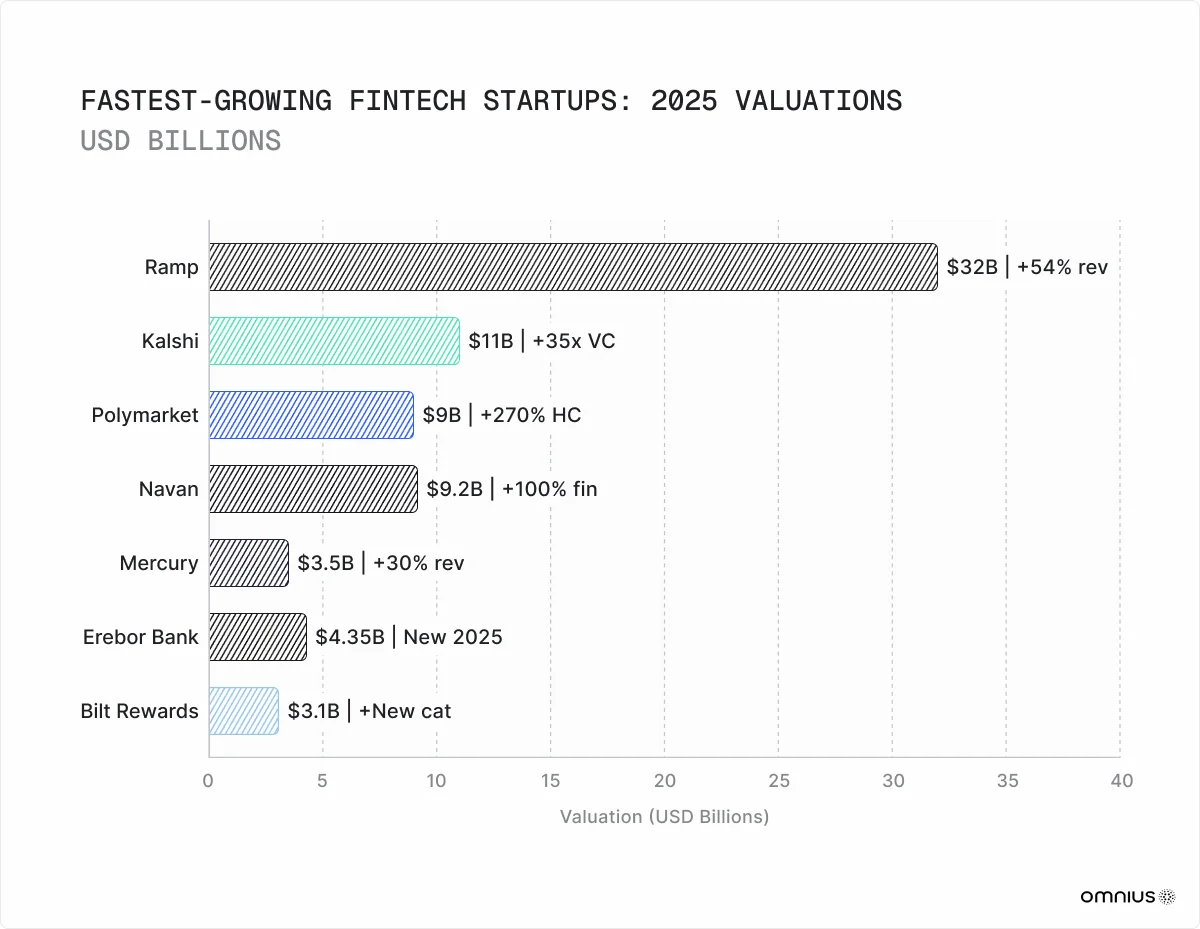

Fastest Growing Fintech Startups and Companies in 2025

While the fintech industry’s titans continued their reign in 2025, a new class of challengers emerged, defined not by quantity but by velocity. In a market where total venture funding rose 25% to nearly $56 billion but the number of deals fell 19%, capital concentrated around a select group of high-speed, focused startups. These companies attacked incumbent models and created entirely new categories, driven by three structural forces: the maturation of AI from a product feature to a core operating model, regulatory clarity that unlocked new markets, and the successful capture of the market gap left by the 2023 collapse of Silicon Valley Bank.

Prediction Markets: A New Asset Class is Born

No category grew more explosively in 2025 than prediction markets. Equity funding in the

sector surged an astonishing 130x, from under $100M in April 2024 to $13B+ in late 2025. This was triggered by a landmark 2024 court victory for Kalshi against the CFTC, which provided the regulatory certainty needed for these platforms to be treated as institutional financial infrastructure.

B2B Finance and Startup Banking: Automating the Back Office

The race to become the financial operating system for modern businesses intensified in 2025. The winners were platforms that moved beyond corporate cards to automate the entire finance stack.

The Rise of the Machine Economy: Agentic AI and KYA

The most forward-looking growth categories of 2025 were those building the foundational infrastructure for an economy where AI agents transact on behalf of humans. The growth was fueled by concrete data, such as a 4,700% year-over-year spike in AI agent-driven retail traffic reported by Adobe, signaling that agent-driven commerce is already happening at scale.

Agentic AI Payments, which builds the payment rails for autonomous AI agents, saw an 80% increase in equity funding. Companies like Catena Labs (backed by Coinbase and Circle) and Skyfire (partnered with Visa) are building the stablecoin-based infrastructure for machine-to-machine commerce.

Know Your Agent (KYA) Identity Infrastructure, a brand-new category that saw over 450% funding growth, provides the identity and authorization layer for the agent economy, answering the critical question: how does a merchant know an AI agent is legitimate and authorized to spend money?

Crypto Infrastructure Matures: RWA Tokenization and Crypto-Native Banking

Real-World Asset (RWA) Tokenization grew over 500% in 2025, from a 5.5 billion market to over 35 billion, driven by institutional demand for on-chain, liquid representations of traditionally illiquid assets like real estate and private credit.

Crypto-Native Banking saw its most audacious new entrant in Erebor Bank, which was founded, funded ($4.35B valuation), and received dual OCC and FDIC charter approval all within the 2025 calendar year, entering a direct race with Mercury to build the defining bank for the next generation of the innovation economy.

Redefining Consumer Finance: WealthTech and Loyalty

AI-Native WealthTech attracted the highest VC funding growth of any fintech sub-sector (90% YoY), using artificial intelligence to provide personalized, scalable investment products for a mass-market audience. Bilt Rewards achieved a rare feat in 2025, creating a new category and scaling to a $3.1 billion valuation by turning rent payments into a loyalty program.

Biggest Fintech Categories in 2025

The fintech industry in 2025 was not a single, monolithic entity but a collection of distinct, powerful categories, each with its own set of market leaders, growth drivers, and competitive dynamics. The year was defined by a few core categories that commanded the lion’s share of investment, transaction volume, and public attention.

Digital Payments & Processing remained the undisputed giant. Businesses running on Stripe alone generated $1.9 trillion in volume, equivalent to roughly 1.6% of global GDP in 2025. Growth was driven by the continued global shift to e-commerce, the widespread adoption of contactless payments, and the maturation of real-time payment networks.

Fintech Lending & Buy Now, Pay Later (BNPL), with a combined market size of over $2 trillion, was a dominant force. The earned-wage access market, a key sub-segment, doubled in size in 2025. AI-driven underwriting models allowed platforms like SoFi and Upstart to assess risk more effectively.

Neobanking & Digital Banking saw a key competitive shift in September 2025 when Revolut dethroned Nubank as the world’s most valuable neobank. The most successful players expanded beyond basic banking to offer a full suite of financial products.

