The question is no longer whether AI will transform search. It already has.

Based on recent industry insights, reports, and industry-expert tests, we’ve created a comprehensive analysis of how AI search is reshaping consumer discovery, brand visibility, and the $750 billion revenue opportunity - synthesizing data from McKinsey, Graphite/Similarweb, SparkToro/Datos, Define Media Group, SISTRIX, Chartbeat, Ahrefs, and Harvard/OpenAI research into a single GEO report for 2026.

Here are some of the most crucial insights that are influencing the SEO/GEO industry in 2026:

- 50% Consumers use AI-powered search

- 45B monthly AI sessions worldwide

- $750B US revenue at stake by 2028

- 20-50% of traditional traffic is at risk due to AI-related changes

Why This Report Cannot Wait (Executive Summary)

According to recent reports, Google now shows AI summaries in around 50% of all queries and is projected to rise to 75%+ by 2028. ChatGPT alone shares nearly 20% of global search traffic when mobile and web usage are properly combined.

Meanwhile, Google referral clicks to publisher websites have collapsed by as much as 60% for small sites, and organic traffic across professional publisher portfolios is down 42% since AI Overviews launched.

This happens because AI summaries keep users on Google rather than sending them to sites, hitting informational content the hardest.

For businesses, this creates an urgent and paradoxical challenge. Consumers are searching more than ever. Total search volume, combining traditional engines and AI, increased by 26% globally since 2022 (ChatGPT launch), but the internet has been completely changed.

Visibility now requires a completely different practice focused on Generative Engine Optimization (GEO), multi-platform presence, and the understanding that search happens not just on Google and ChatGPT, but across Amazon, YouTube, Reddit, X, TikTok, Instagram, and dozens of other platforms.

Here are the core arguments every business must internalize going into 2026:

- AI search is large, fast-growing, and mobile-first - not a niche experiment.

- Traditional search is flat, not dying, and the pie is getting bigger, not shrinking.

- Google's AI Overviews are affecting the decrease of the organic traffic - a 42% decline is already on record.

- Search is an everywhere behavior: Amazon, YouTube, and Bing each outpace ChatGPT on desktop.

- GEO is not optional - only 16% of brands currently track AI search performance systematically.

Biggest news

To understand where search is heading, these are the numbers to help you during this process:

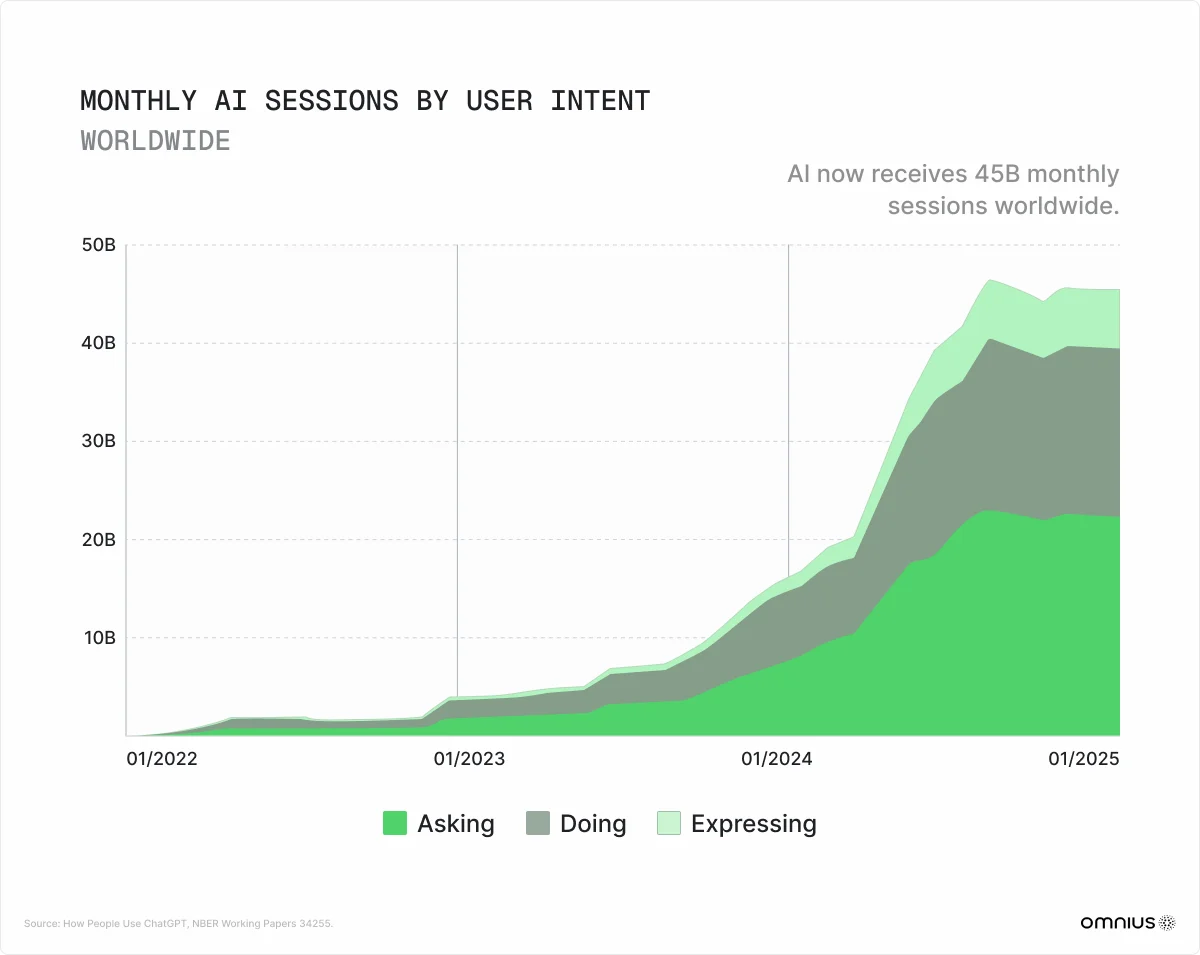

- AI now receives 45 billion monthly sessions worldwide

- Total search volume has increased 26% globally since ChatGPT launched

- The "No-Click" Era Dominates: Over 80% of Google searches end without a click to a website, with AI Overviews, powered by Gemini, contributing to the decline in organic traffic, with a record 42% decline.

- GEO Over SEO: Generative Engine Optimization (GEO) has become a primary marketing function, with over 20-30% of traditional SEO budgets shifting to AI search optimization.

- Hyper-Personalization: AI systems now create "nested learning" models, resulting in unique, highly personalized answers for every user, making a single "best page" concept obsolete.

- Trust and Citations Over Clicks: AI models prioritize reputable, authoritative sources, shifting the focus to digital PR, expert-driven comparison data, and brand mentions.

- Emergence of Specialized Tools: The GEO tool market has exploded, with specific platforms attracting over $96M+ (Profound) in funding and focusing on AI citation alerts and sentiment tracking.

- Profound, an AI-powered marketing platform focused on Answer Engine Optimization (AEO), reached unicorn status with a $1 billion valuation in February 2026.

- The leading AI search platforms in Q1 2026 include ChatGPT (dominant share), Perplexity (leading citation rates), and Google Gemini.

The AI Search Top Investments That Happened

The AI search ecosystem is bifurcated into two distinct player categories: LLM platforms that power consumer and enterprise AI search, and GEO/AEO tools that help you measure and optimize your visibility on those platforms (such as our tool Atomic does as well).

The capital flowing into AI search and infrastructure is not a speculative bubble. It is a structural commitment by the largest technology companies and institutional investors on earth. Understanding the investments here can help you contextualize the speed and permanence of the transition your business must navigate.

Here are the headline investment figures:

- $211B - Total AI sector funding 2025

- 50% - Share of global VC captured by AI in 2025

- ~$400B+ - Hyperscaler capex committed to AI infrastructure 2025

- $189B - Funding in February 2026 alone (record month)

Biggest Players: LLM Platforms

February 2026 became the largest single month of startup funding ever recorded at $189 billion globally, driven by OpenAI ($110B), Anthropic ($30B), and Waymo ($16B).

While concentration in three companies accounted for 83% of that capital, the broader signal is clear: institutional investors are treating frontier AI infrastructure as a new asset class comparable to sovereign wealth allocation, not traditional venture capital.

Sources: Crunchbase, AI Funding Tracker, Forge Global, company announcements, Q1 2026

The AI search companies are rapidly transitioning from venture-backed startups to the largest public companies in human history. OpenAI is targeting a $1 trillion IPO in Q4 2026. xAI-SpaceX is targeting June 2026 at up to $1.5 trillion - potentially the largest public offering in history.

