SaaS in 2025: Key Statistics, Benchmarks, and Industry Findings

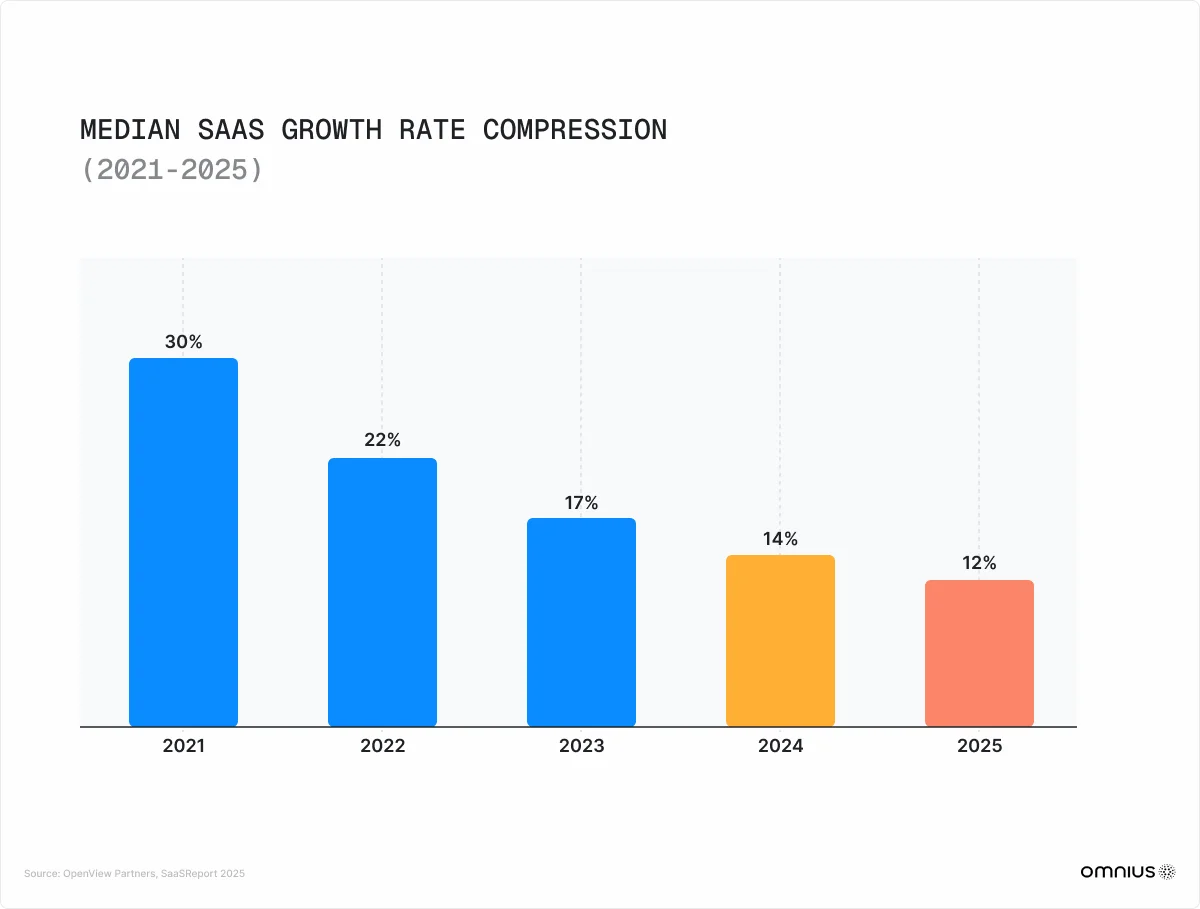

- Growth rates have hit a structural floor. The median SaaS growth rate compressed to 12% in 2025, down from 30% in 2021, forcing a permanent industry pivot from top-line expansion to capital efficiency.

- AI-native architectures are heavily outperforming AI-added features. Companies capturing the most enterprise value (like Palantir and Cursor) built systems entirely around AI capabilities, rather than bolting AI features onto legacy systems of record.

- The "System of Action" is replacing the "System of Record." As AI commoditizes data storage and retrieval, pricing power has shifted entirely to platforms that execute complex workflows and deliver measurable operational outcomes.

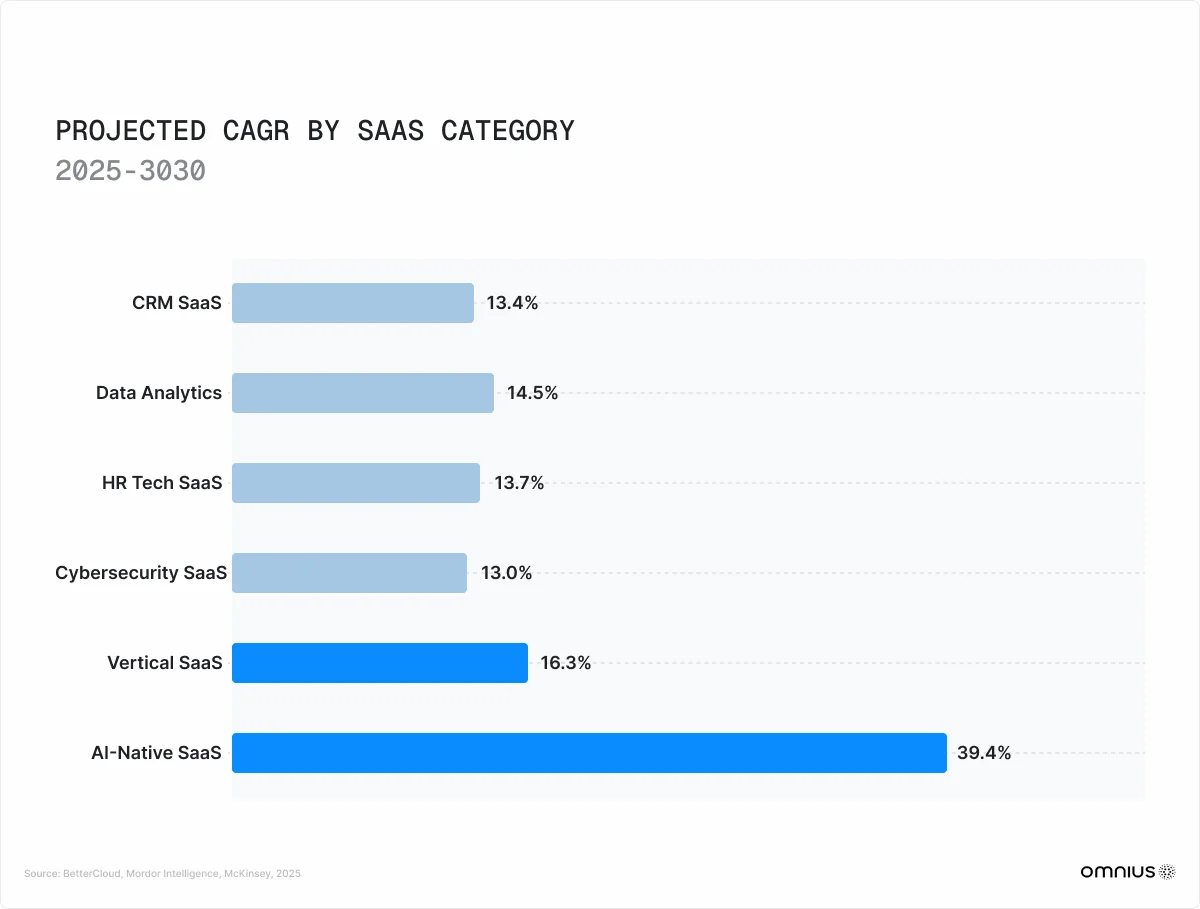

- Vertical SaaS is capturing a disproportionate share of the market. With a 16.3% CAGR, vertical SaaS companies are up to 3.3 times more likely to become financial outliers than horizontal tools, driven by deep domain expertise and embedded fintech revenue.

- Usage-based pricing is now the industry standard. 85% of SaaS companies have adopted usage-based or hybrid pricing models, acknowledging that seat-based pricing breaks down when AI allows fewer human users to accomplish more work.