Cryptocurrency & Digital Assets roared back in 2025, driven by significant institutional adoption and newfound regulatory clarity. The passage of the GENIUS Act provided a framework for stablecoins, bringing a new level of legitimacy to the asset class.

Infrastructure & Tokenization saw significant institutional validation when JP Morgan issued a $50 million bond on the Solana blockchain, demonstrating the viability of using public blockchains for traditional financial instruments.

Central Bank Digital Currencies (CBDCs) saw a pivotal year of divergence. While the United States officially paused its retail CBDC efforts, China expanded its e-CNY pilot to over 3.5 billion transactions, and the European Central Bank advanced its Digital Euro project.

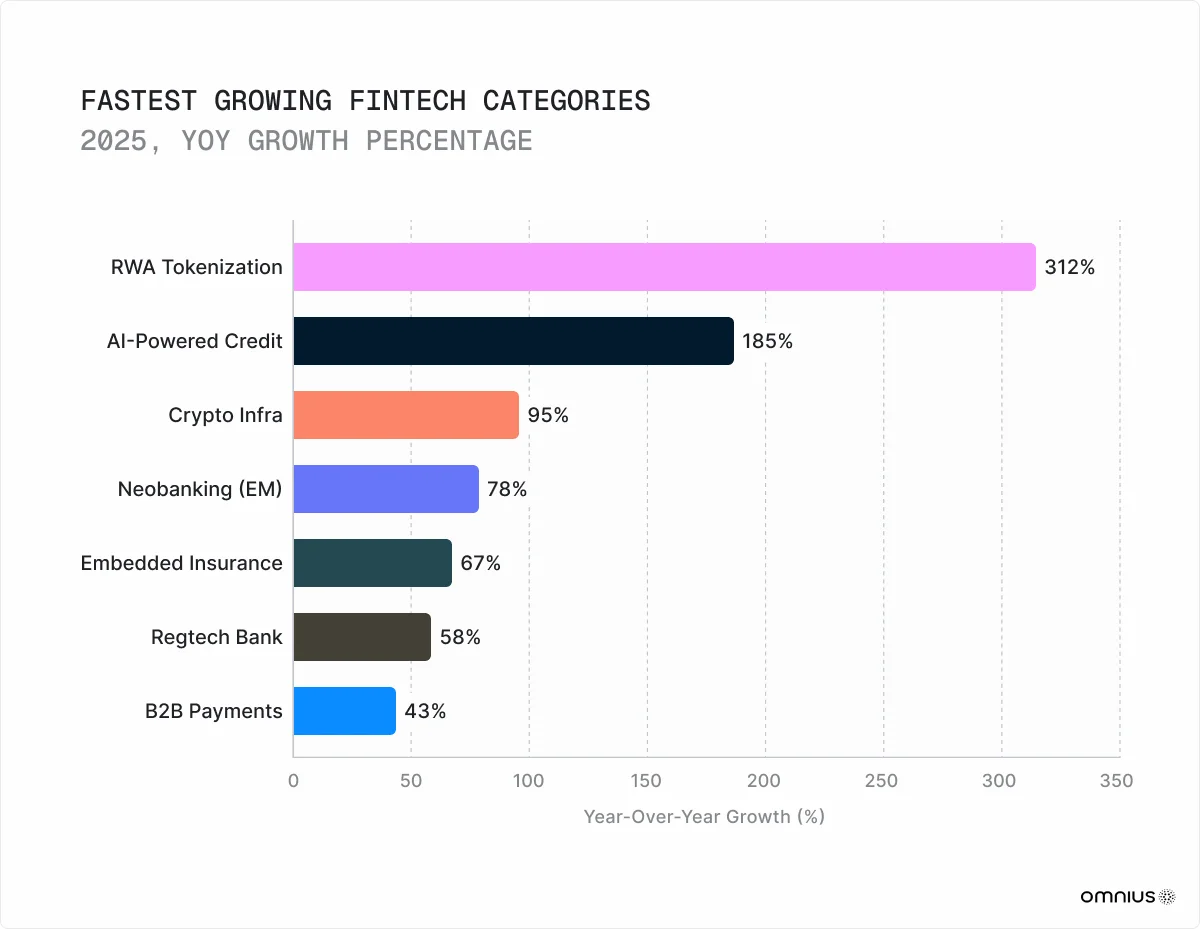

Fastest Growing Fintech Categories in 2025

While the largest fintech categories command the biggest market shares, the most valuable strategic insights often come from observing the rate of change. In 2025, a handful of categories experienced explosive, non-linear growth, driven by specific catalysts like regulatory breakthroughs, technological maturation, and new market formation.

Prediction Markets exploded from a niche curiosity into an institutional-grade asset class, with VC funding surging 35x. Kalshi reached an $11 billion valuation on the back of $1 billion+ in weekly trading volume. The competitive advantage is twofold: a regulatory moat that is difficult to replicate, and a liquidity network effect where deep markets attract more traders. The primary risk is that trading volume is highly event-driven and may decline significantly in a non-election year.

Agentic AI Payments and KYA Identity Infrastructure are the foundation of the emerging machine economy. Agentic AI Payments saw 80% YoY funding growth, validated by the “Adobe Signal”, a 4,700% YoY spike in AI agent-driven retail traffic. KYA, with its >450% funding growth, provides the trust layer for this economy. Both categories are still in their infancy, and there is a significant risk that incumbents like Visa and Mastercard could acquire or build their own solutions.

RWA Tokenization grew over 500% to a $35 billion market as institutions began to represent ownership of real-world assets as tokens on a blockchain.

%20Tokenization.webp)

Stablecoin Infrastructure grew to a $306 billion market cap, spurred by the GENIUS Act, with B2B stablecoin payment volume growing 733% YoY. The primary risk for stablecoins remains regulatory; a hostile shift in policy could severely curtail their use.

B2B Finance Automation, exemplified by Ramp’s growth to $1 billion in annualized revenue, used AI to move beyond corporate cards and automate the entire back-office

finance stack. The moat is deep workflow lock-in combined with an AI data flywheel. AI Native WealthTech saw the highest VC funding growth of any fintech sub-sector (90% YoY) by using AI to offer personalized, sophisticated investment management to a mass-market audience.