The place for brands to establish early GEO positions before these companies are fully established is narrowing.

Biggest Players: GEO/AEO Tools

A new software category has emerged to help brands measure and optimize AI search visibility. The market is consolidating rapidly, with Profound emerging as the enterprise leader and a cluster of mid-market and specialist tools serving different segments.

The Peec AI funding is particularly significant for the marketing industry: a $21M Series A specifically raised for Answer Engine Optimization confirms that GEO/AEO has crossed the threshold from marketing practice to investable business category. Capital follows markets, and capital is following GEO.

Here are the numbers in more detail:

Understanding AI search and what’s happening with it can help you improve your presence and use its benefits more effectively.

1. The True Scale of AI Search

Bigger, faster, and more mobile than any prior estimate suggested

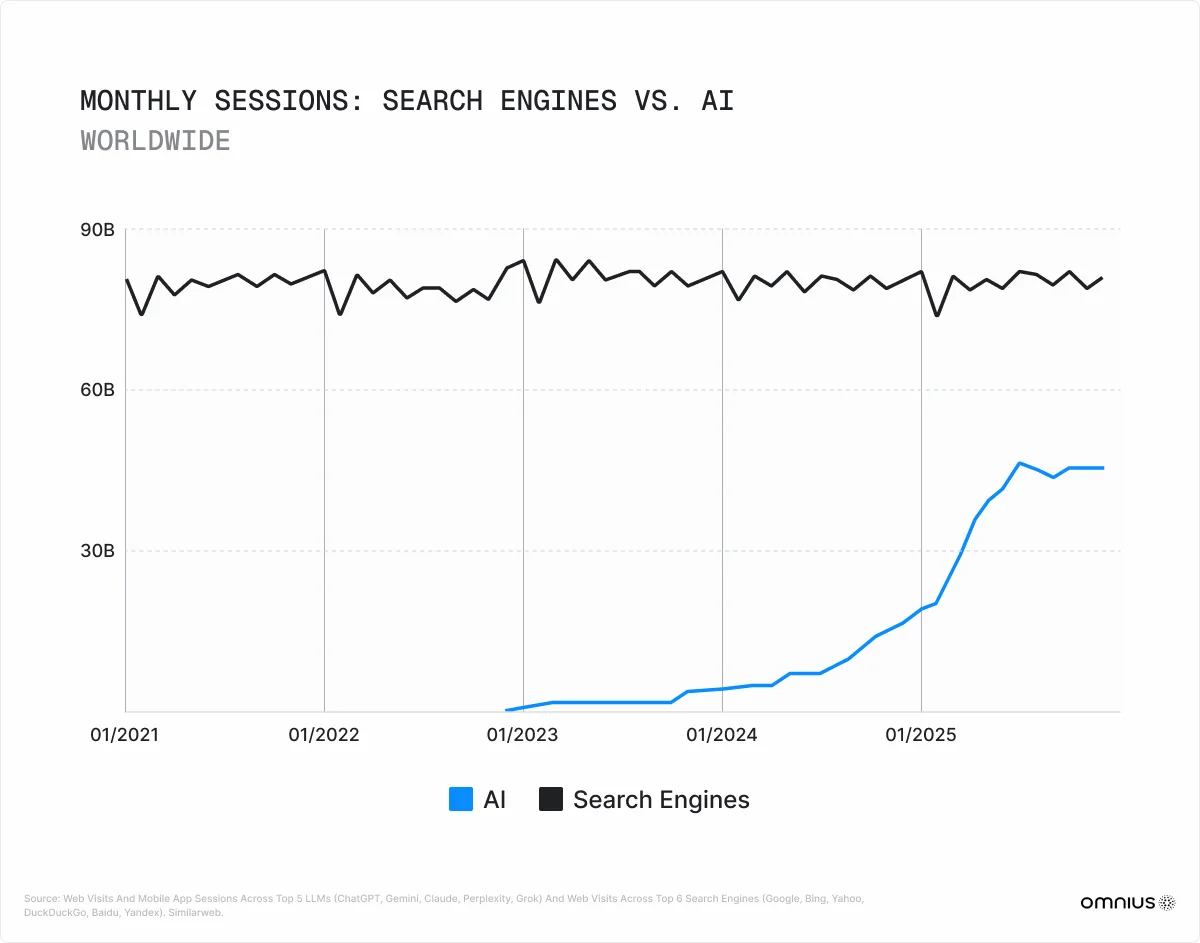

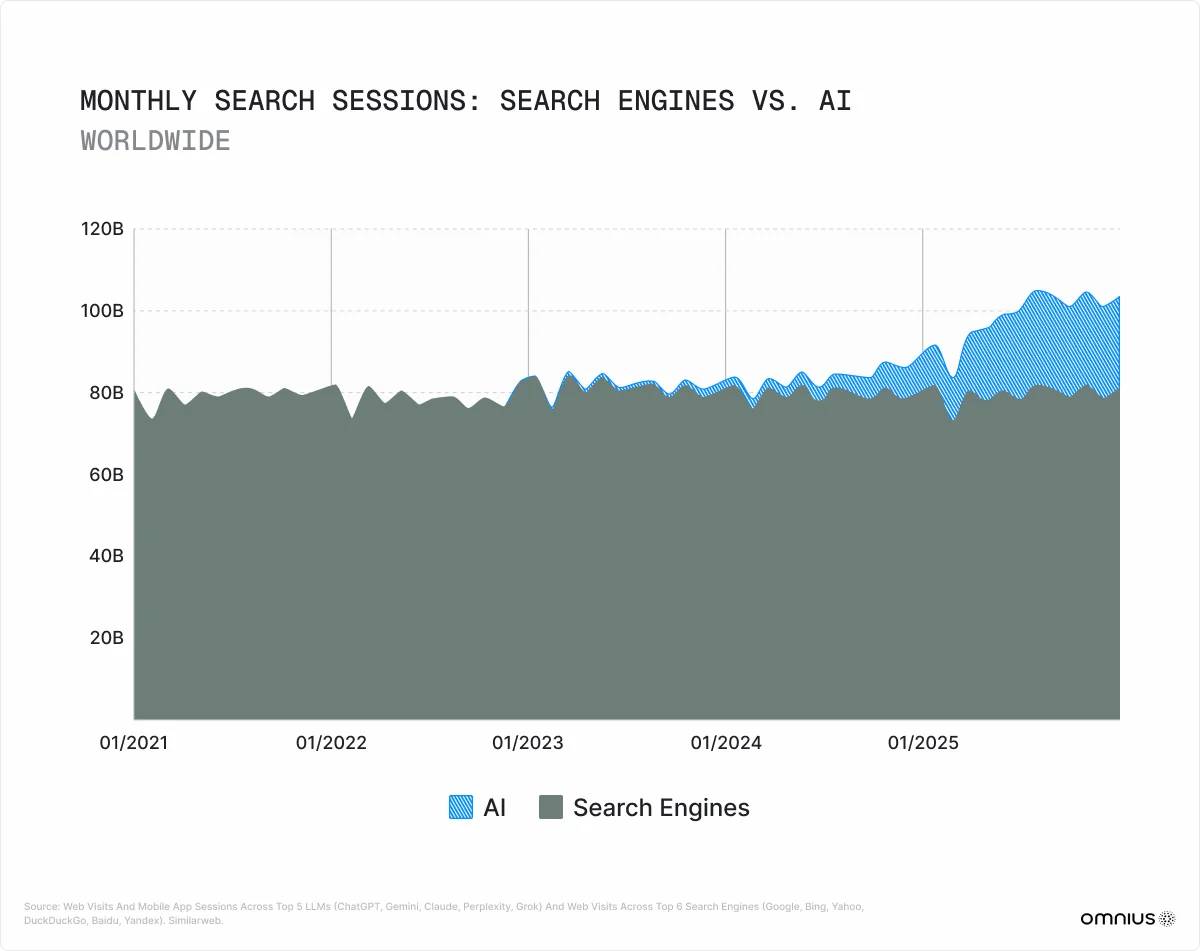

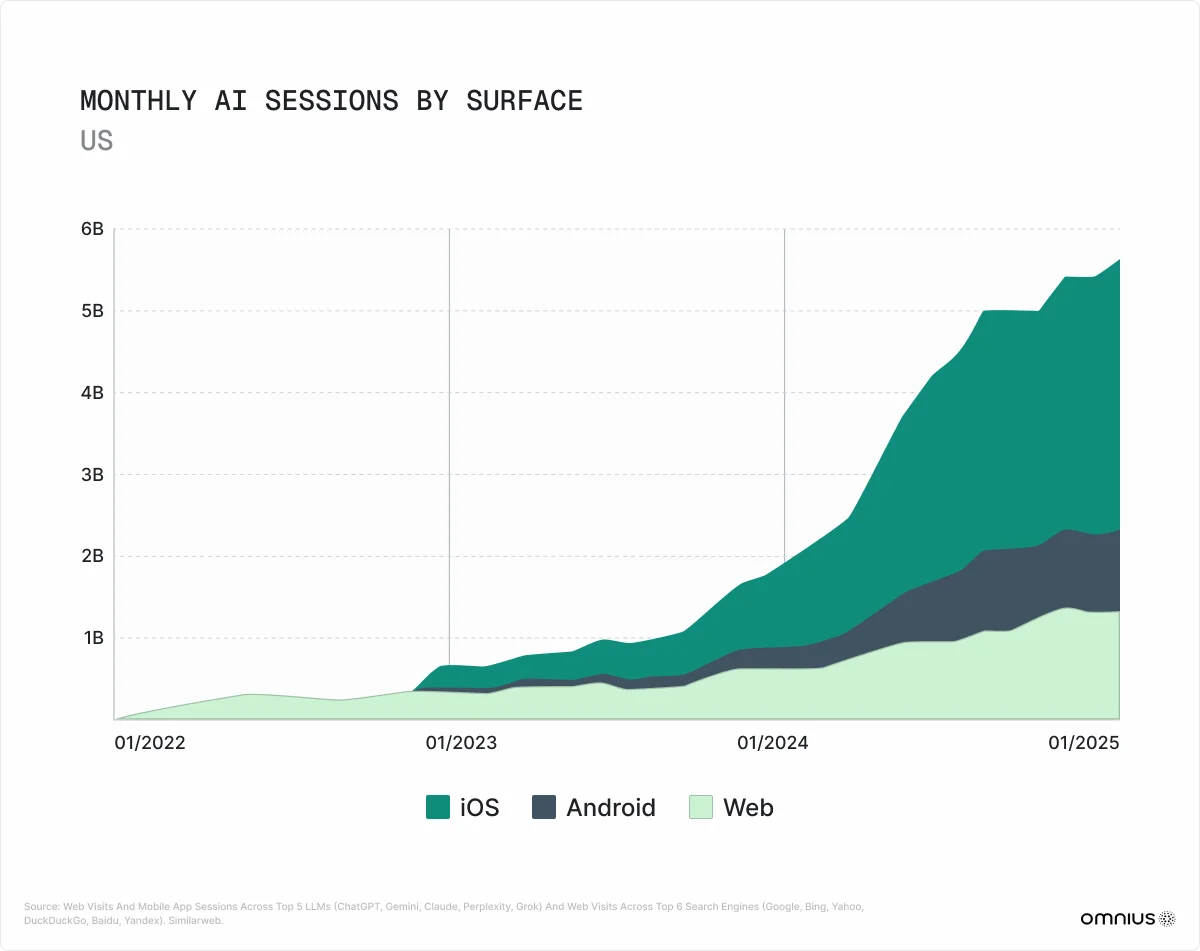

When AI analysts first compared ChatGPT to Google, they relied exclusively on desktop web traffic data, a methodology that missed 83% of actual AI usage on mobile apps. However, Graphite.io and SimilarWeb corrected this blind spot and found that AI now receives 45 billion monthly sessions worldwide, representing 56% of all search engine sessions globally and 34% in the United States.