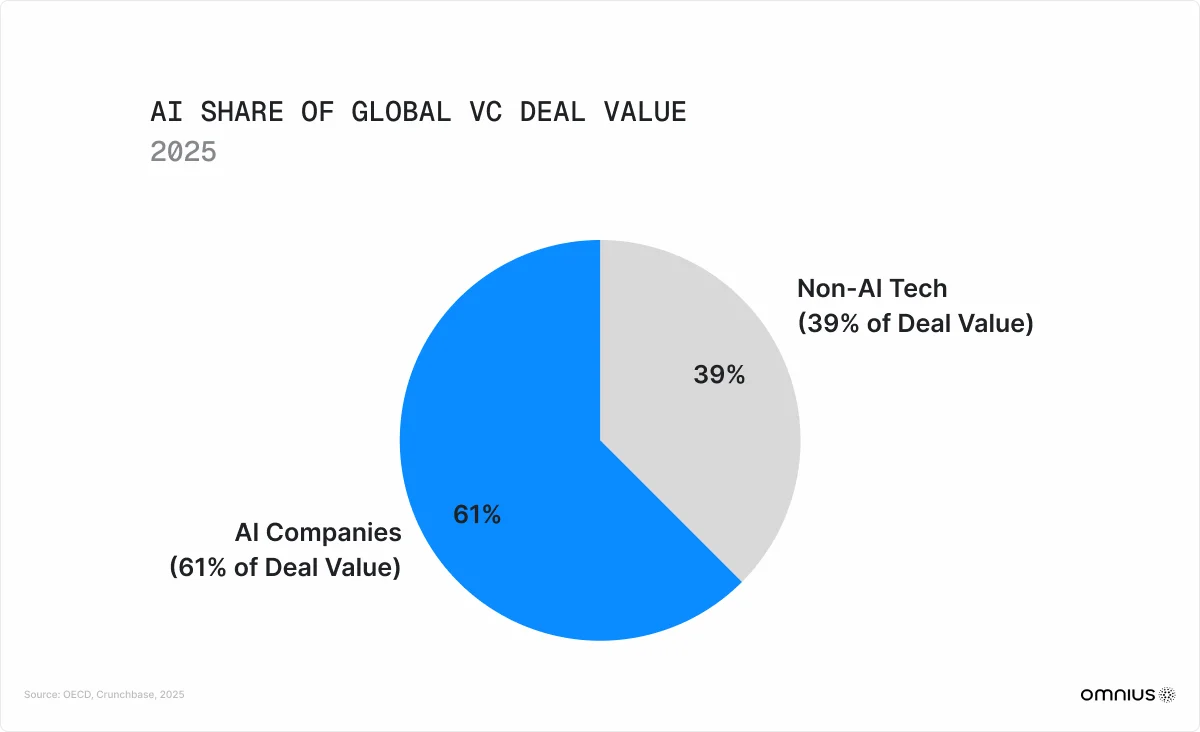

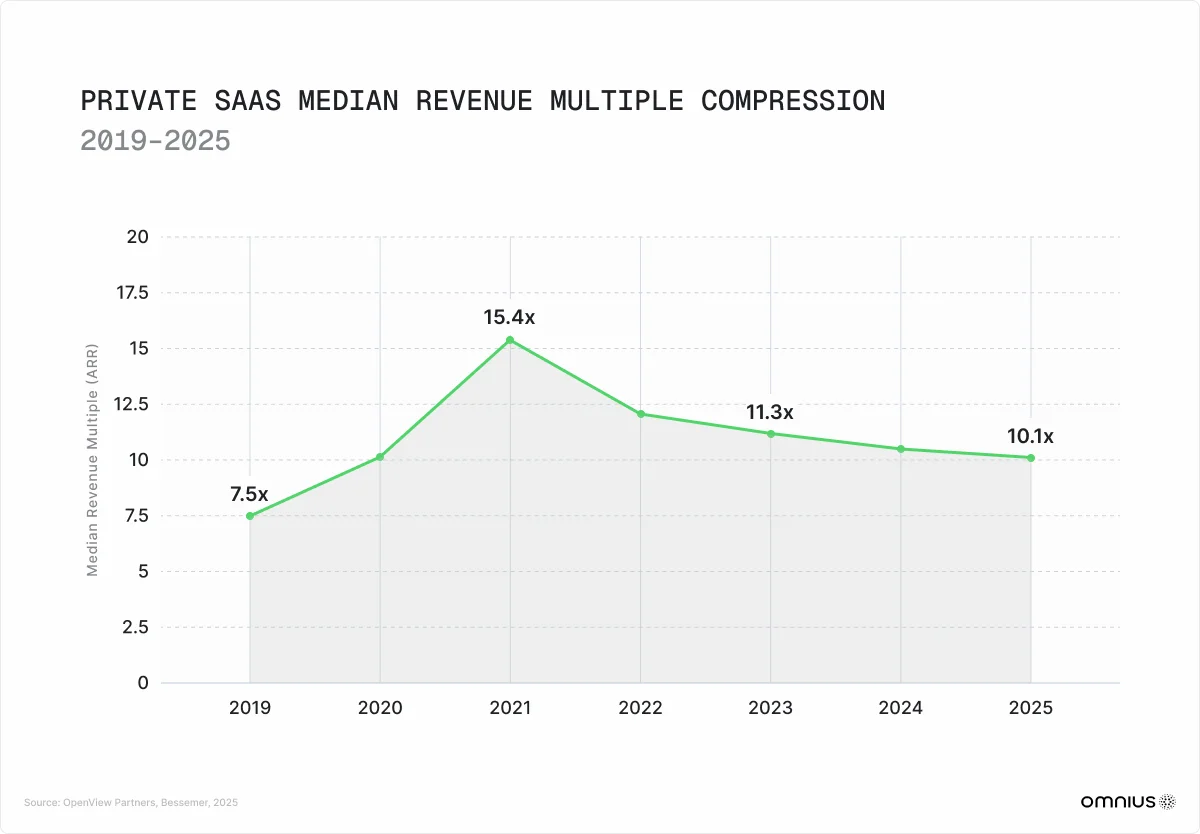

- Venture capital is highly concentrated. AI companies absorbed 61% of all VC deal value in 2025, leaving traditional SaaS companies stranded on a $500 billion dry powder backlog with compressed revenue multiples of roughly 10.1x.

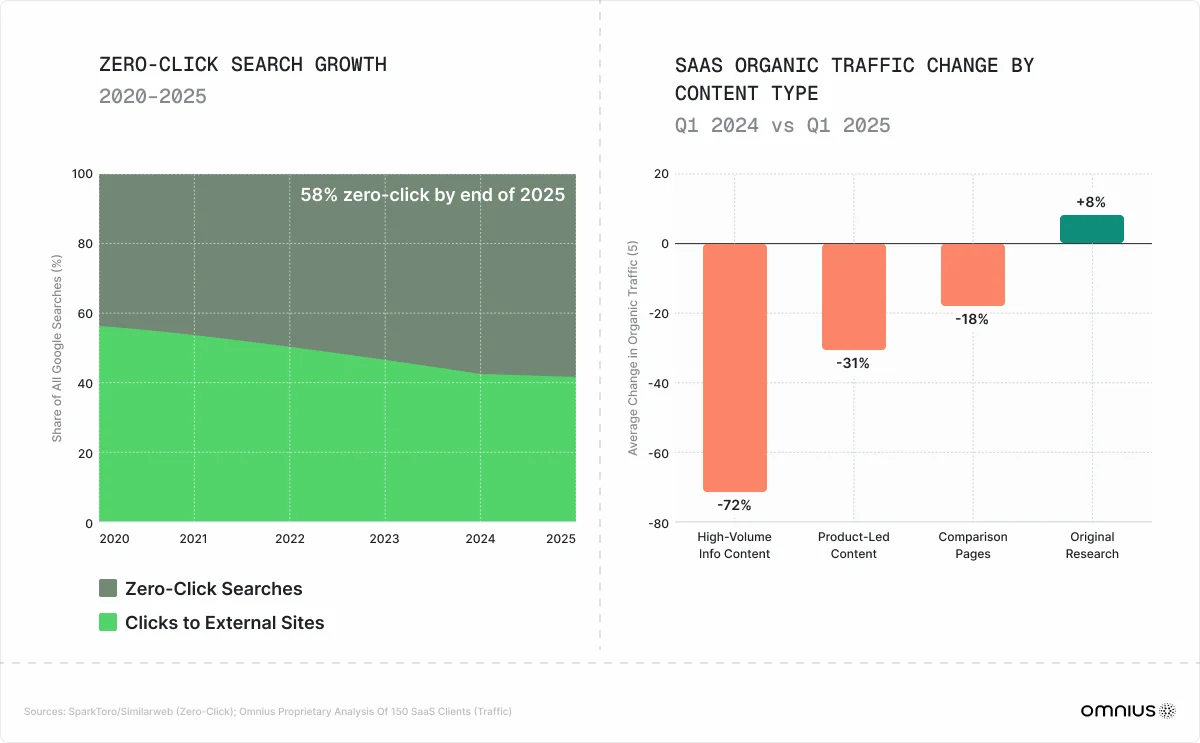

- Traditional SaaS SEO is no longer enough. The rollout of AI Overviews and aggressive Google algorithm updates caused organic search traffic for broad informational content to drop by up to 80%.