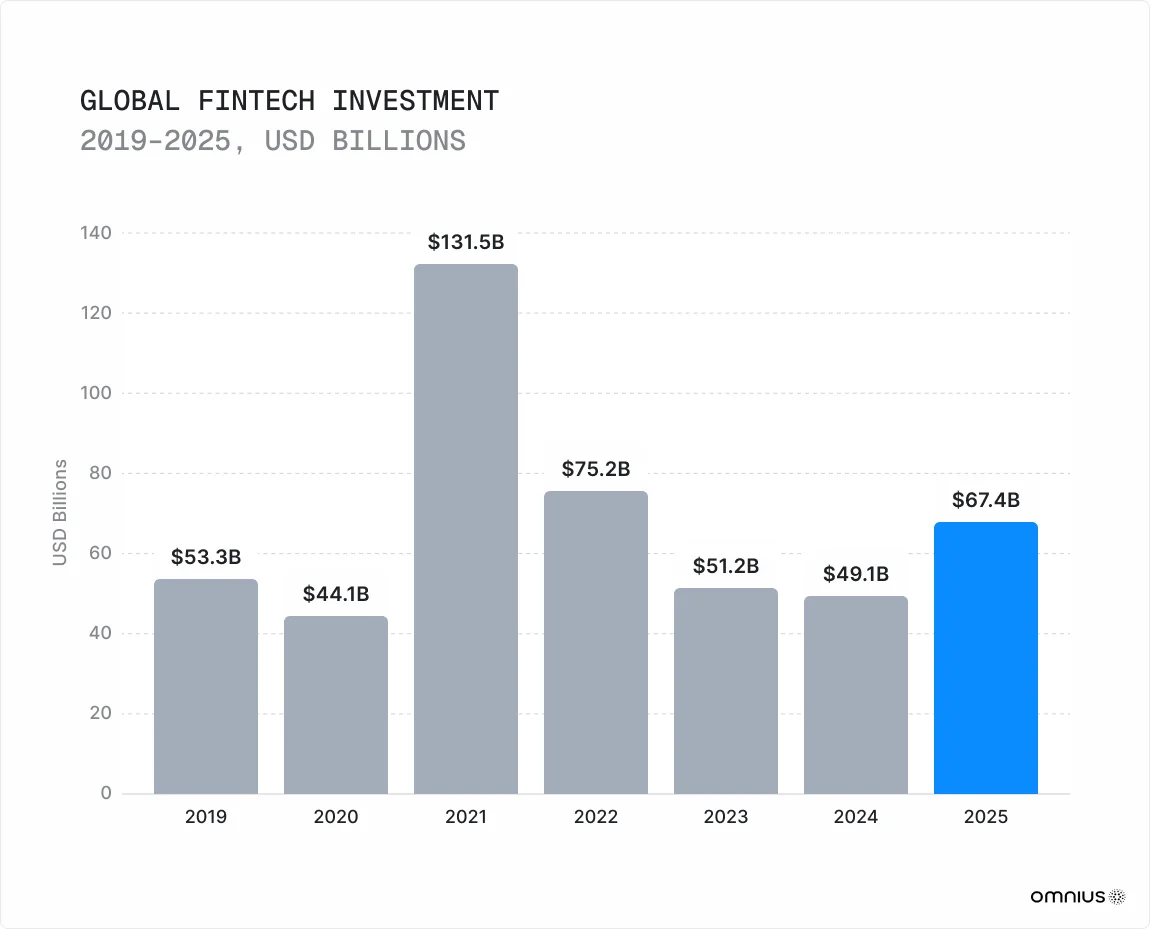

Fintech Biggest Investments and Acquisitions in 2025

The year 2025 marked a decisive turning point for fintech capital markets. After a two-year correction, global fintech investment rebounded sharply to $116 billion, a 21% increase from 2024. This surge in value occurred even as the total number of deals fell by 14.7% to 4,719, signaling a significant “flight to quality” where capital concentrated into fewer, larger, and more strategically coherent transactions.

The defining theme of the year was strategic convergence. The traditional boundaries between fintech sub-sectors dissolved as payments giants acquired crypto infrastructure, crypto exchanges bought traditional brokerages, and AI became a primary acquisition target across all categories. Profitability, not just growth, became the new mantra for investors, with the average M&A multiple settling at a more sober 4.4x EV/Revenue.