In the US, AI usage alone grew 300% YoY between December 2024 and December 2025, proving that the zero-sum narrative is empirically wrong. Critically, total search volume, combining traditional engines and AI, has increased 26% globally since ChatGPT launched, confirming that AI is a great addition, not a cannibalistic source of traffic.

The explosive growth from 2024 onward reflects mobile app adoption being captured in the data.

From near-zero in late 2022, AI sessions reached the scale of a major search engine competitor in under three years, a trend that even mobile apps, the previous fastest-adopted technology, did not match.

For businesses, this is the baseline: AI is not emerging, it has emerged already.

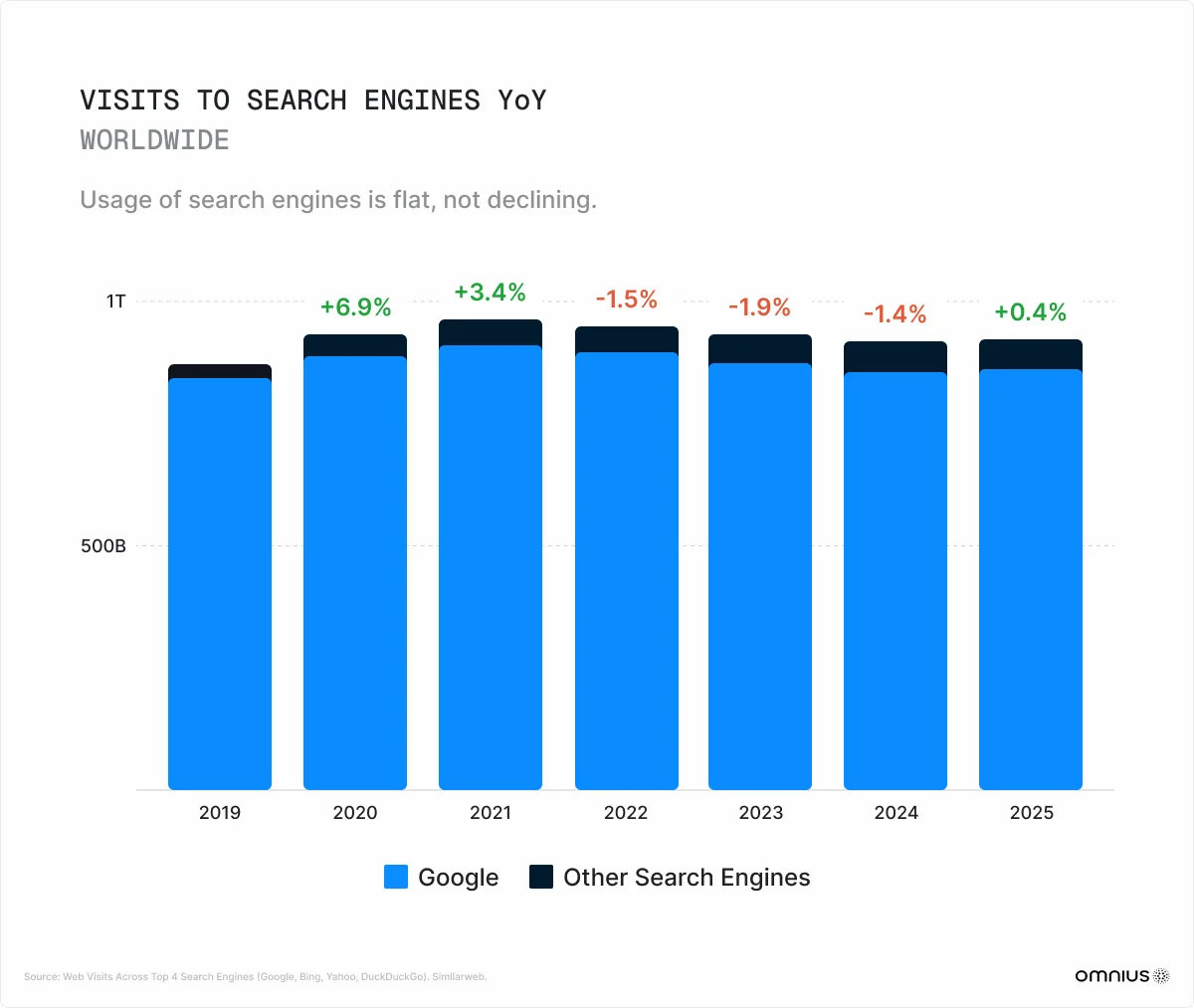

The search engine growth trend has been essentially flat for five years, hovering between 70B and 80B monthly sessions, while AI has stacked on top as a new, incremental layer. Brands that position their strategy as “AI versus Google” are asking the wrong question.

The right question is:

Where am I visible across the now-larger total discovery ecosystem?

The year-on-year data is a critical stabilizing anchor.

A six-year flat trajectory definitively debunks the “search is dying” narrative.