Introduction

The global SaaS market reached $315.68 billion in 2025 and continues its expansion as AI deepens its integration into enterprise workflows. Projections indicate that this trajectory is far from over. The market is expected to expand at a CAGR of roughly 20%, potentially reaching an astonishing $1.13 trillion by 2032.

.webp)

However, the era of predictable growth is over. The market is huge, but the rules deciding who captures that growth have permanently changed. We are currently witnessing a profound market bifurcation. A distinct group of companies has accelerated dramatically by embracing AI-native architectures and deep vertical specialization.

Meanwhile, the vast majority of horizontal platforms have struggled to maintain momentum as enterprise budgets tighten and software spending consolidates.

1. What Happened in SaaS in 2025: Palantir, Salesforce, Anthropic

The SaaS industry experienced huge market divergence in 2025, driven by a single underlying thesis: the market is ruthlessly separating companies that execute AI from companies that perform AI.

Palantir executed. Salesforce performed. Anthropic is funding the infrastructure layer underneath both. And the traditional SEO is not enough when AI execution reaches the distribution layer. The financial markets heavily rewarded companies that could prove real enterprise adoption of AI while punishing those that merely marketed AI as a surface-level feature.

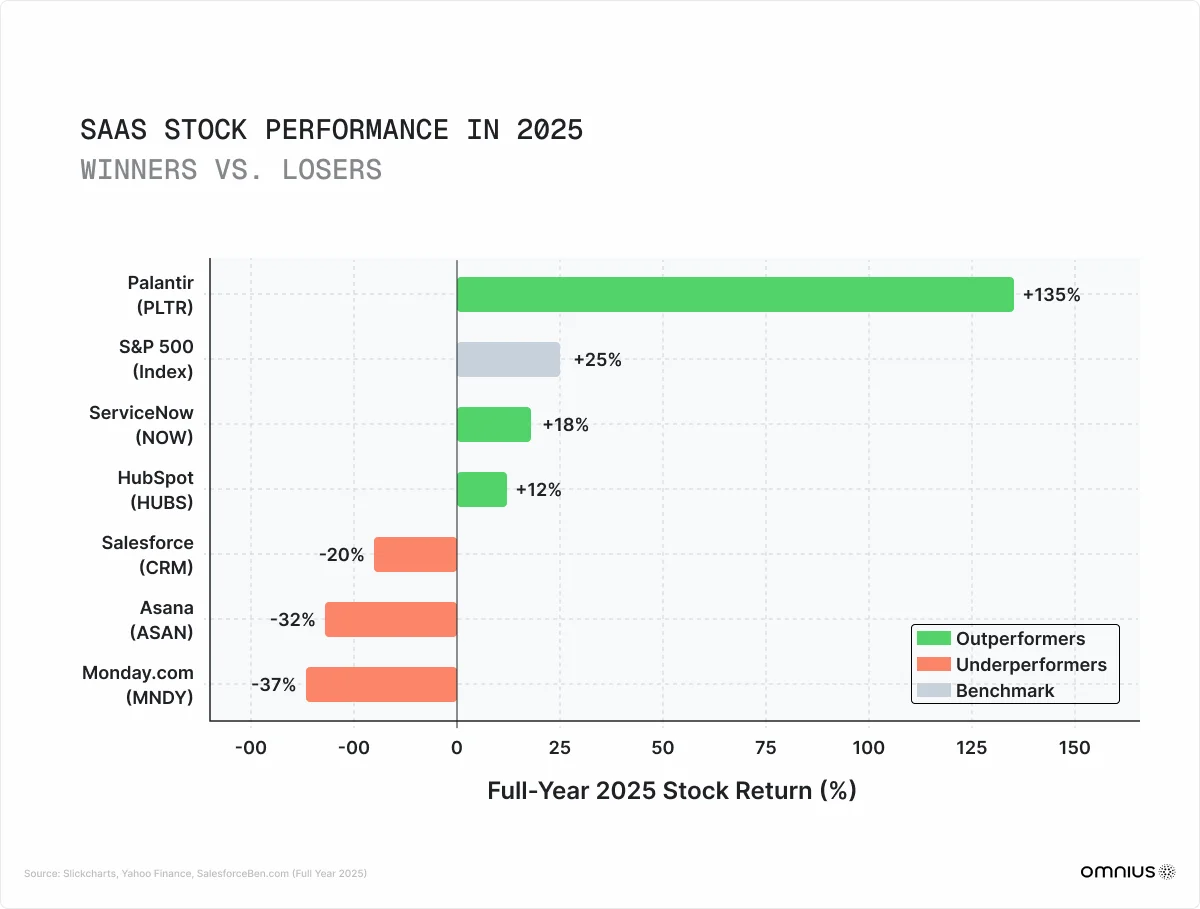

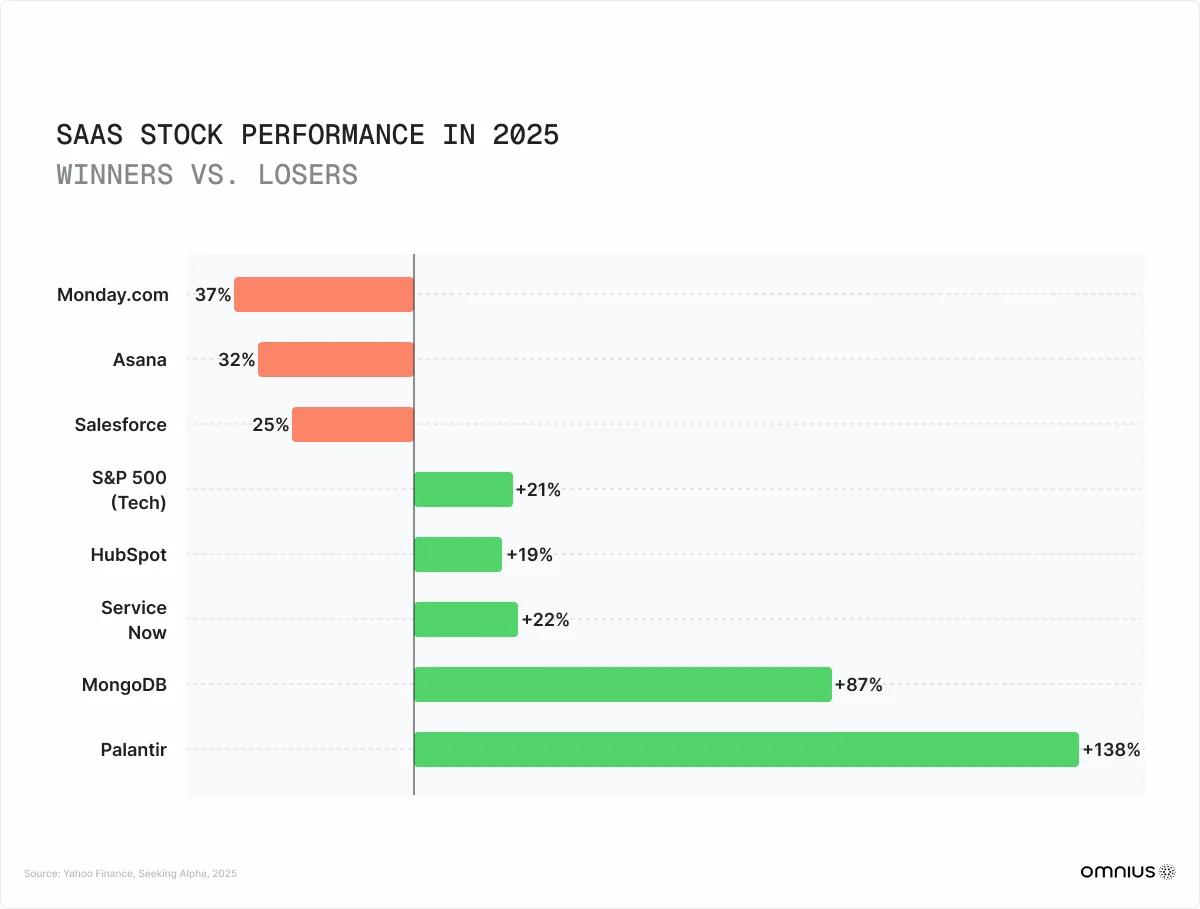

Palantir Technologies delivered the most significant media narrative of the year, posting historic market performances that proved the immense enterprise appetite for AI systems. Palantir's stock surged an incredible 135% in 2025, making it the top-performing stock in the S&P 500.

This growth was driven by the great adoption of its Artificial Intelligence Platform, which allowed enterprises to build custom applications directly on top of their operational data.

Salesforce faced a sharp market correction, with its stock dropping approximately 25% over the year. Despite investing in the marketing of Agentforce, the CRM leader suffered decelerating revenue growth as enterprise customers started to delay implementations, skeptical of the immediate ROI.