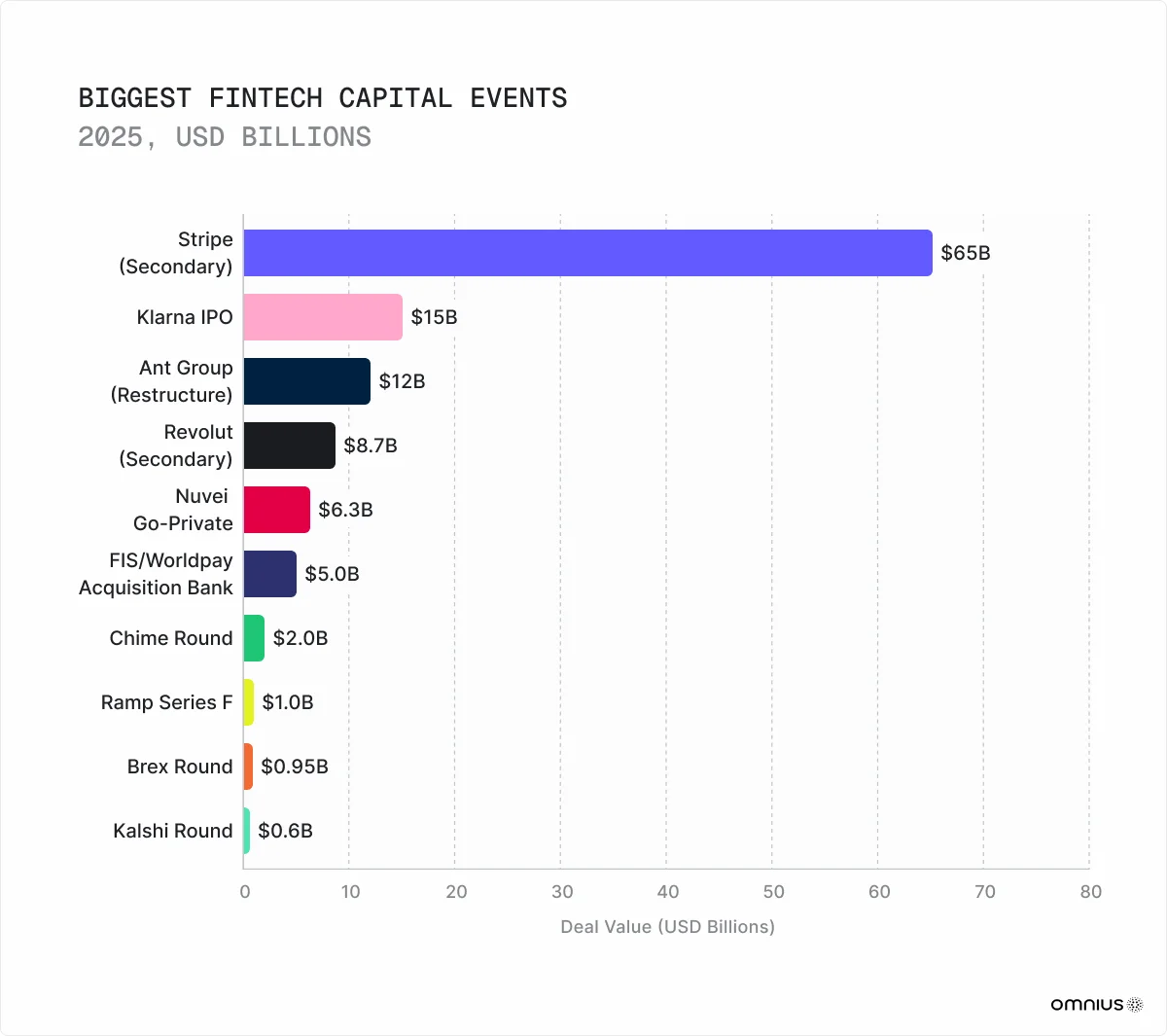

The Ten Landmark Mega-Deals of 2025

The IPO Market Revival

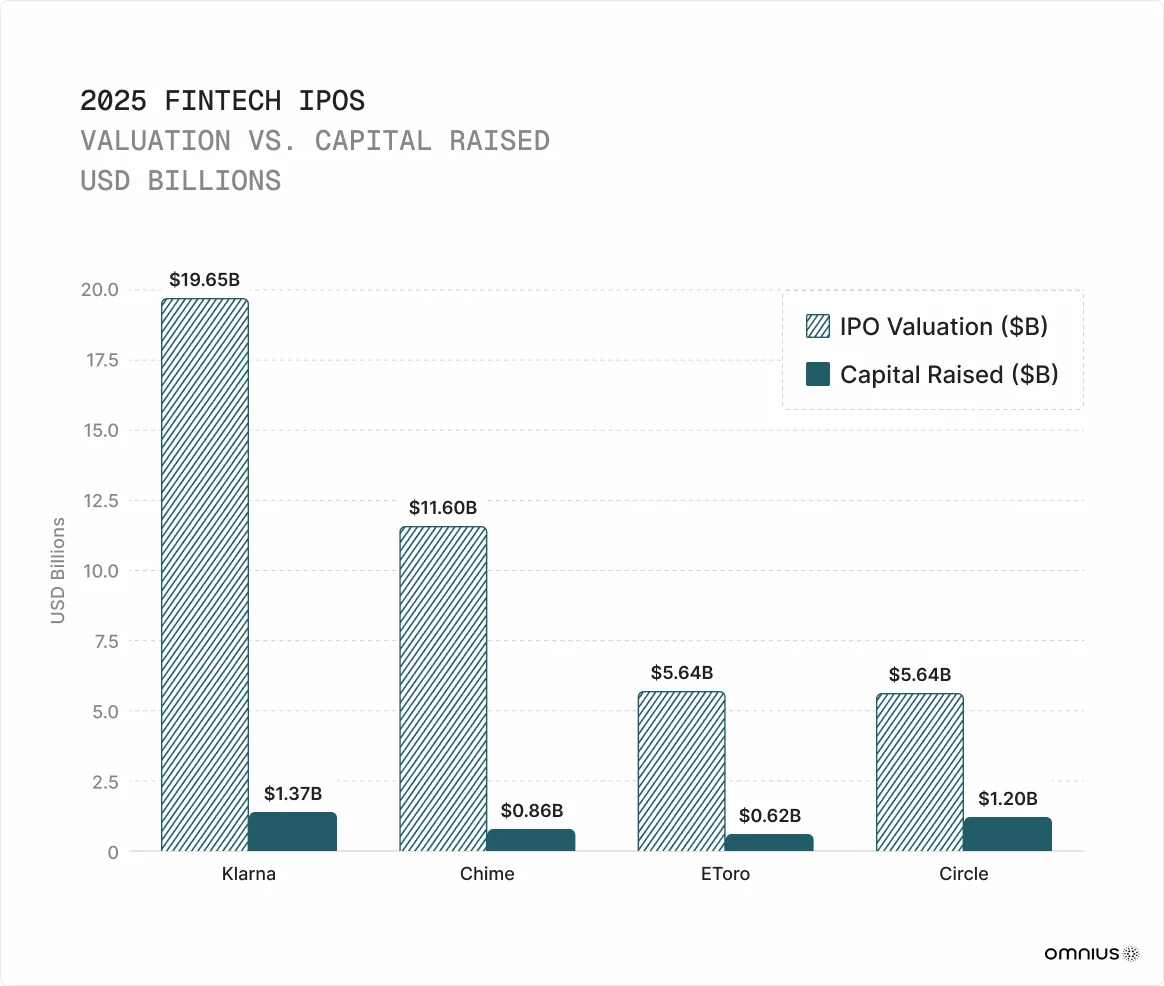

The fintech IPO market saw a dramatic revival in 2025, with total exit value surging 282% year-over-year to $67.6 billion. Four major listings signaled a renewed public market appetite for mature, high-quality fintech assets: Klarna debuted at a $19.65 billion valuation; Chime debuted at an $11.6 billion valuation; eToro debuted at a $5.64 billion valuation; and Circle debuted at a $5.64 billion valuation.

Sector-by-Sector Capital Flows

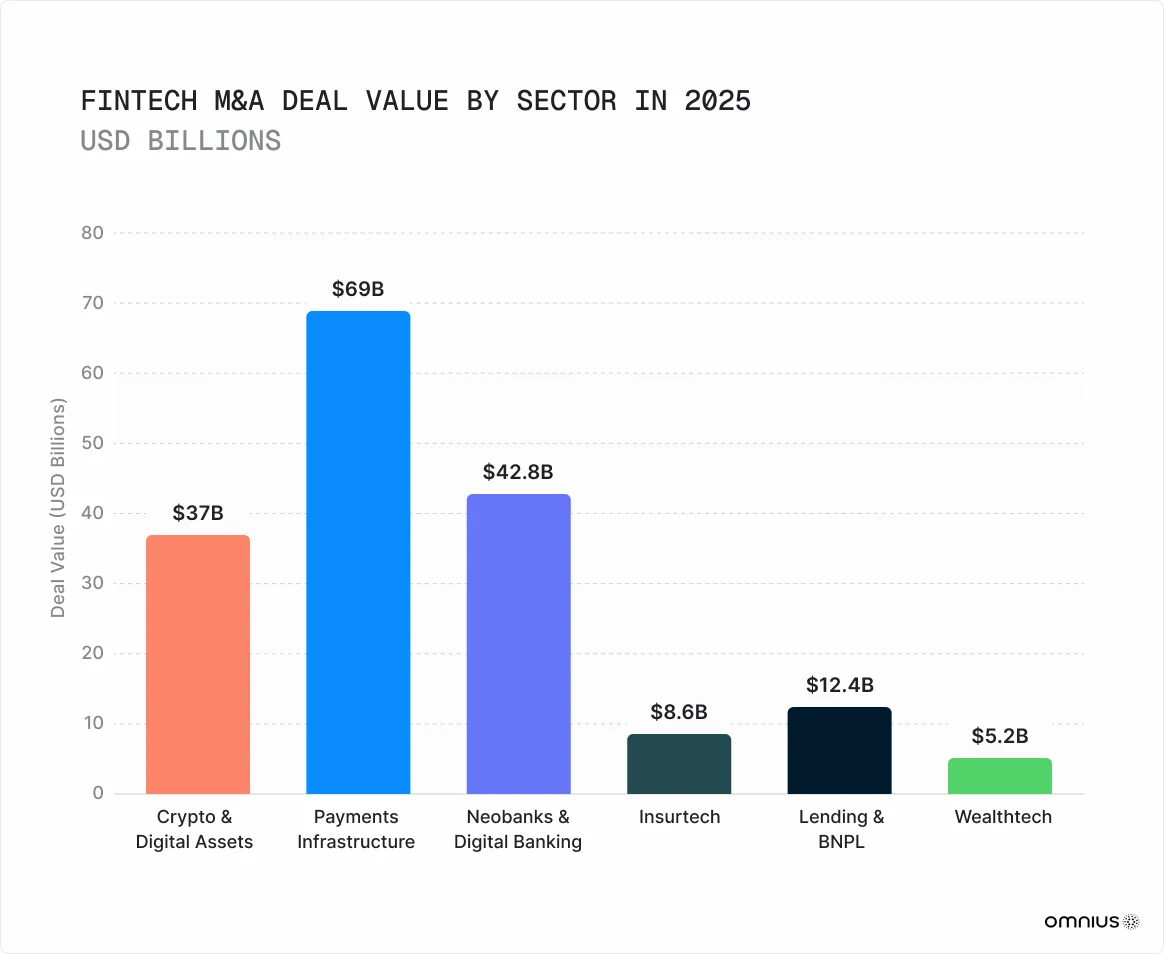

Crypto & Digital Assets was the breakout sector for M&A, with deal value soaring 655% to $37 billion. The theme was “TradFi meets Crypto,” as major crypto players acquired traditional financial infrastructure. Payments Infrastructure consolidation reached $69 billion, with major deals including Xero’s $2.5B acquisition of Melio and TPG’s $2.2B acquisition of AvidXchange. Insurtech saw a surprise comeback, with investment surging 196% to $8.6 billion, driven by traditional incumbents acquiring digital-first platforms. Neobanks & Digital Banking investment reached $42.8 billion.