Despite years of headlines predicting Google’s imminent collapse, aggregate search engine visits have not declined, as you can see within the SimilarWeb’s study:

The modest 2022–2024 dips are consistent with pandemic-era comparisons, not structural decay. What has changed is share distribution within an expanded total, which is precisely where brand visibility strategy must now focus.

Key insight: Even with this growth, roughly 48% of AI prompts are “Doing” or “Expressing” tasks, not search. When adjusted for search-equivalent “Asking” prompts only, AI commands 28% of global search sessions, still a historic market share shift that no brand can ignore.

2. The Search Market Share Realignment

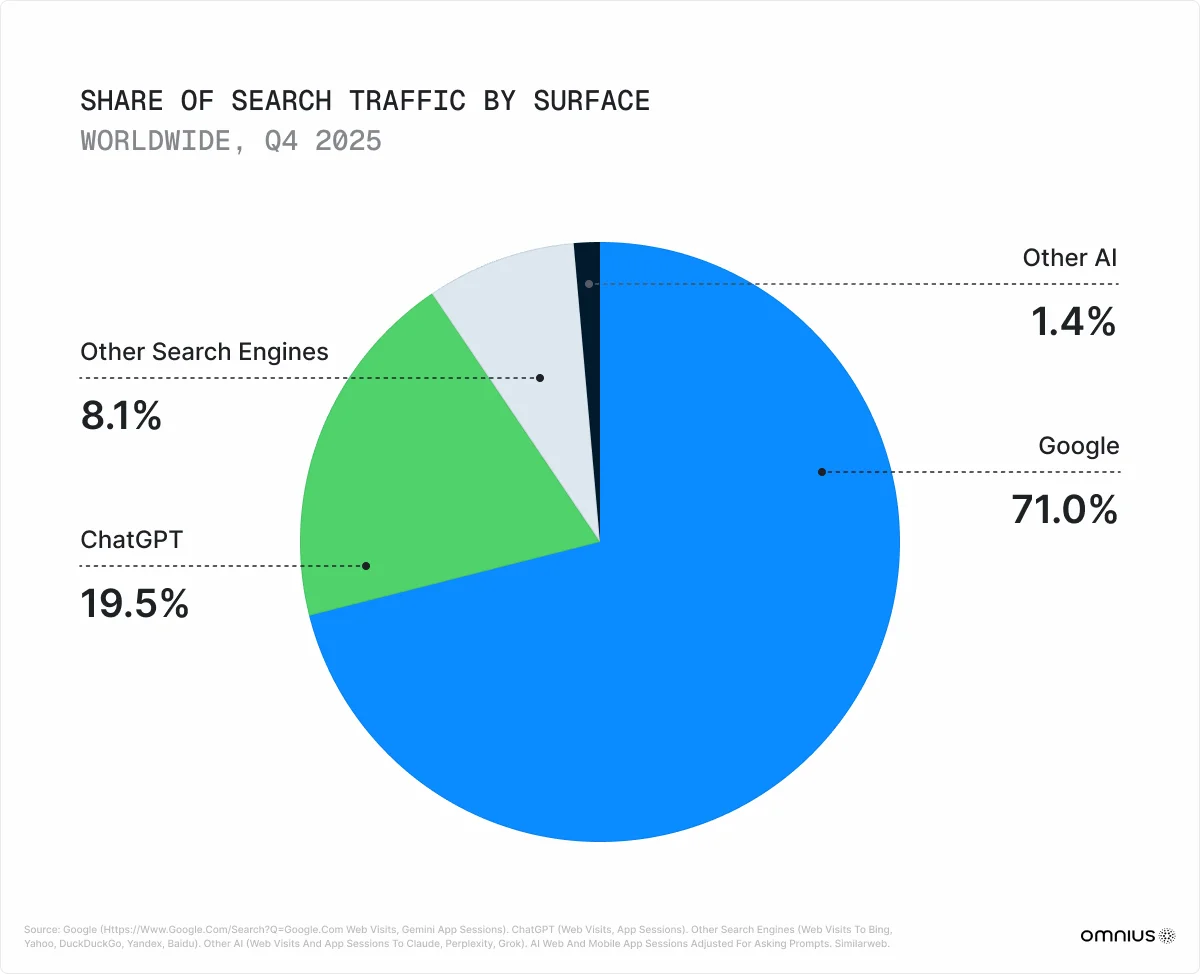

For the first time in a decade, Google's grip on discovery is genuinely loosening

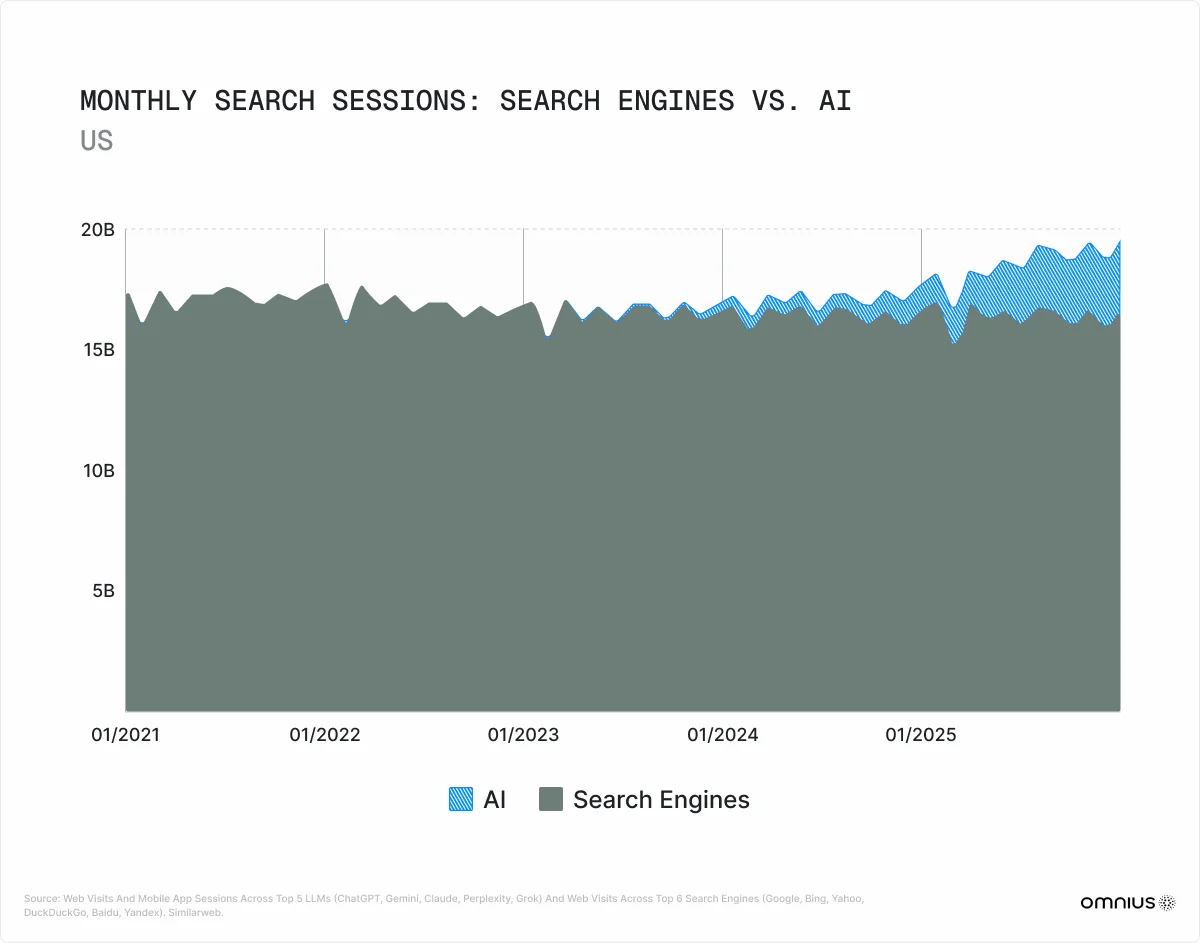

Google’s global search traffic share fell from 89% in 2023 to 71% by Q4 2025, an 18% decline in two years. ChatGPT, adjusted for search-relevant “Asking” prompts only, now commands 19.5% of global search traffic and 12.3% in the US. These figures were previously understated by 4x to 5x because prior analyses excluded mobile app usage, which represents 83% of all AI interactions.

ChatGPT’s global share (19.5%) is significantly higher than its US share (12.3%), driven by faster AI adoption in emerging markets across Asia, Latin America, and Africa where users are leapfrogging traditional search behavior entirely.