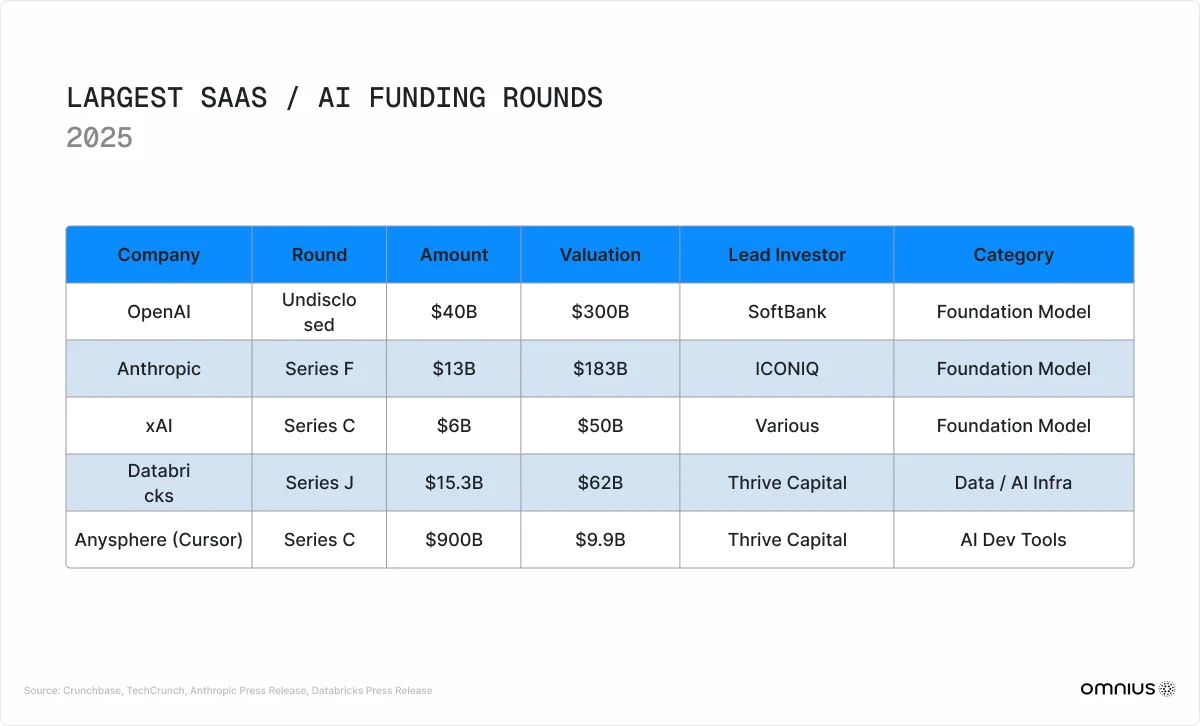

In the private markets, Anthropic made headlines by completing a staggering $13 billion Series F funding round in September 2025. This injection of capital brought the company's post-money valuation to $183 billion. This followed a $3.5 billion Series E earlier in the year, highlighting the unprecedented concentration of capital flowing into foundational AI models.

Over the past year, a combination of Google’s algorithm updates and the rollout of AI Overviews has completely changed how users search. As answers began appearing directly within search results, the need to click through to blog content declined sharply. For many established SaaS companies, this exposed a heavy reliance on broad, top-of-funnel content that was no longer driving meaningful traffic.

Based on Omnius’s analysis of SaaS portfolios, companies built around this model experienced an average decline of 72% in organic blog traffic in 2025. This wasn’t a temporary but a structural change - one that is forcing the industry to reconsider how customer acquisition through organic channels actually works.

Watch for in 2026:

The market is no longer buying promises of future AI capabilities. Investors and enterprise buyers are demanding immediate, measurable workflow automation. If your AI features do not allow a customer to demonstrably reduce headcount or increase output within days, they are viewed as a cost center, not a value driver.

2. SaaS Growth Rate, Churn, and Pricing Benchmarks in 2025

The underlying mechanics of SaaS growth changed, and expansion is now significantly slower and harder to achieve than during the zero-interest-rate anomaly of the early 2020s. The median SaaS growth rate has steadily compressed over the past several years.

In 2021, the median growth rate sat at a robust 30%. This compressed to 17% in 2023, dropped to 14% in 2024, and finally settled at just 12% in 2025. Furthermore, net new annual recurring revenue across public SaaS companies dropped 29% year-over-year, falling to $1.65 billion in the first quarter of 2025.

SaaS has become the default operating layer for modern enterprises, but at scale, it’s created significant complexity. The average company now manages around 275 SaaS applications, and as CFOs take a closer look, they’re finding that nearly 53% of licenses are unused or underutilized. What once drove efficiency is now quietly driving waste.

Because of this, organizations are actively consolidating redundant tools. The average number of SaaS applications used per mid-market company has dropped from 112 in 2023 to 106 in 2024, and this consolidation trend accelerated through 2025.

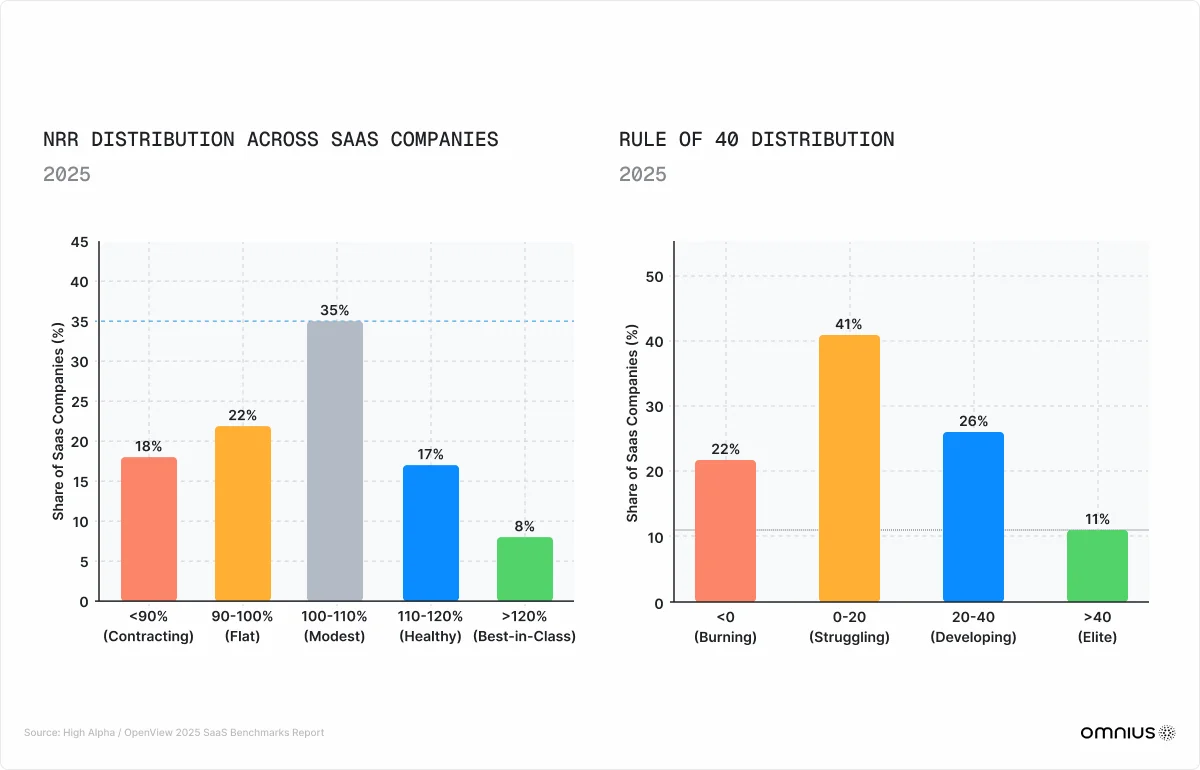

To combat churn, companies are focusing more on Net Revenue Retention (NRR). The median NRR for SaaS companies in 2025 is 106%, while the median "Rule of 40" score (growth rate plus profit margin) sits at a dismal 11% to 12%.

Resolving the Data Tension:

These two metrics - 106% NRR and 11% Rule of 40 - might seem contradictory, but they tell a highly coherent story of a market under pressure. A 106% median NRR means the average company is barely expanding its existing customer base, netting just 6% of its revenue from expansion. This is far below the 120%+ NRR required for compounding, efficient growth. Combined with compressed top-line growth rates, the resulting Rule of 40 score of 11–12% reflects a market where most companies are growing slowly and investing more to maintain that meager growth, leaving almost no room for profitability.

Pricing models also underwent a transformation. By 2025, approximately 85% of SaaS companies had adopted usage-based or hybrid pricing models, up from roughly 30% in 2019. Seat-based pricing is structurally misaligned with the future of work. If your software makes a customer's employees 50% more efficient, allowing them to reduce their team size, a seat-based pricing model means you lose revenue for delivering a better result.