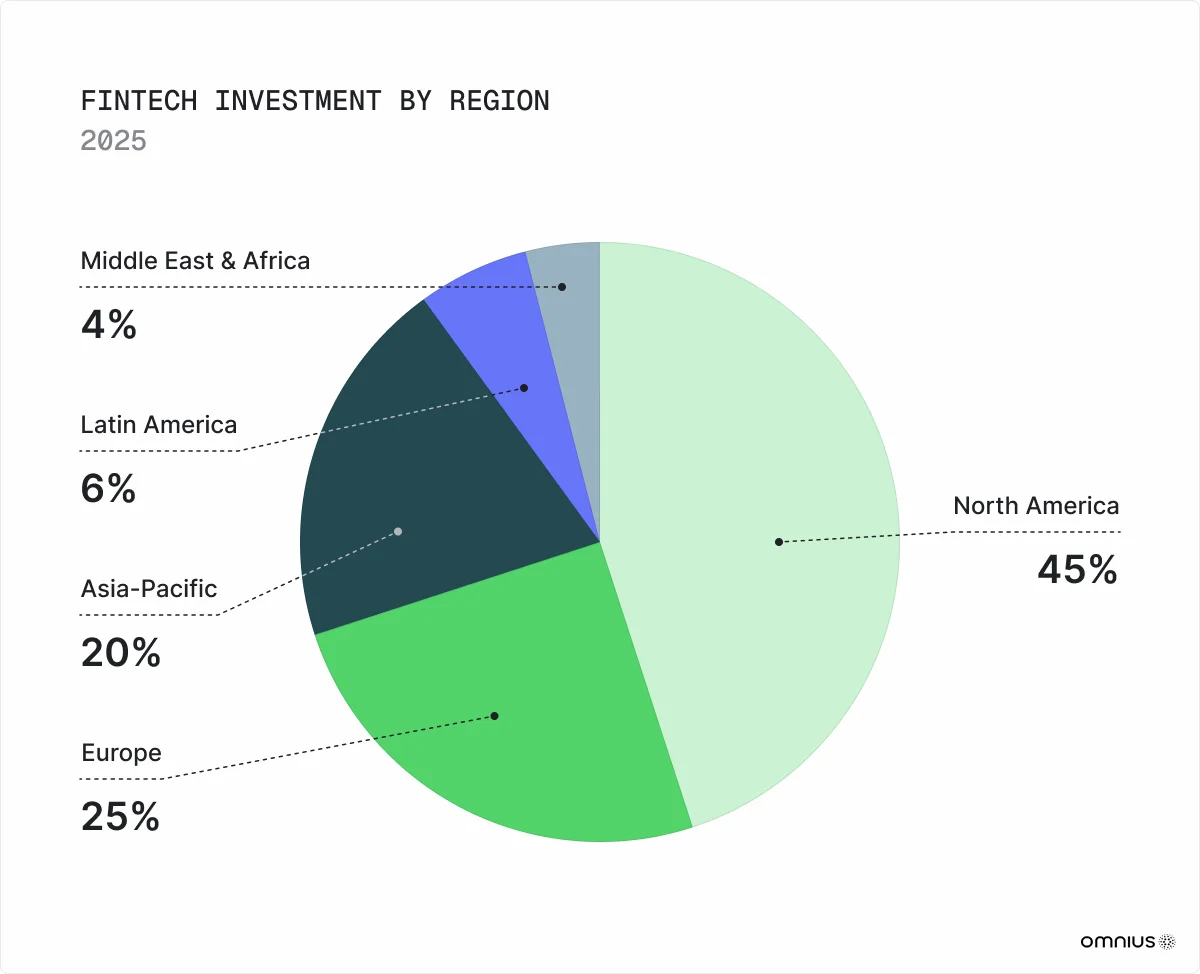

Geographic Distribution of Investment

Geographical Fintech Segmentation and Data Insights 2025

The global fintech market is not a monolith; it is a collection of distinct regional stories, each shaped by its own unique regulatory landscape, consumer behavior, and technological infrastructure. While sources vary on the precise total market size, with estimates for 2025 ranging from $255 billion to $395 billion, they agree on the overall trend: a decisive rebound in investment to $116 billion and a clear divergence in the growth narratives of each major geography.

Global Fintech Market at a Glance — 2025

Regional Deep Dives

North America: The Leader in Innovation and Investment. North America attracted $66.5 billion in investment in 2025, with the US alone accounting for $56.6 billion. The market is characterized by its mature infrastructure, high consumer adoption (77% of consumers prefer digital banking), and its role as the epicenter of AI and crypto innovation. The most consequential development was the passage of the GENIUS Act, the first federal stablecoin framework in US history. The leading players are Stripe, Chime, Coinbase, Robinhood, and Cash App.

Europe: The Regulatory Superpower. Europe’s fintech advantage is structural, built on the most advanced regulatory architecture in the world. The implementation of the EU Instant Payments Regulation and the full applicability of MiCA in 2025 created a unified, pan European market. The UK remained the single largest investment destination in Europe ($3.6B). Europe’s leaders include Revolut, Monzo, Wise, Klarna, and Adyen. The EU’s single-market scale means continental Europe will increasingly export its fintech infrastructure globally.

Asia-Pacific: The Scale and Growth Engine. Asia-Pacific is the largest fintech market by size and the fastest-growing major region, with a projected CAGR of up to 27.45%. India’s Unified Payments Interface (UPI) has become the global template for real-time payments, processing over 18 billion transactions per month in 2025. In China, the super-apps Alipay and WeChat Pay process a staggering $68 trillion in annual transaction volume. The region is led by Ant Group, PhonePe, Paytm, GrabFinancial, and Airwallex.