For global businesses, this signals that an international GEO strategy is even more urgent than US-focused planning.

The trend chart shows a consistent, accelerating structural shift across 2024 and 2025.

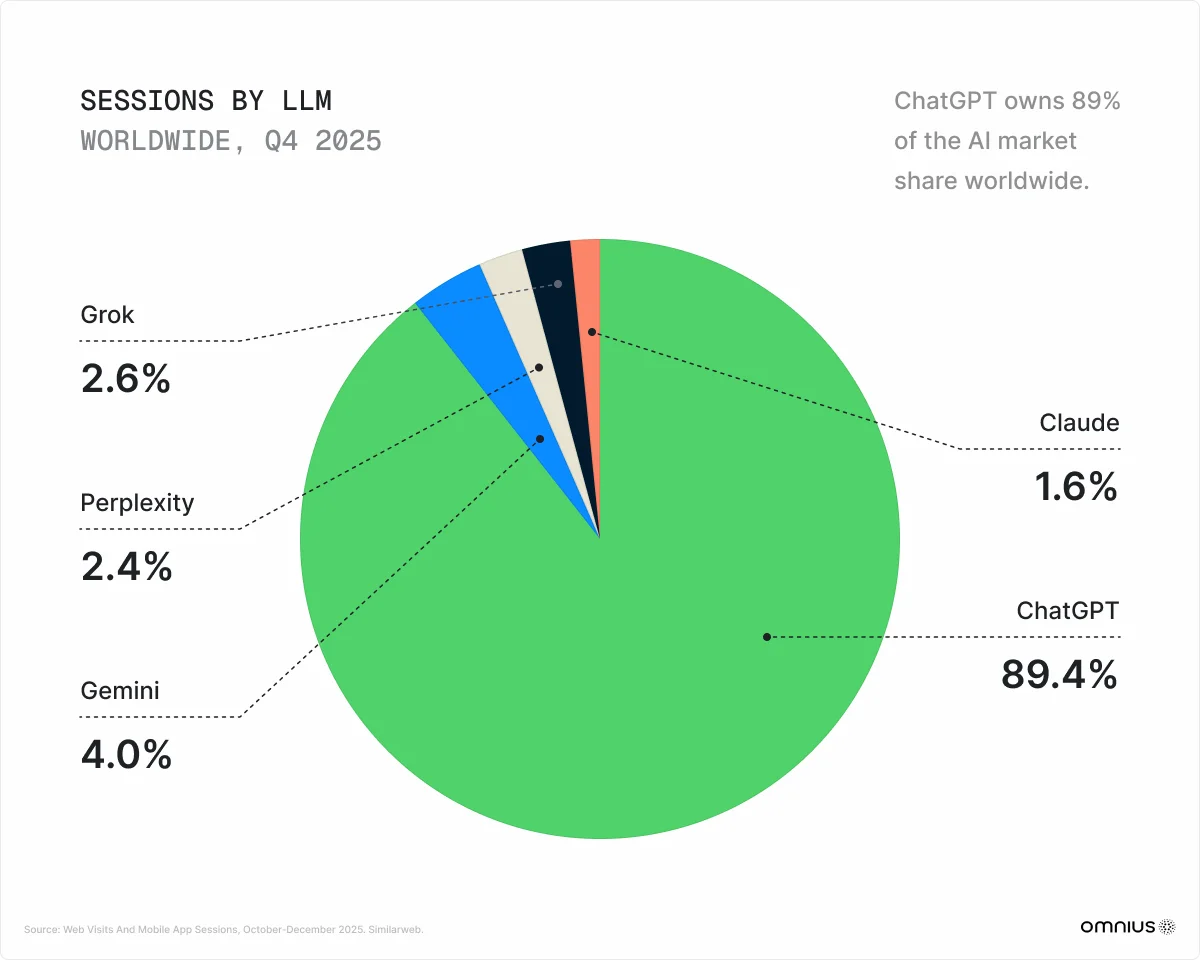

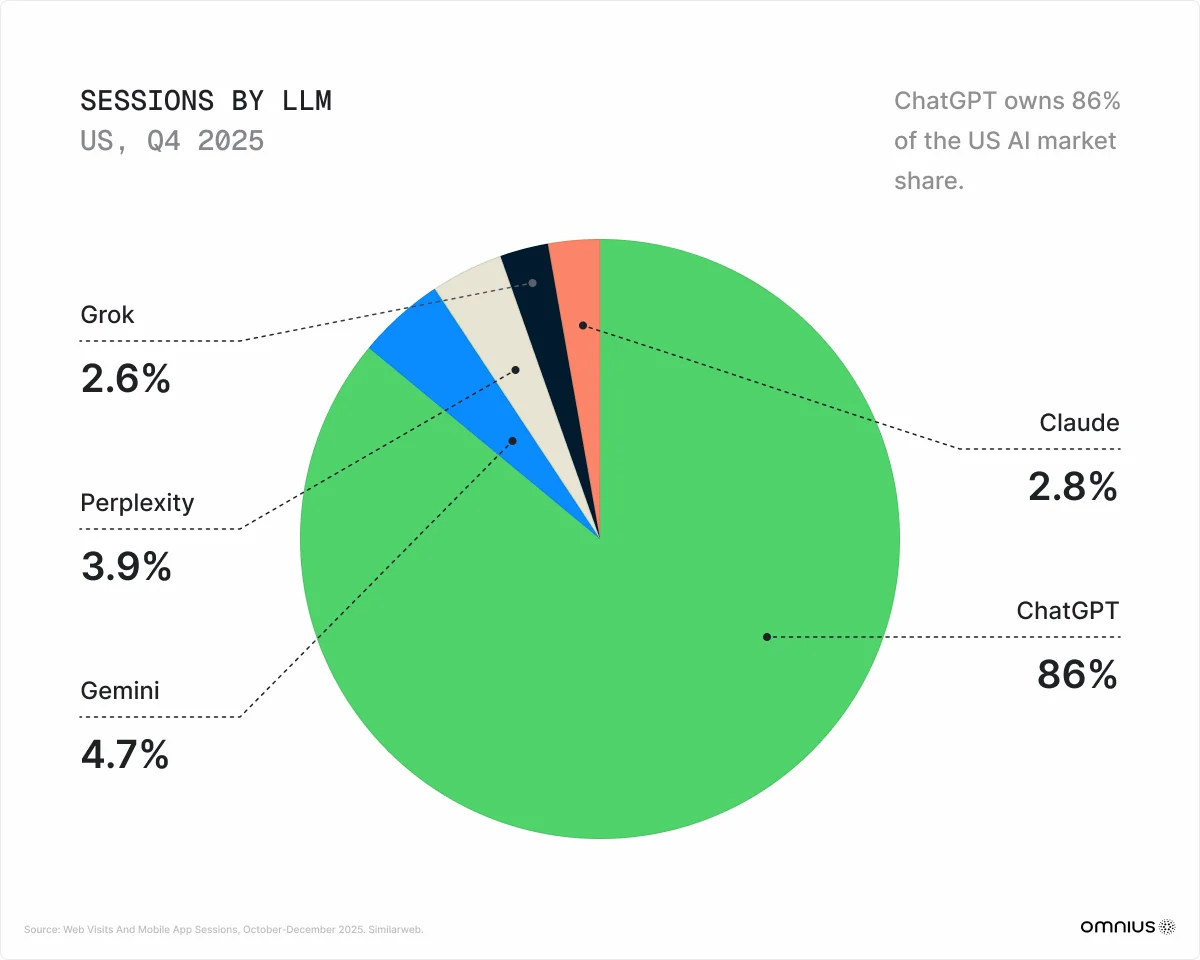

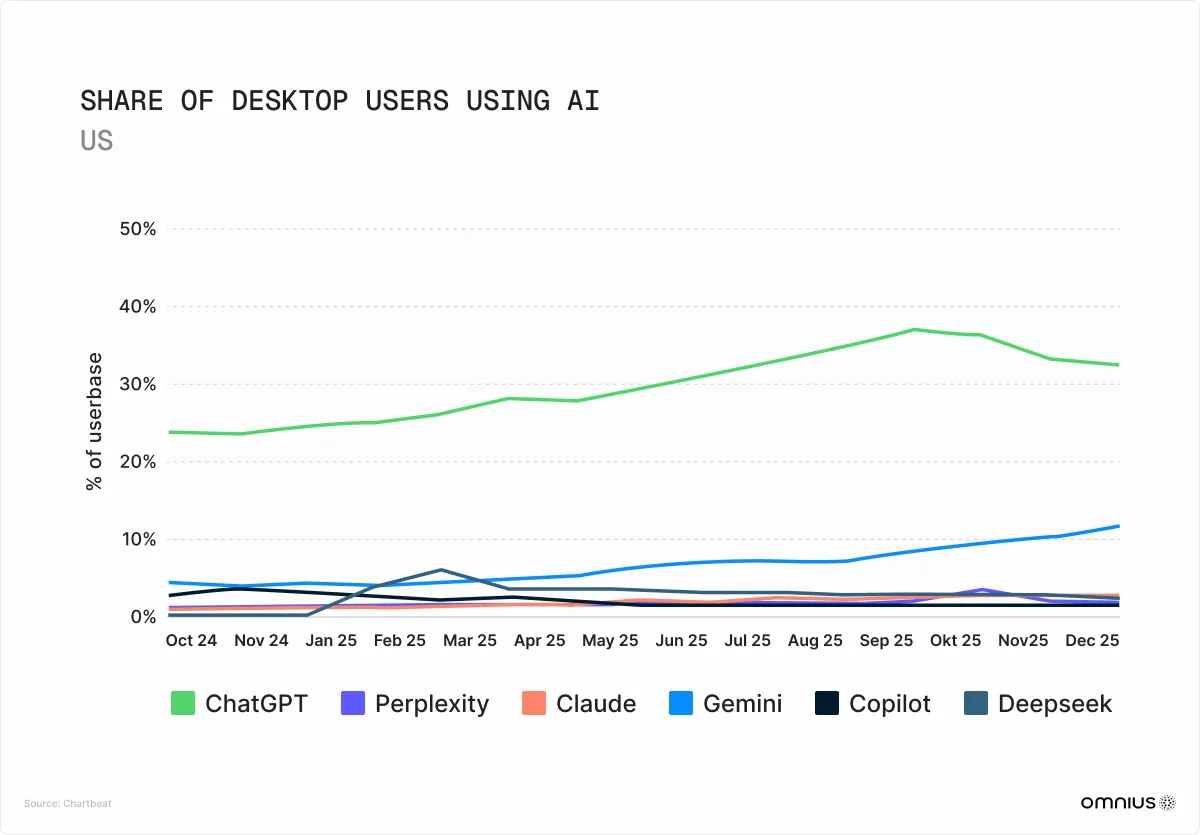

The trend of change has not slowed. Within the AI segment itself, ChatGPT maintained near-monopoly dominance - 89.4% of worldwide AI sessions.

Here’s how it looks when it comes to the US - the results are pretty much the same, with ChatGPT covering 86% in the US:

However, Gemini’s trajectory deserves close attention: at 11.2% of US desktop AI users by December 2025 and deeply integrated into Google’s search, Chrome, and Android infrastructure, it is the only AI product positioned to leverage an existing distribution moat comparable to Google’s own.

Multiple experts predicted that Google would overtake ChatGPT’s AI chat market share within 12 to 18 months.

And we’ve already started seeing this coming true - During January, and upon the launch of Gemini 3, it continued to take the market share with more than 22% share during February ‘26, up from 19.5% 1 month ago, according to SimilarWeb:

Key insight: Google lost 18% of its global search traffic share in 24 months. No comparable incumbent has lost this much search market share this quickly in the Internet era.