Watch for in 2026:

Transitioning to usage-based pricing (billing by API calls, compute, or transactions) is no longer optional; it is an existential requirement. We see a rise in "Outcome-Based Pricing," where vendors guarantee specific business results (e.g., a guaranteed percentage increase in lead conversion) and take a percentage of the financial upside, moving entirely away from software access fees.

3. Top SaaS Companies in 2025: Winners vs. Losers

The top SaaS companies in 2025 split into two distinct camps: platforms that successfully monetized AI, and legacy incumbents that failed to adapt. The winners showed that when your product actually fits how modern enterprises work, growth follows.

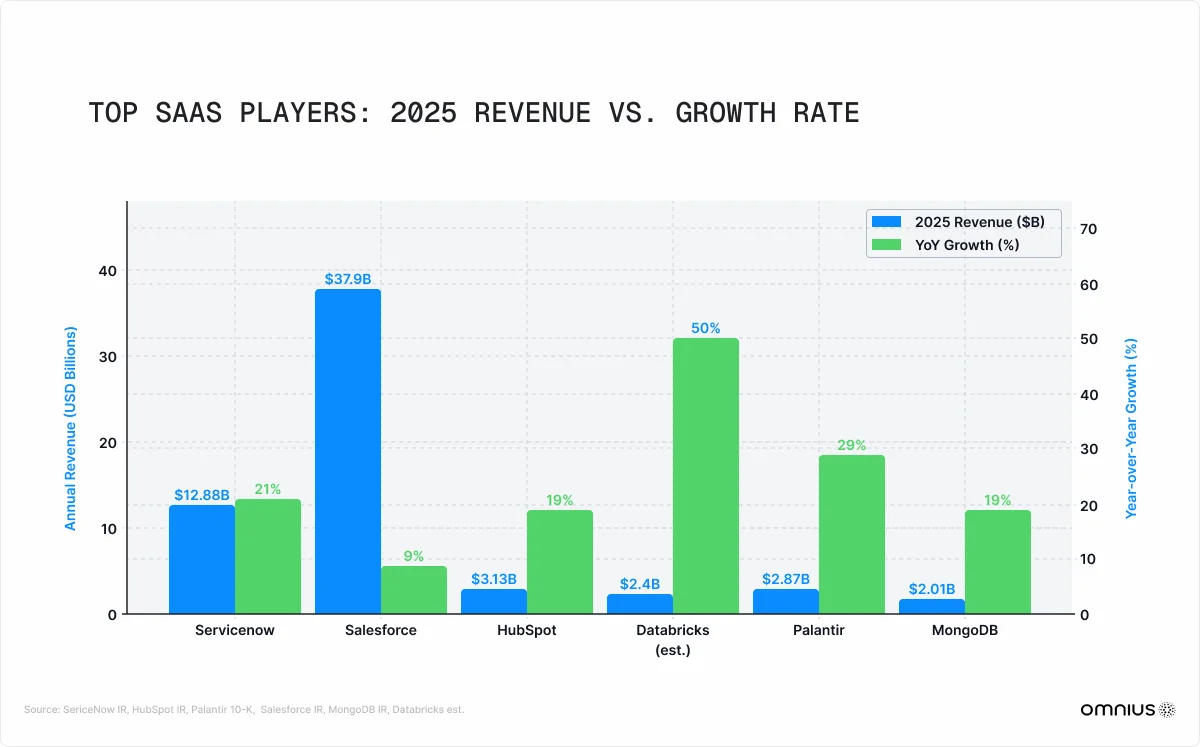

ServiceNow is a strong example of an incumbent that adapted well to the shift toward AI. The workflow automation giant reported subscription revenues of $12.88 billion for the full-year 2025, representing a highly impressive 21% year-over-year growth. By adding its fifth major product line and crossing the $1 billion revenue threshold in multiple categories, it proved that enterprises are willing to consolidate their operations onto comprehensive platforms that demonstrably improve efficiency.

HubSpot also demonstrated resilience, reporting annual revenue of $3.13 billion for 2025, an increase of 19% from the previous year. While the company faced significant challenges regarding top-of-funnel content marketing, its core CRM and marketing automation platform remained sticky among mid-market customers.

However, the defining story of 2025 was the rise of Palantir and MongoDB.

Palantir’s US commercial business became a clear blueprint for how enterprises are actually adopting AI in practice.

At the same time, MongoDB was positioned exactly where the shift was happening. Its document-oriented architecture fits naturally with the unstructured, high-volume data that AI applications generate. As a result, every new AI workload customers deployed directly increased their usage - and their spend.

That’s what made the difference.

With a consumption-based pricing model, growth wasn’t forced - it compounded. As customers scaled their AI workloads, their revenue scaled, ultimately driving a valuation of roughly 12× forward sales.

On the other side of the spectrum, broad horizontal productivity tools suffered.

Companies like Asana and Monday.com saw their stock prices decline by 32% and 37%, respectively. When enterprise customers audited their software spending, they frequently found multiple overlapping project management tools that accomplished similar tasks.

Watch for in 2026:

The moat of “workflow familiarity” is gone. Enterprises are no longer sticking with tools just because they’re used to them. As switching costs have dropped, companies are aggressively consolidating their stacks. If your product isn’t directly tied to revenue or clear cost savings, it’s exposed, especially as bundled alternatives from Microsoft or ServiceNow become harder to justify against.

What follows is predictable. We expect a wave of M&A across the horizontal productivity space, with mid-tier project management and collaboration tools getting acquired at steep discounts by larger platform players expanding their ecosystems.

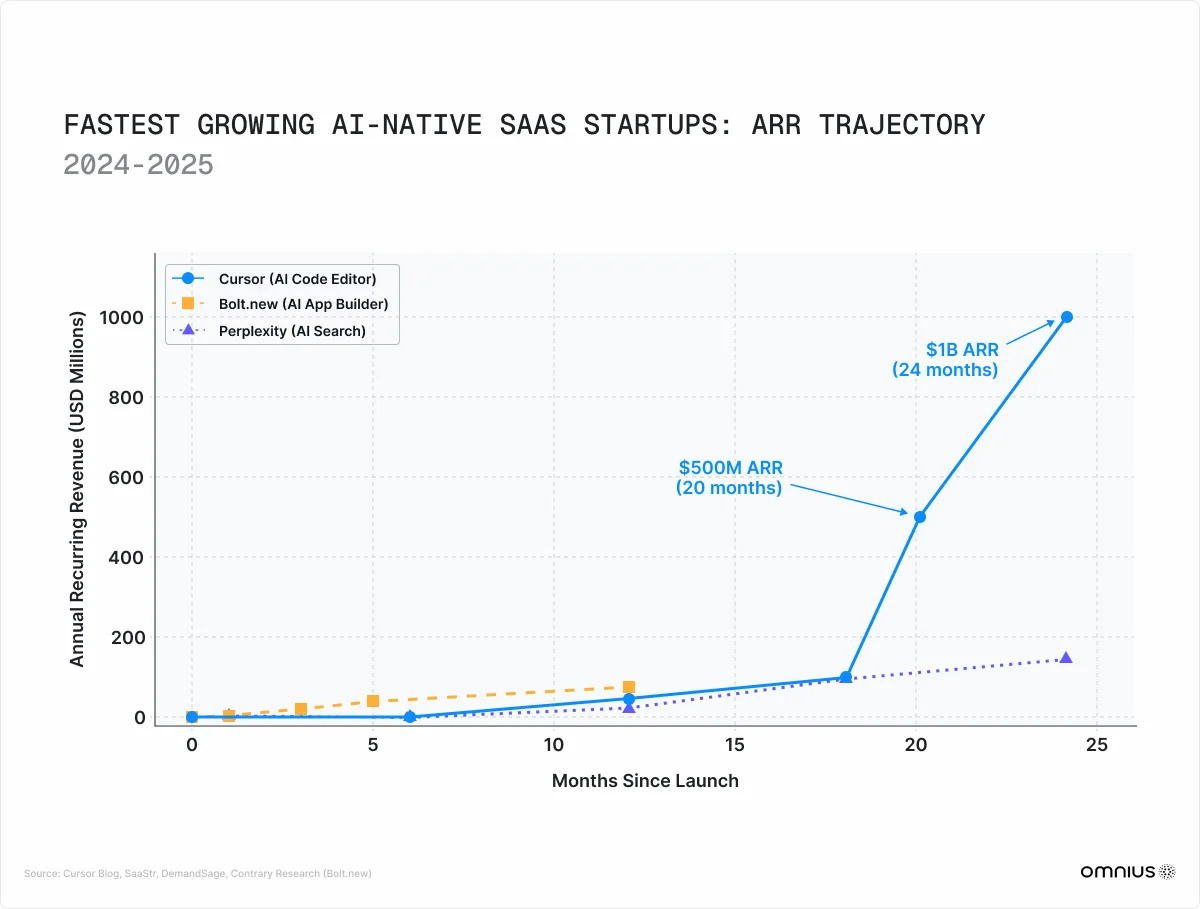

4. Fastest Growing SaaS Startups in 2025: Cursor, Perplexity & the New PLG

While established companies fought for single-digit growth improvements, a new generation of startups scaled at unprecedented speeds. These fast-growing companies bypassed traditional enterprise sales motions entirely, relying instead on developer-led adoption and evolved product-led growth (PLG) strategies.