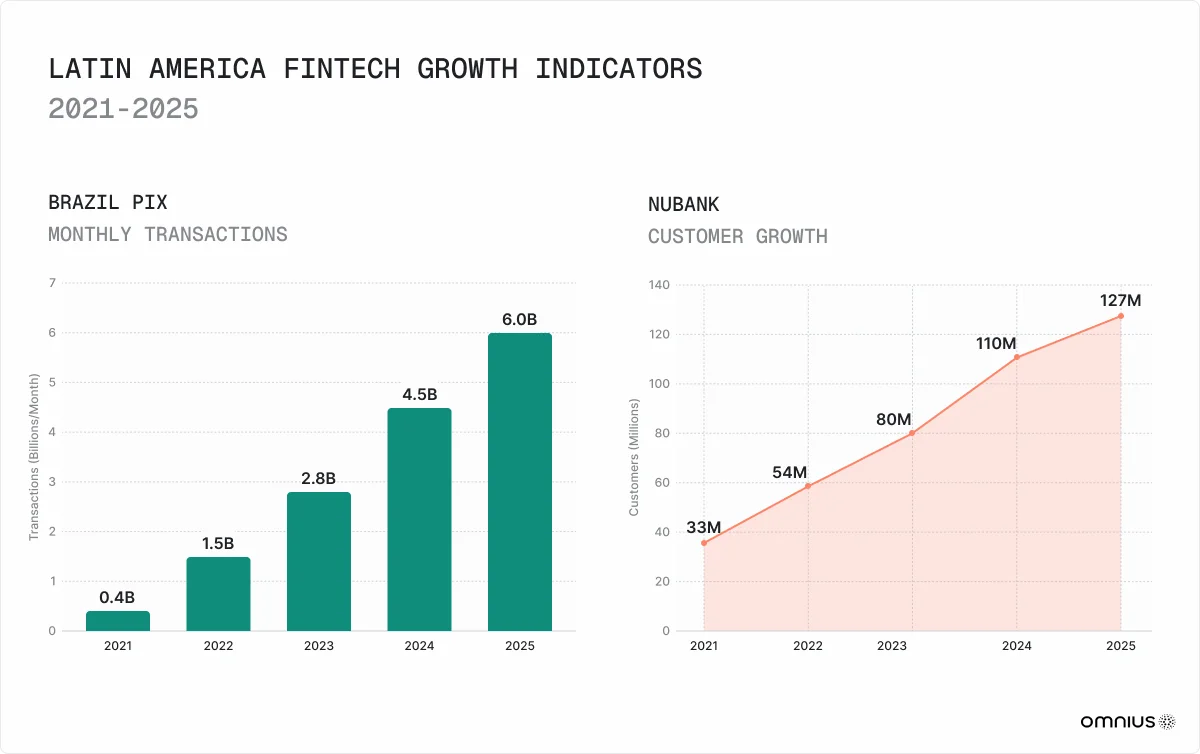

Latin America: The Financial Inclusion Frontier. With 70% of its population unbanked or underbanked, Latin America represents the world’s largest financial inclusion opportunity outside of Sub-Saharan Africa. Brazil is the regional powerhouse, where the central bank’s Pix instant payment system processes over 6 billion transactions per month. Nubank reported 122 million active users and became the most profitable neobank globally in 2025.

MENA & Africa: The Mobile-First Future. The MENA region saw the fastest funding growth globally (+80% YoY), driven by sovereign wealth investment. In Africa, mobile money is the dominant financial service, with platforms like M-Pesa providing essential services to tens of millions of people who have never had a traditional bank account. Key players include Tabby and Tamara in MENA, and M-Pesa, OPay, and Interswitch in Africa.

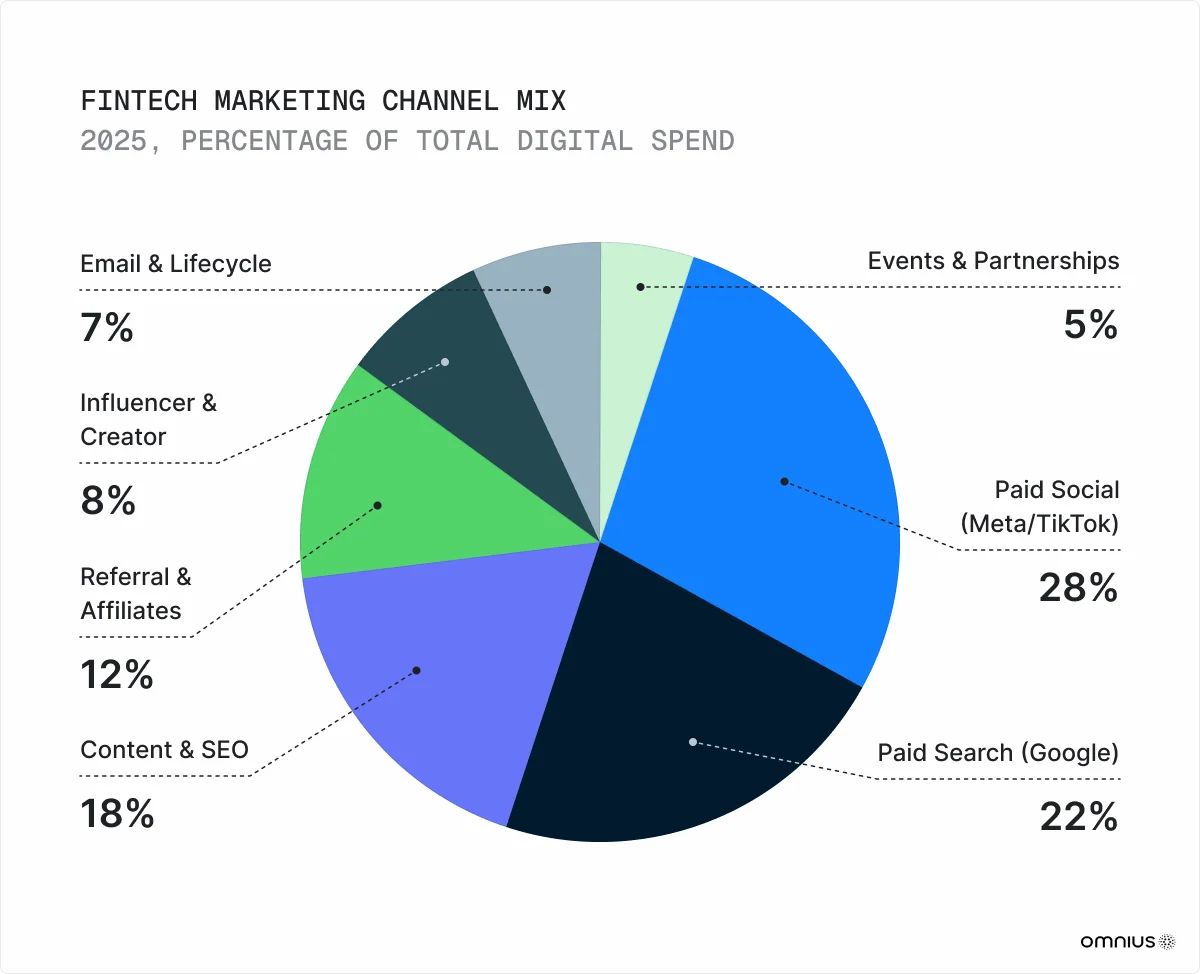

Fintech Marketing Trends and Stats in 2025

Fintech marketing in 2025 was defined by a series of seismic shifts that forced a fundamental re-evaluation of strategy. It was a year characterized by three simultaneous pressures: record-high customer acquisition costs, the fracturing of traditional digital discovery channels by AI, and the rise of a new generation of creators as the primary arbiters of financial trust. The companies that thrived were not those with the largest budgets, but those that mastered a new playbook combining data-driven precision with authentic, human-centric storytelling.