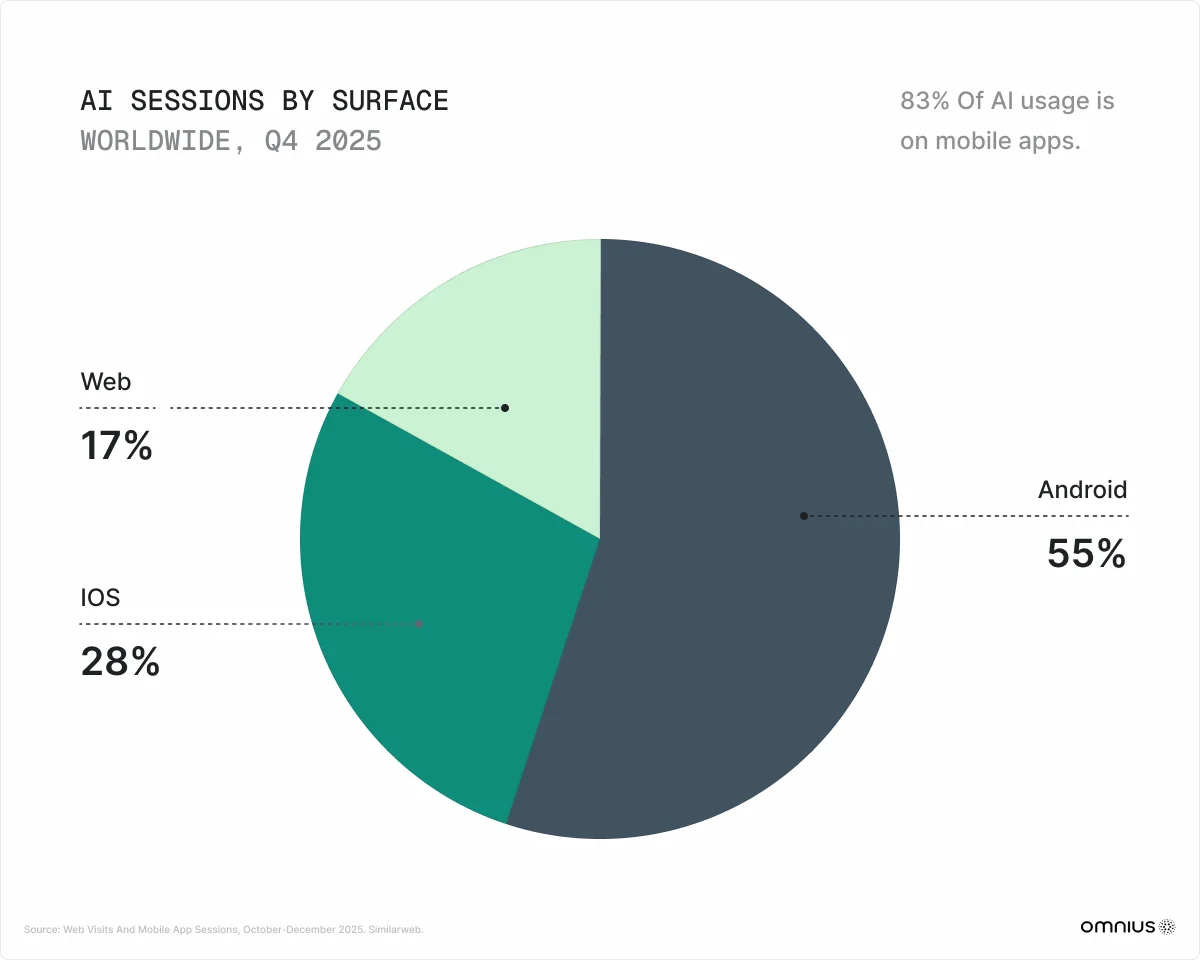

3. AI Search is a Mobile-First Phenomenon

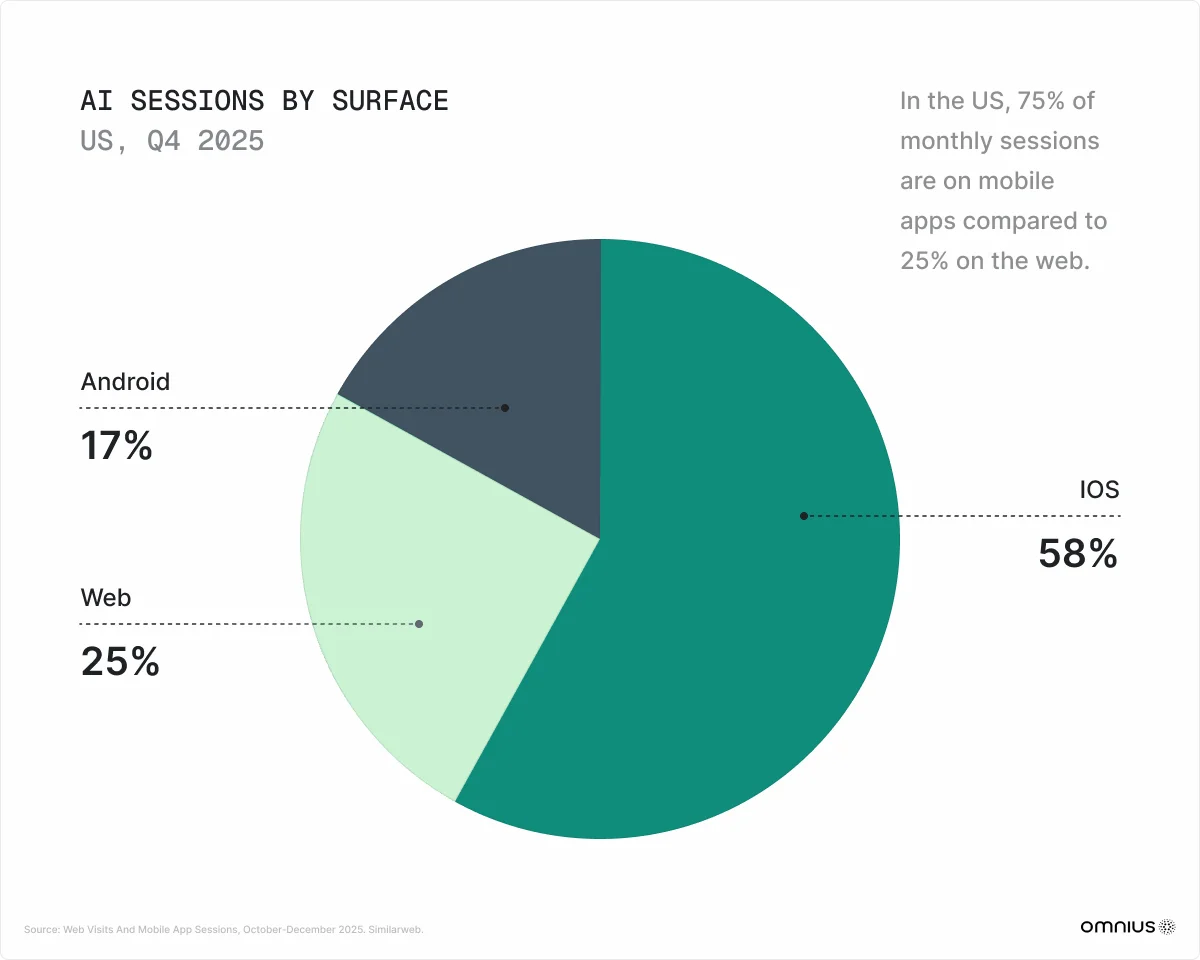

The discovery that 83% of all AI interactions occur on mobile apps, not desktop browsers, fundamentally changes what GEO means in practice. The geographic split is revealing. Globally, Android’s 55% share reflects AI adoption being driven by Android-dominant emerging markets.

In the United States, the split is 75% mobile, with iOS accounting for 58% and Android 17% of total US AI sessions.

Both geographies confirm the same strategic imperative: if your GEO process uses desktop browser testing, you are designing for the minority use case.

The explosive growth from mid-2024 onward is almost entirely iOS-driven. This coincides with ChatGPT’s integration into iOS features and the broader normalization of AI assistants on Apple devices.

This has three immediate implications for brand strategy:

- Brand content optimized for AI must be tested on mobile screen sizes and interaction patterns, not desktop.

- Consumer AI journeys are happening in-the-moment, on smartphones, often during consideration phases that historically belonged to mobile Google Search.

- The 4x to 5x underestimation in previous AI traffic reports means marketing investments based on web-only data were systematically mispriced against the actual consumer opportunity.