Cursor, the AI-powered code editor, was arguably the fastest-growing startup of the year. The company reached $500 million in annualized revenue in mid-2025, doubling its revenue every two months. Cursor grew entirely through developer adoption without a traditional sales or marketing team.

Supabase grew its user base to 1.7 million developers. The company successfully executed a developer-first go-to-market strategy, maintaining a generous free tier that allowed engineers to prove value before asking for payment.

Workato represents a different archetype - enterprise-led rather than developer-led - but its growth confirms the same underlying dynamic: companies that reduce integration complexity between fragmented SaaS tools are capturing budget that previously went to consolidation projects.

These startups succeeded by evolving the PLG playbook. Instead of hiding core features behind strict paywalls, they delivered substantial value upfront. Companies that implemented this generous free-tier model typically saw conversion rates of 5% to 15%, far higher than the 1% to 3% common in traditional freemium models.

Watch for in 2026:

Developer-led growth is consistently outperforming traditional, top-down enterprise sales. When end-users - developers, designers, analysts - can adopt a tool on their own, prove its value, and integrate it into their daily workflows without ever speaking to sales, the enterprise deal becomes a formality, not a negotiation.

Now, that model is evolving. With the rise of “agentic PLG,” AI agents acting on behalf of users can discover, test, and recommend tools automatically, completely changing how self-serve funnels are built and how software gets adopted.

5. Biggest SaaS Categories in 2025: Systems of Action vs. Record

In 2025, the core philosophy of enterprise software shifted from Systems of Record to Systems of Action. Historically, massive categories such as CRMs, ERPs, and HR databases served simply as digital filing cabinets.

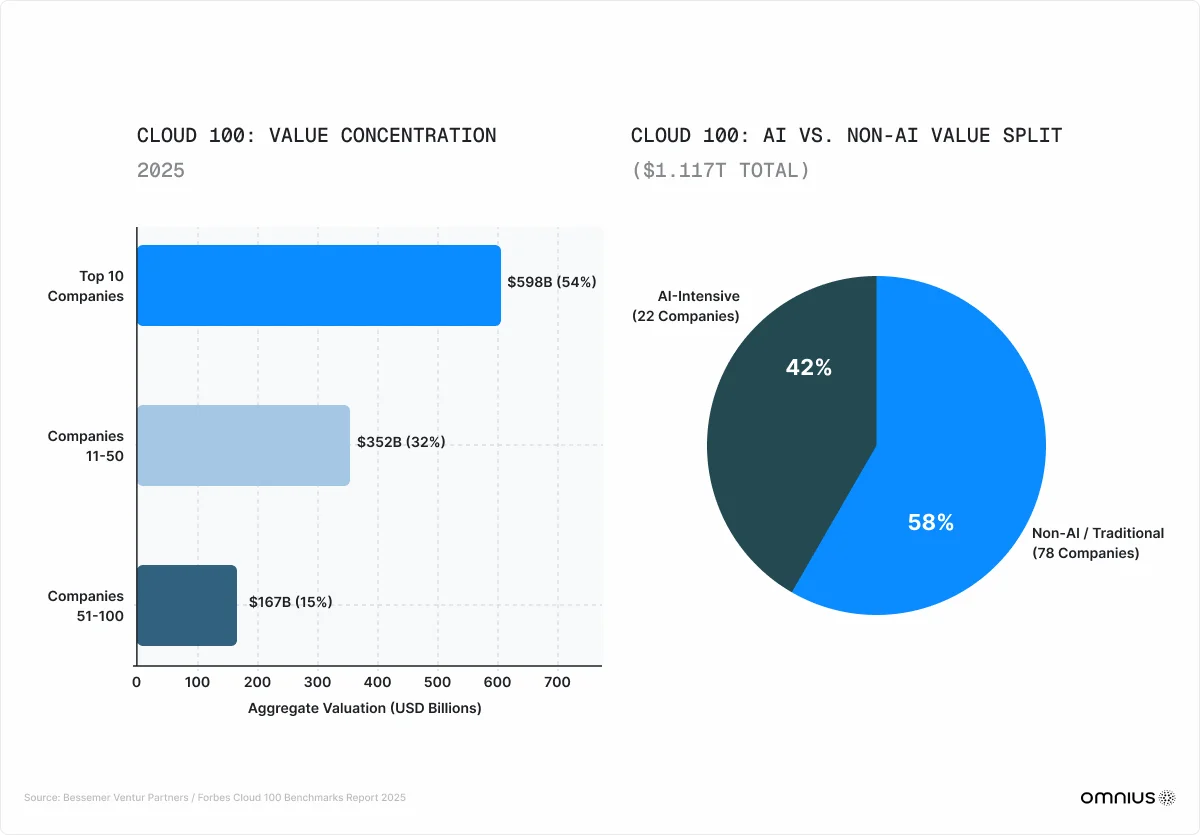

The Bessemer Venture Partners Cloud 100 Benchmarks Report for 2025 highlighted this concentration of value. The aggregate valuation of the Cloud 100 reached a record $1.117 trillion, up approximately 36% from 2024. However, this wealth was highly concentrated. The top 10 companies on the list held 54% of the total value, representing roughly $598 billion.

AI was the undeniable heavyweight category. AI-intensive companies captured $464 billion in value - representing 42% of the total Cloud 100 list value, despite accounting for only 22 of the 100 companies. These AI leaders achieved average revenue multiples of 24x, compared to just 19x for non-AI companies.

Watch for in 2026:

Building another digital filing cabinet is a dead end. Investors won’t fund it, and enterprises won’t buy it. Software is no longer expected to just store data - it needs to actively participate in how the business runs. The next generation won’t rely on manual data entry. It will monitor communication channels on its own, keep records up to date automatically, and execute follow-ups without waiting on humans.

6. Fastest Growing SaaS Categories in 2025: Vertical, AI-Native & Fintech

While broad horizontal categories stagnated, specialized sectors experienced amazing growth. AI-native SaaS and Vertical SaaS were the undisputed leaders, driven by increasing demand for advanced technologies and highly specific industry solutions.

Vertical SaaS companies - those building software for specific industries like healthcare, legal, or construction - proved to be 1.5 to 3.3 times more likely to become financial outliers compared to horizontal platforms. The vertical SaaS market is projected to expand at a 16.3% CAGR.

A note on market share definitions: Vertical SaaS is projected to reach approximately $317 billion by 2032, which. While this represents roughly a 28% share of the projected $1.13 trillion SaaS market. This concentration reflects the category's aggressive CAGR and the fact that specialized industry solutions are rapidly cannibalizing the budgets previously allocated to generic horizontal tools.

For example, the healthcare vertical generated the highest revenue per customer of any category. These platforms understood HIPAA compliance, insurance billing, and clinical workflows at a granular level. Consequently, sales and marketing spend for healthcare SaaS companies dropped by 83%.

Another massive growth driver within vertical SaaS was embedded fintech. In 2025, 39% of vertical SaaS companies offered embedded financial capabilities, with payments representing 30% of that functionality. By integrating payment processing directly into their operational software, these companies created additional revenue streams and dramatically increased switching costs.

Watch for in 2026:

Niche is the new scale. By focusing on a specific vertical, companies can build deeper, more essential workflows that generic competitors cannot match. Furthermore, adding embedded fintech (payments, lending, payroll) can even triple the average revenue per user (ARPU) without requiring additional customer acquisition costs.

We expect to see the emergence of "Micro-Vertical SaaS", hyper-specialized tools targeting sub-sectors (e.g., software specifically for pediatric dentistry rather than general healthcare), powered by AI that makes building bespoke software economically viable.