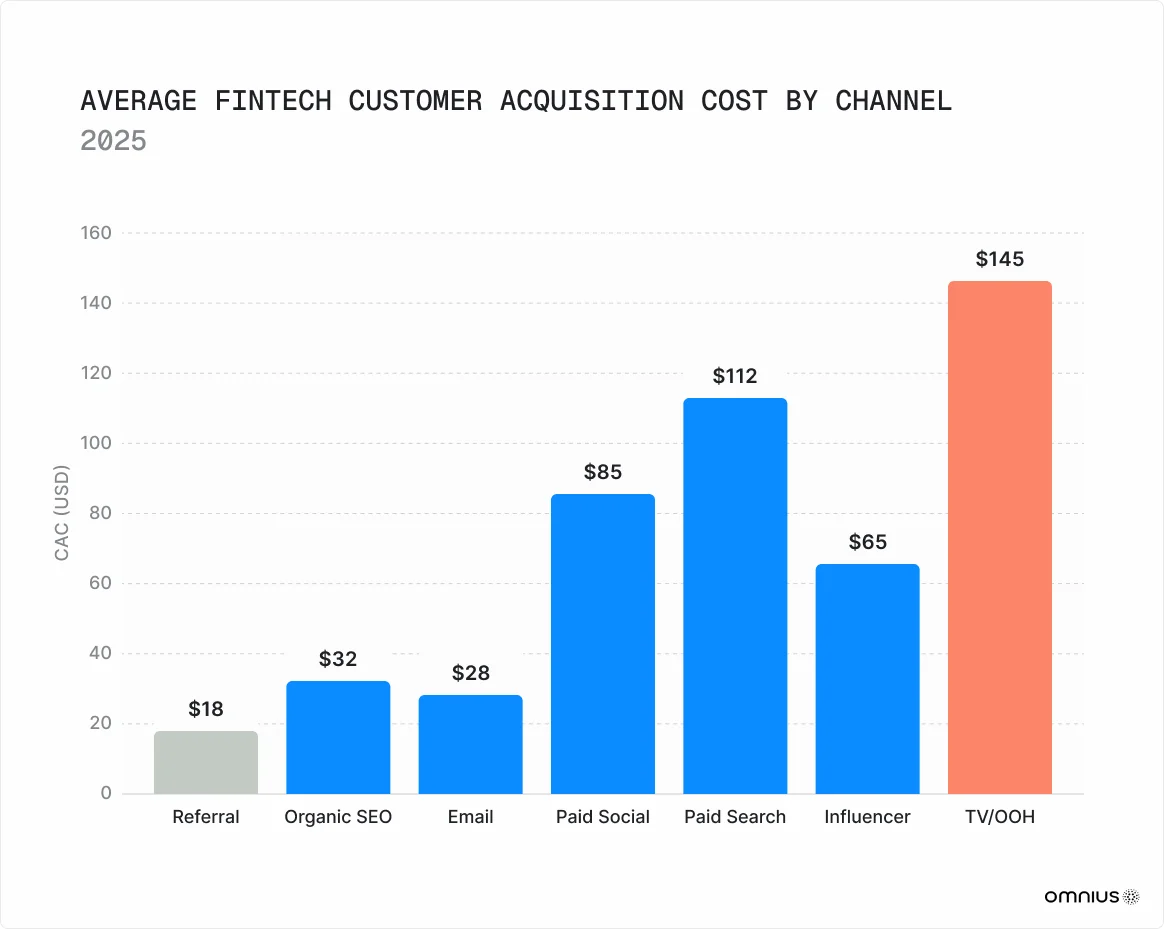

The Customer Acquisition Cost (CAC) Crisis

The most significant headwind for fintech marketers in 2025 was the spiraling cost of acquiring customers. The industry-wide average CAC surged by 40-60% between 2023 and 2025, reaching an industry-high average of $1,450. This was driven by intense competition, the inherent trust deficit in financial services, and significant compliance overhead. However, this average masks a wide variance by acquisition channel.

This economic reality forced a strategic shift toward channels with more durable unit economics, such as organic content, referral programs, and community-led growth, to achieve a healthy LTV:CAC ratio of 3:1 or higher.

The AI Disruption: From Search to Personalization

The shift from traditional search to AI-generated answers became a 2025 operating reality. Google’s AI Overviews, reaching 1.5 billion users monthly, drove a 61% decline in organic click-through rates for informational queries. This gave rise to Generative Engine Optimization (GEO), a new practice focused on getting content cited within AI answers. The strategic nuance is critical: Google AI Overviews tend to cite sources that already rank in the top 10, while ChatGPT often cites lower-ranking pages, and Perplexity favors fresh, proprietary data. A multi-platform AI visibility strategy became essential.

Simultaneously, AI became the operational standard for personalization. The AI-in-CRM market reached $11 billion, and AI-powered personalization was shown to increase conversion rates by up to 30%. Bank of America’s AI assistant, Erica, set the industry benchmark by handling 70% of customer queries, demonstrating the power of AI to deliver personalized service at scale.

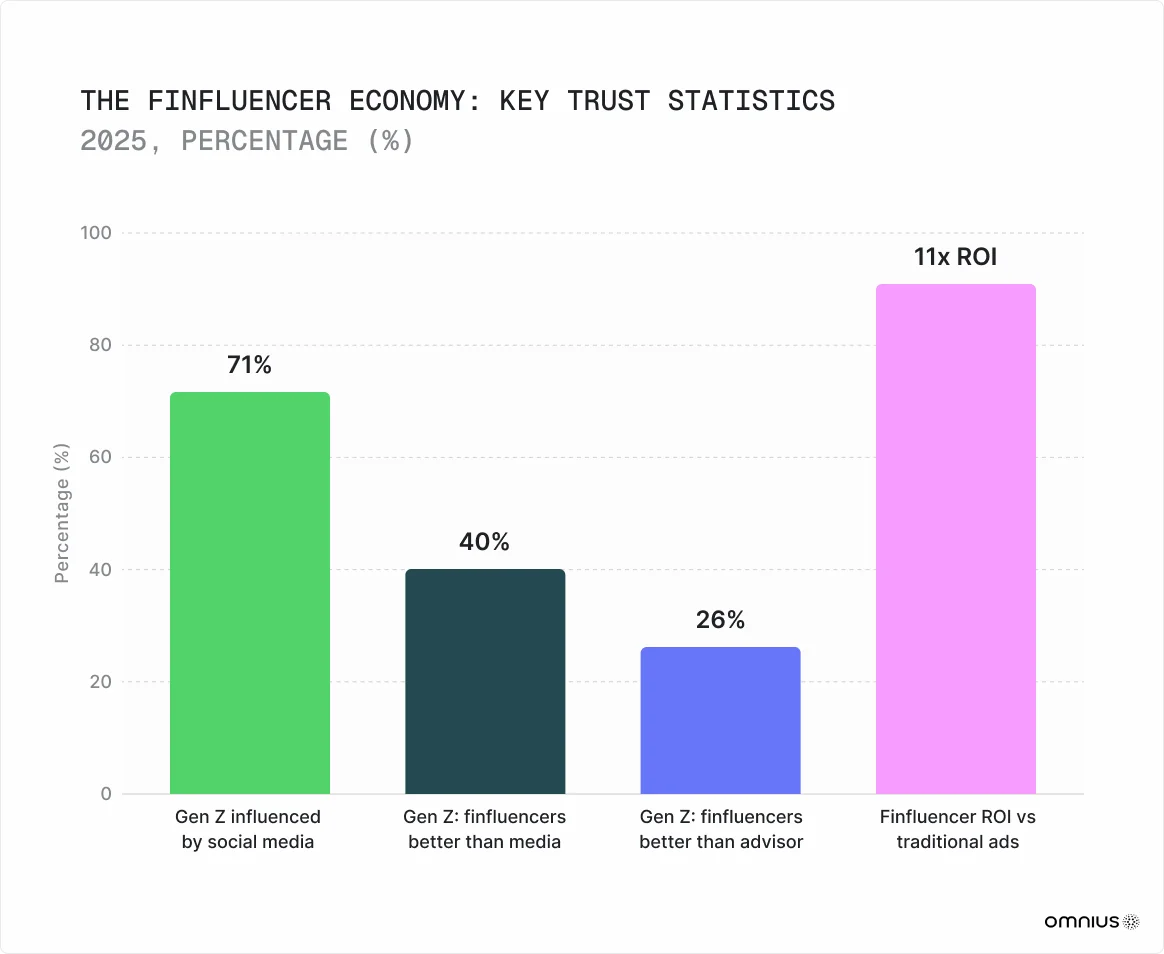

The Social Trust Revolution: The Rise of the Finfluencer

Perhaps the most consequential shift of 2025 was the transfer of trust from institutions to individual creators. The “finfluencer” economy reached maturity, with TikTok becoming a primary source of financial education. 71% of Gen Z report that their financial decisions are influenced by social media. 40% of Gen Z say FinTok influencers give better advice than traditional media, and 26% say it is better than what they receive from their own financial provider. Fintech-focused influencer campaigns achieved 11x the ROI of traditional digital advertising. This forced brands to build authentic, compliance-vetted partnerships that leveraged creator credibility to bridge the industry’s persistent trust deficit.