4. How People Actually Use AI (Type of queries that dominate)

Not all prompts are searches - understanding the distinction is critical for GEO investment

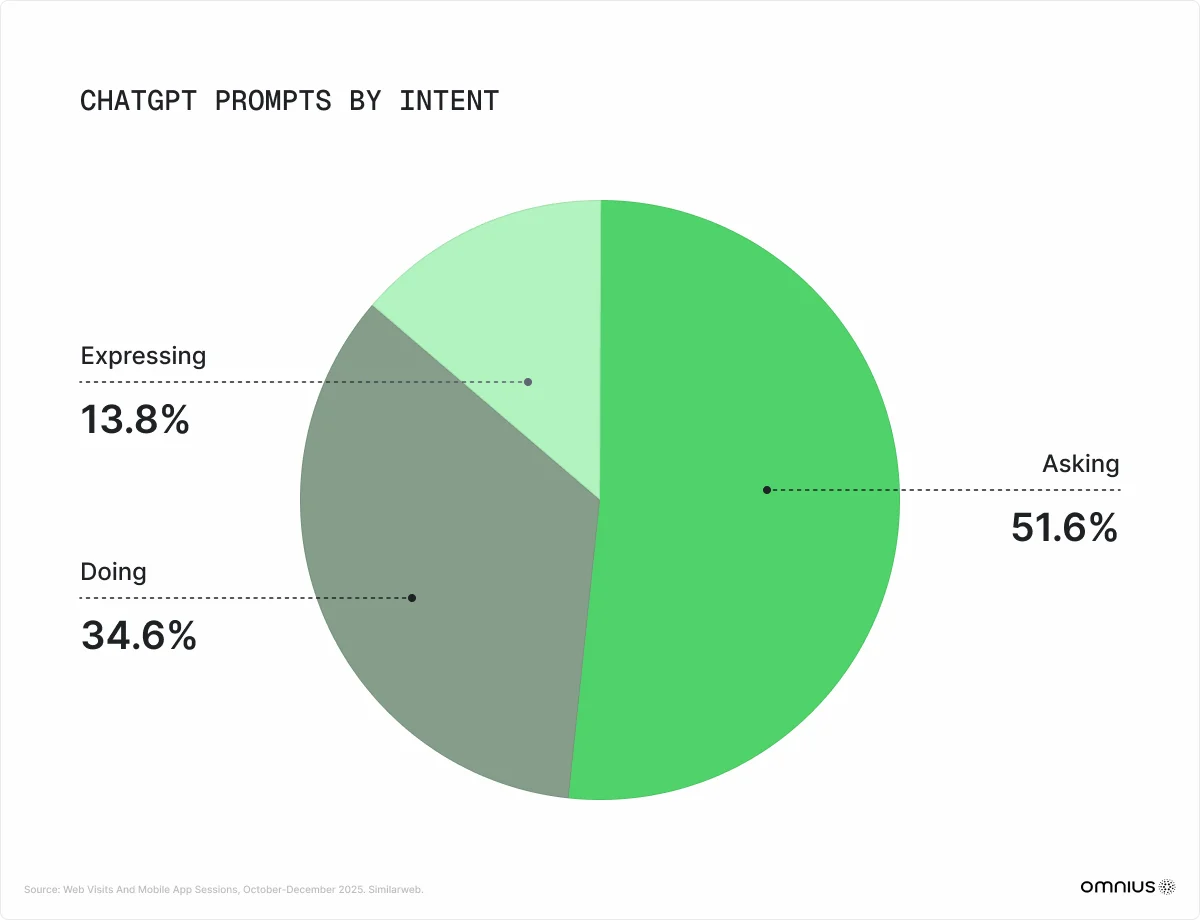

A Harvard/OpenAI study of over one million ChatGPT prompts provides us with a critical segmentation framework. The research classifies prompts into three intent categories:

- Asking (51.6%) - Information-seeking directly comparable to search: “What factors should I consider when choosing a CRM?”

- Doing (34.6%) - Task completion: drafting emails, writing code, creating documents. Not a search substitute.

- Expressing (13.8%) - Conversational statements with no information-seeking intent.

This segmentation matters enormously for how businesses should think about GEO investment. The Asking queries are where brand visibility, product comparisons, category education, and purchase recommendations occur, the entire consumer decision journey as it existed on Google, now happening inside AI interfaces.

Key insight: When adjusted for Asking-only prompts, ChatGPT accounts for 20% of global search-equivalent traffic and 12% in the US. The true addressable GEO opportunity sits precisely in this Asking segment.