7. SaaS Venture Capital in 2025: AI Funding & Revenue Multiples

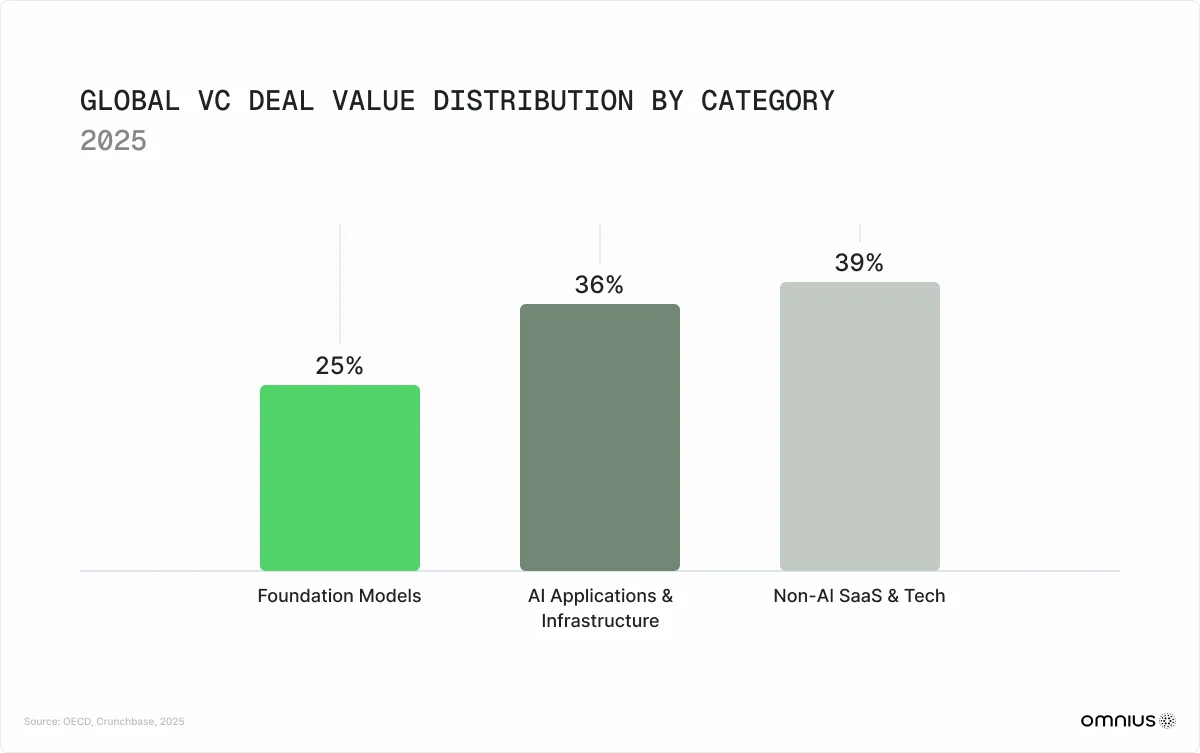

The 2025 SaaS VC landscape was defined by extreme concentration. Global VC projections reached $490 billion, but capital was highly selective, rewarding AI-native architectures while starving traditional software.

By the end of 2025, AI companies attracted an astonishing 61% of all VC deal value, despite representing only 37.5% of the total deal count. The average deal size for an AI company doubled from $17.2 million to $35.9 million. Foundation model builders like OpenAI and Anthropic absorbed 40% to 50% of all AI funding, acting as massive gravitational wells for global capital.

For non-AI software companies, the funding environment was far more challenging. Venture and private equity funds sit on an estimated $500 billion in undeployed capital originally earmarked for software investments, raised during the 2020–2022 cycle when SaaS multiples were at their peak.

A lot of this capital is now stuck. AI is absorbing most new investment, the IPO window is still effectively closed for anything that isn’t top-tier, and the secondary market for private SaaS equity has become much thinner.

In other words, there are fewer ways out and fewer buyers. The median revenue multiple for private SaaS businesses compressed to a 7–10x range of annual recurring revenue, down from 15x+ at the 2021 peak.

Watch for in 2026:

If you’re not building with AI-native architecture, you’re competing for a rapidly shrinking pool of venture capital. At the same time, over $500B in undeployed capital is putting pressure on VCs and private equity firms to either invest or return funds. That’s turning them into active buyers of consolidation plays. If you can’t reach profitability or restart growth, the most likely outcome isn’t a big exit - it’s a discounted sale to a PE-backed roll-up.

And this is just the beginning. A wave of “zombie SaaS” recapitalizations is coming. Companies that raised at 2021 valuations but are now stuck at $10M–$20M ARR will be pushed into down rounds or forced asset sales as their runway runs out.

8. SaaS Marketing in 2025: The Rise of GEO

SaaS marketing had to evolve in 2025. The content marketing engine that powered the industry for years started losing efficiency, pushing companies to rethink distribution and find new ways to capture demand.

The primary catalyst for this collapse was the arrival of the zero-click search era. By the end of 2025, 58% of all Google searches ended without a single click to an external website. Google's rollout of AI Overviews reduced click-through rates.

Simultaneously, Google's algorithm updates heavily penalized sites that built massive traffic through broad, top-of-funnel informational content with no value. The search engine's strict enforcement of its E-E-A-T framework decimated traditional SaaS blogs.

With SEO yielding diminishing returns, LinkedIn thought leadership emerged as the primary channel for B2B SaaS marketing. Founder-led content outperformed traditional brand marketing by 2 to 3 times on engagement metrics.

Watch for in 2026:

The era of outsourcing growth to junior writers producing generic listicles is over. Today, distribution is earned through real insight. If your marketing doesn’t bring a contrarian view, proprietary data, or deep, tactical expertise, it gets ignored - by both algorithms and actual buyers.

This is where the shift is happening. The next wave is “data as marketing.” The strongest SaaS companies will turn anonymized product usage into original research, creating content that AI can’t fabricate and competitors can’t replicate.

9. The Main Category: Generative Engine Optimization (GEO)

Beyond the limitations of traditional SEO, 2025 marked the emergence of a new, clearly defined discipline: Generative Engine Optimization (GEO). Where SEO focused on ranking within a list of blue links, GEO focuses on being cited, summarized, and recommended by AI-powered answer engines - such as Google’s AI Overviews, Perplexity AI, ChatGPT, and Claude AI.

The goal hasn’t disappeared - it’s transitioned from visibility through clicks to visibility through answers.

The mechanics of GEO differ from SEO, because AI answer engines do not rank pages; they synthesize information from sources they recognize as authoritative, current, and structurally clear. This means that the SEO levers - keyword density, backlink volume, and domain authority - have limited influence over whether a brand appears in an AI-generated answer.

Instead, GEO actually rewards structured data, direct factual claims with clear attribution, original research, and consistent brand mentions across multiple independent sources.

For SaaS companies, this shift has immediate commercial implications. A company that ranks first on Google for "best CRM for startups" but is never mentioned in an AI Overview or Perplexity answer is effectively invisible to a growing segment of buyers who begin their research with an AI query rather than a search engine.

More and more B2B buyers are starting their research using AI tools instead of Google. Based on Omnius data, around 18–24% of early-stage research (when people are just exploring options) already comes from AI platforms.

This was measured by:

- Tracking traffic coming directly from those tools

- Asking users how they found the product

And the key part: that percentage is growing every month.

The companies that are winning in GEO in 2025 share three characteristics:

- They publish original, citable data (like benchmark reports and proprietary surveys).

- They maintain consistent, factually accurate brand descriptions across their website, press releases, and third-party review platforms.

- They structure their content with clear, direct answers to specific questions rather than long-form narratives designed to maximize time on page.

Watch for in 2026:

GEO is not a replacement for SEO - it is a parallel discipline that requires a different content strategy. The single highest-leverage investment a SaaS company can make in 2026 is publishing one piece of original, data-backed research per quarter. Each report becomes a permanent citation source for AI engines, compounds in authority over time, and generates the kind of inbound links that improve both traditional SEO and GEO simultaneously.

Google will introduce dedicated AI Overview visibility metrics within Google Search Console, formally establishing GEO as a trackable acquisition channel and rendering third-party rank trackers obsolete for top-of-funnel measurement.