B2B Marketing and the Rise of ABM

While consumer trends dominated headlines, B2B fintech marketing underwent its own revolution with the widespread adoption of Account-Based Marketing (ABM). With 70% of B2B marketers using an ABM strategy, companies reported an average 208% increase in revenue from these efforts. The structural driver was the complexity of enterprise sales, long buying cycles and multiple stakeholders, which made personalized, account-specific marketing far more effective than broad demand generation.

Regulatory Constraints and Brand Building

Regulatory compliance became a significant marketing cost center in 2025. 60% of fintech companies paid at least $250,000 in compliance fines in the previous year, making a compliance-first marketing workflow a necessity, not a choice. In this high-stakes environment, brand marketing became synonymous with trust-building. Sports sponsorships emerged as a high-impact channel, with Airwallex’s partnership with the McLaren F1 team delivering a 70% increase in consumer trust metrics, a remarkable return for a B2B brand.

Best Fintech Marketing Campaigns of 2025

In 2025, fintech marketing crossed a significant threshold, evolving from a focus on performance and product features to a full-fledged embrace of brand building and cultural relevance. As customer acquisition costs from paid channels surged, the most innovative companies recognized that brand equity was a more durable competitive moat. This section analyzes five of the most impactful and strategically significant fintech marketing campaigns of the year, each demonstrating a different facet of this “brand turn.”

1. Cash App: The Cultural Collaborator

The Strategic Problem: Despite its dominance in P2P payments among Gen Z, Cash App needed to broaden its appeal and drive adoption of its expanding banking suite. The objective was to establish Cash App as a lifestyle brand, not just a utility.

The Campaign: A sophisticated, two-tiered campaign. The main “Cash In” brand films, directed by Emmy-nominee Ramy Youssef, used documentary-style realism to build emotional relevance. This was paired with a high-impact cultural moment: a short film starring Timothée Chalamet that screened in cinemas before summer blockbusters including Superman and Fantastic Four. The counterintuitive casting of a prestige actor generated significant earned media, with the campaign covered by entertainment press rather than just marketing trade publications.

The Impact: The Chalamet film garnered over 10.5 million YouTube views in its first month, proving that Hollywood-quality creative can compete for cultural attention. The earned media value from celebrity casting effectively made the cinema buy free, demonstrating that a single, well-executed cultural moment can be more efficient than millions in traditional ad spend.

2. Revolut: The Global Expansion Vehicle

The Strategic Problem: With 65 million customers, Revolut was a European giant but remained largely unknown in the US, Asia, and Latin America. It needed a global-reach vehicle to accelerate expansion without market-by-market brand building.

The Campaign: A $50 million-per-year title sponsorship of the Audi F1 Team, announced July 30, 2025. This was more than a logo placement; it was the purchase of global expansion infrastructure. The team would formally be called the Audi Revolut F1 Team. The narrative alignment was perfect: Audi, a newcomer to F1, and Revolut, a challenger to incumbent banks, shared a story of ambitious disruption. Revolut Business was also integrated into the team’s financial operations, powering seamless checkout solutions for merchandise.

The Impact: With a global F1 fanbase of 827 million, the sponsorship provided Revolut with a cost-per-fan-reached of approximately $0.06, a level of efficiency impossible to replicate through digital advertising. Revolut didn’t buy F1 branding; it bought a global expansion platform, transforming every race into a brand story.

3. Monzo: The Emotional Rebrand

The Strategic Problem: With over 9 million users, Monzo was well-known but not well understood. The campaign was built on a powerful customer insight: Monzo users were seven times more likely to use the word “love” to describe their bank than customers of any other bank.

The Campaign: The “Money Never Felt Like Monzo” campaign, developed with the creative studio Uncommon, translated this feeling into a series of visceral, emotional visual metaphors: arguments became embraces, anxiety became joy. The campaign ran across TV, cinema, and out-of-home, a significant investment in brand over performance.

The Impact: The results provided the clearest causal link between brand investment and business outcomes in 2025. A 77% increase in marketing spend to £97.4M coincided with Monzo’s first £1 billion revenue year (+48% YoY), an 8x increase in profit, and the addition of 2.2 million new customers. Notably, 67% of new customers still came via word of mouth, demonstrating that the ATL campaign amplified rather than replaced organic growth.

4. Nubank: The Entertainment Co-Creator

The Strategic Problem: As the world’s largest digital bank outside of Asia with 118.6 million customers, Nubank needed to support its expansion into Mexico and Colombia while reinforcing its brand identity.

The Campaign: A partnership with Netflix for the second season of the hit show “Wednesday.” Instead of a simple sponsorship, Nubank’s internal creative team co-created an original animated character, “Littlefoot”, a charismatic animated foot with dreams of becoming an actor, inspired by the show’s iconic “Thing.” This was Nubank’s first campaign to air simultaneously in two countries, launched July 30, 2025.

The Impact: The campaign reached over 115 million customers across Brazil and Mexico, demonstrating a new model for fintech marketing: co-creating entertainment content rather than simply advertising alongside it. By embedding its brand within a globally recognized cultural phenomenon, Nubank generated massive reach and engagement while reinforcing its identity as a creative and culturally relevant financial partner.

5. Airwallex: The B2B Brand Builder

The Strategic Problem: As a B2B payments infrastructure company, Airwallex faced the challenge of building brand credibility and trust in a crowded market.

The Campaign: A multi-year partnership with the McLaren Formula 1 team. This was not just a sponsorship but a deep integration, with Airwallex technology powering the team’s global financial operations. The partnership was activated through co-branded content, VIP experiences, and tech showcases that demonstrated the real-world performance of Airwallex’s infrastructure.

The Impact: The partnership generated over 200 million media impressions and was credited with a 70% increase in consumer trust metric, a remarkable return for a B2B brand. For B2B fintechs, a premium sports partnership can be a powerful tool for transferring credibility and demonstrating technological prowess in a real-world, high performance environment.

Conclusion

The fintech industry in 2025 marked a clear transition from disruption to integration. What was once a fragmented ecosystem of challengers has evolved into a core component of the global financial system, defined by stronger regulation, improved business fundamentals, and deeper collaboration with traditional institutions. Profitability, operational efficiency, and trust have replaced rapid, unsustainable growth as the primary drivers of success.

At the same time, innovation has not slowed, it has matured. Advances in artificial intelligence, the rise of embedded finance, and the institutionalization of digital assets have reshaped how financial services are delivered and consumed. New categories such as agent-driven commerce and tokenized assets signal that the industry is still in an early phase of long-term transformation.

Ultimately, 2025 demonstrated that fintech is no longer an alternative to traditional finance, it is its evolution. The companies that will define the next decade are those that can balance innovation with compliance, growth with profitability, and technology with trust.

FAQs

1. What does the fintech industry report 2025 say?

The fintech industry report 2025 highlights a rebound in global investment, reaching around $116 billion, along with stronger profitability and more selective funding. It shows the sector maturing, with a focus on sustainable growth rather than rapid expansion.

2. What are the key trends in the fintech industry in 2025?

Key trends include AI-driven financial services, embedded finance, open banking, and the rise of digital assets like stablecoins. There is also increased regulatory scrutiny and a stronger focus on efficiency and profitability.

3. Is the fintech industry growing in 2025?

Yes, the fintech industry is still growing, with revenues increasing by over 20% year-over-year, outperforming traditional financial services. However, growth is becoming more disciplined, with investors focusing on high-quality, scalable companies.

.png)

.svg)

.svg)