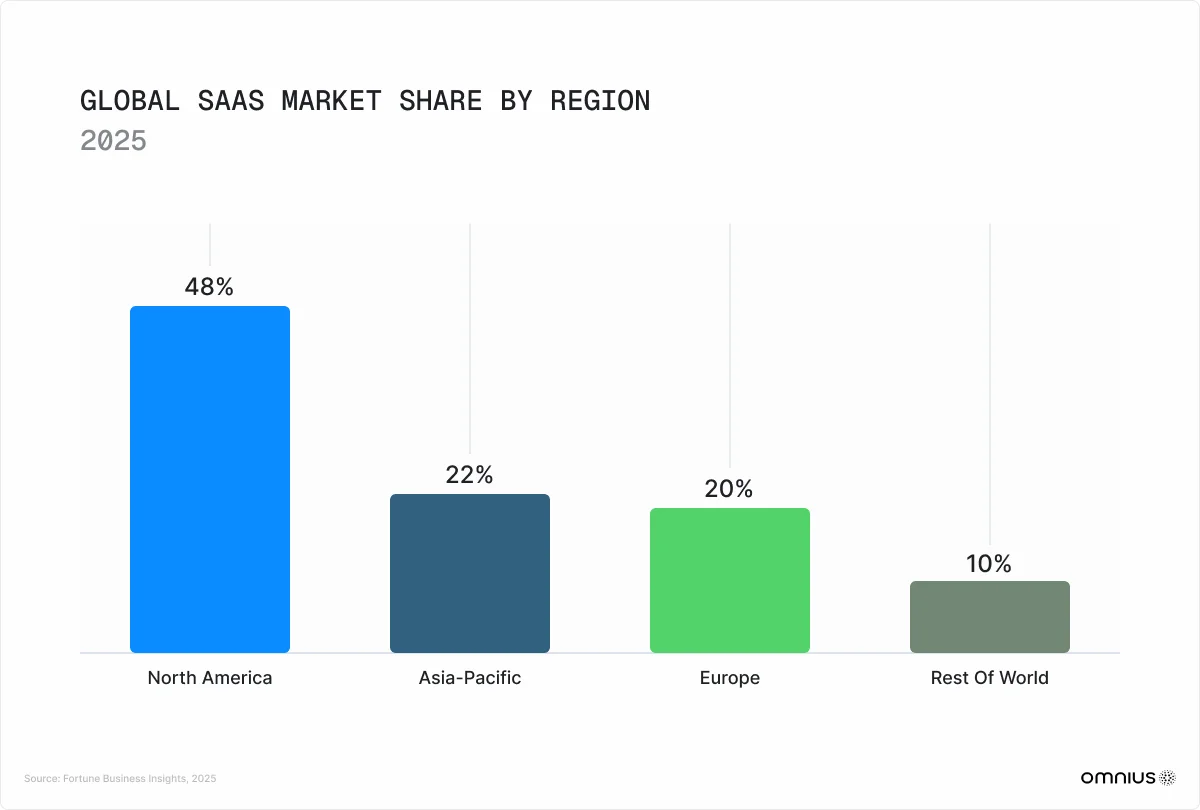

10. Geographical Data: SaaS Market Size by Region in 2025

While North America remains the dominant force in the global SaaS ecosystem, the market has become increasingly multi-polar. Regional regulation, infrastructure build-outs, and capital availability strongly influenced scaling in 2025.

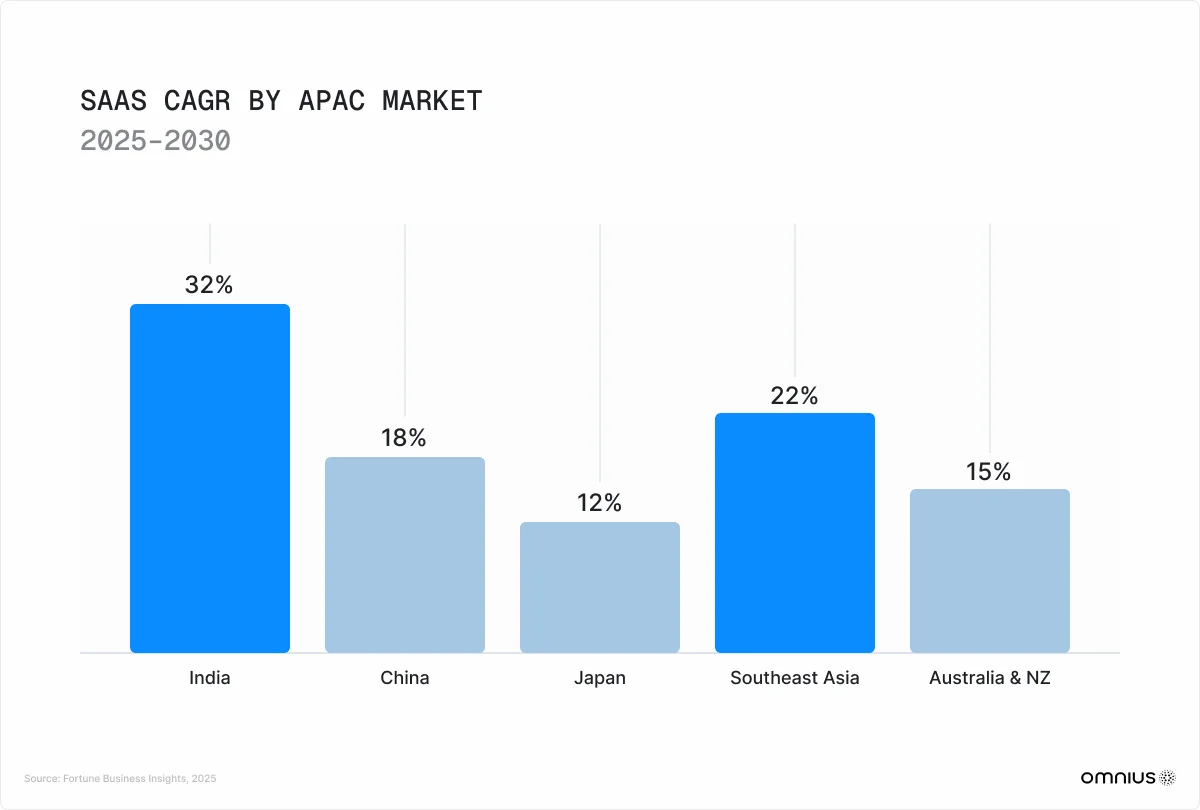

North America retained the largest market share, accounting for approximately 48% of global SaaS revenue. However, this market is highly mature, and growth rates have stabilized compared to other regions. The Asia-Pacific (APAC) region recorded the highest growth rates globally, expanding at a projected CAGR of 16.1% to 22%. Driven by massive domestic markets and rapid cloud infrastructure expansion, APAC represented approximately $69 billion of the global market in 2025 (roughly 22% of the $315.68 billion baseline).

APAC's absolute market size is expected to approach $86 billion by the end of 2026, up from approximately $69 billion in 2025 - a ~25% single-year jump that is consistent with the upper bound of the stated range. India, for example, stood out as a hyper-growth market, expanding at a staggering 30% to 35% CAGR.

Europe maintained a steady, moderate growth trajectory, capturing roughly 20% of the global market. European growth was heavily driven by vertical SaaS, HR tech, and finance tools, largely spurred by complex regulatory requirements and strict data-sovereignty laws like GDPR.

Compliance-driven software, like data governance, consent management, and privacy infrastructure, is growing much faster than the rest of the European SaaS market, roughly at double the pace. This is mainly due to regulation. As enforcement of GDPR and the EU AI Act increases, companies are being forced to upgrade their systems, turning compliance into a mandatory investment, not a choice.

France is a strong example of this. Its SaaS market is expected to grow from €4.75 billion to over €11 billion by 2030, fueled by government-backed cloud initiatives and a rapidly maturing startup ecosystem.

Latin America, the Middle East, and Africa represent the next frontier for SaaS expansion, though data coverage for these regions remains limited. Available projections suggest these markets are transitioning from early adoption toward enterprise SaaS usage, with Brazil and the UAE leading their respective regions. Readers should treat projections for these geographies as directional rather than precise, since third-party research coverage is materially thinner than for North America and Europe.

Watch for in 2026:

North America is still the most competitive - and most expensive - place to acquire customers.

So if you’ve already found product-market fit there but haven’t expanded into APAC, especially India, you’re likely missing your biggest growth opportunity. India is growing at 30–35% year over year, driven by rapid digital transformation and much lower customer acquisition costs compared to Western markets.

At the same time, regulation is starting to reshape where and how companies operate. The EU AI Act will require AI and SaaS companies to localize parts of their infrastructure within the EU. If they don’t, they risk losing access to the market. That shift will benefit European cloud and AI infrastructure providers and will likely trigger a wave of acquisitions, as US companies buy their way into compliance instead of building from scratch.

Conclusion

The era of growth-at-all-costs is over.

The expectations placed on software companies regarding product quality, measurable outcomes, and economic discipline are higher than ever. The companies that are winning operate in defined vertical categories, embed AI deeply into their workflows, maintain good net revenue retention, and communicate clear, outcome-based value to buyers. Those that remain broad, undifferentiated, or inefficient face severe pressure in renewals, pricing, and market valuation.

For founders and revenue leaders planning their next phase of growth, the mandate is clear: do fewer things, but do them significantly better. Narrow your ideal customer profiles, go toward usage-based pricing models that align with customer value, and use AI to execute real business processes rather than treating it as a surface-level marketing feature.

Those are not temporary disruptions - it is a reconfiguration of how software is built, sold, and valued. The companies that will define the next 10 years of SaaS are already operating by these new rules: they are AI-native and ruthlessly focused on measurable outcomes. The ones still operating by the rules of 2019 are not in a slow decline; they are in a fast one.

.png)

.svg)

.svg)