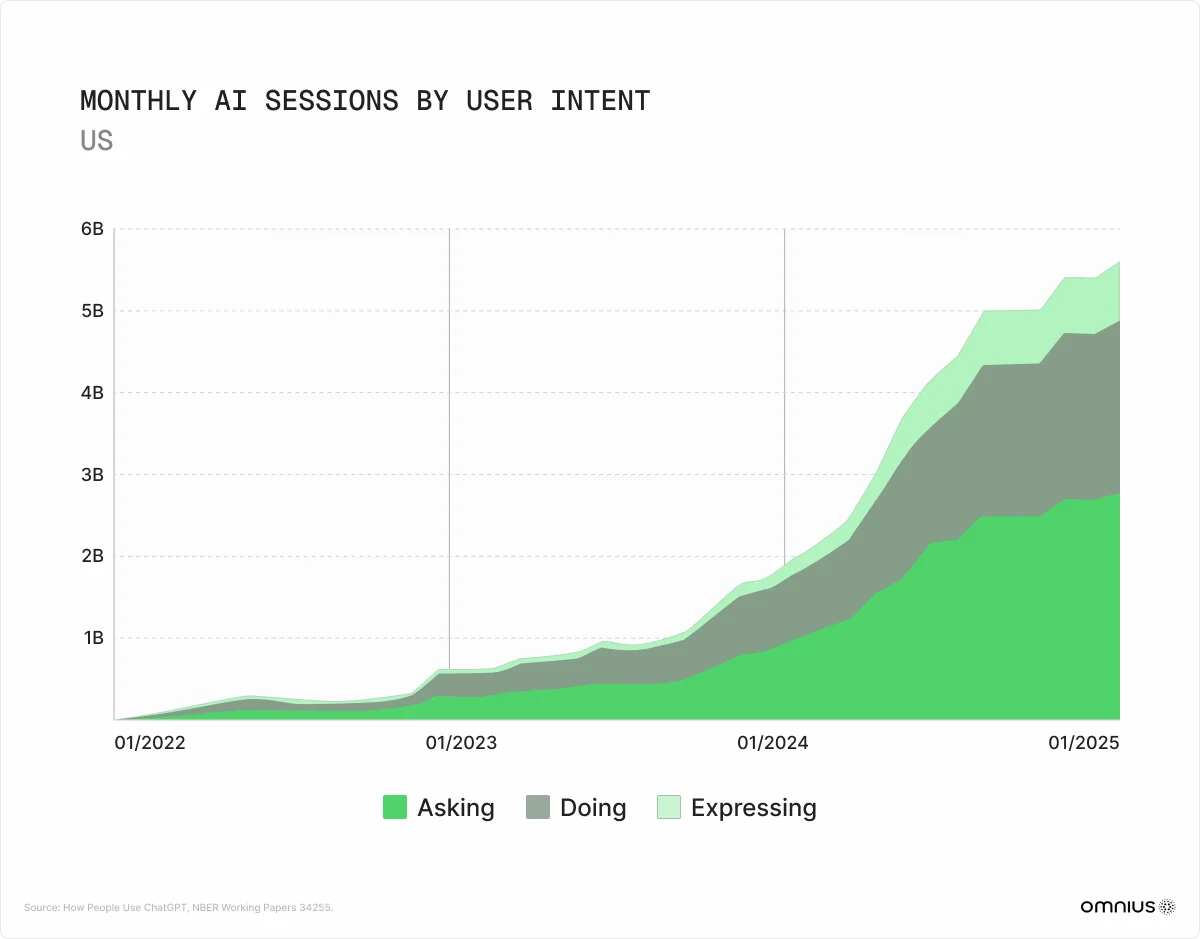

Even taking only the Asking segment, the US market is heading toward approximately 2.5 billion search-equivalent AI sessions per month, a market that did not exist three years ago.

Query Intent: How AI Overviews Are Expanding Across the Funnel

In January 2025, AI Overviews were overwhelmingly an informational-query phenomenon. By October 2025, the picture had changed dramatically:

Source: Semrush AI Overviews Study, 10M+ keywords, Jan–Oct 2025

The rise in navigational queries is the most alarming finding for brand marketers. A 1,296% increase in branded query AIO triggers means that users searching specifically for your company or product name are increasingly receiving an AI-generated summary rather than seeing your website at the top of results. This is a fundamentally new type of brand equity threat to your website that did not exist 18 months ago.

Long-tail queries of 8+ words trigger AI Overviews 57% of the time. Shorter, high-volume head terms remain more protected, but this window is narrowing as Google expands AIO coverage through 2026.

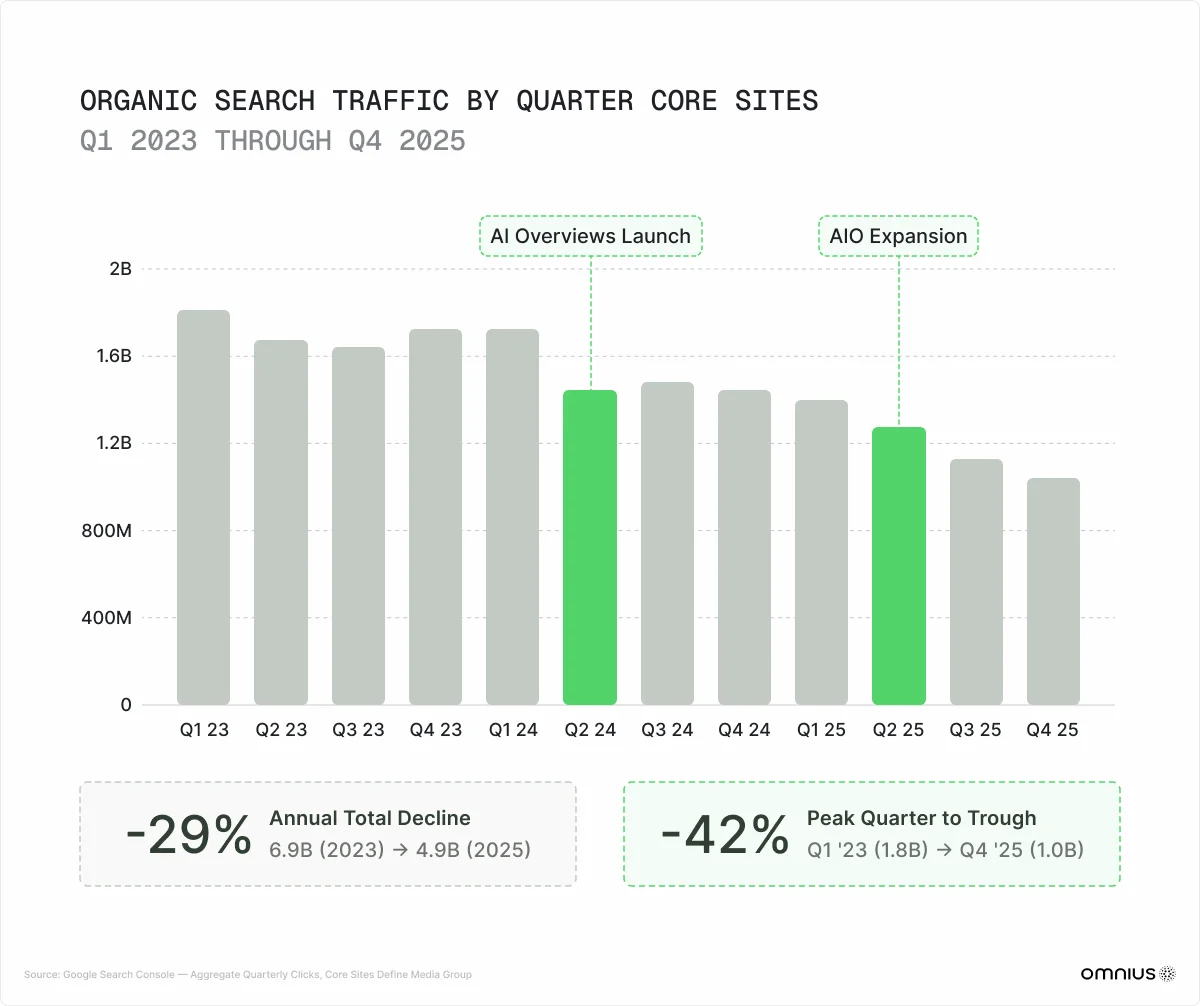

5. The Publisher Traffic Crisis

A 42% organic decline is already on record, and it’s accelerating

While AI search adds sessions to the total discovery market, its impact on organic web traffic is severe, measurable, and accelerating. Define Media Group, tracking a 64-site portfolio through Google Search Console, recorded a 42% decline in organic search clicks from the pre-AI Overview average to Q4 2025. Separately, Chartbeat data shows:

- Google Search referrals fell 60% for small publishers (under 10,000 daily pageviews)

- Medium publishers (10K–100K daily pageviews) saw a 47% decline

- Even large publishers (100K+ pageviews) experienced a 22% drop

- AI chatbots, despite all the growth, still account for less than 1% of all publisher referrals

The quarterly trajectory is critical reading for any business whose brand relies on organic search.

Two distinct shock events are visible.

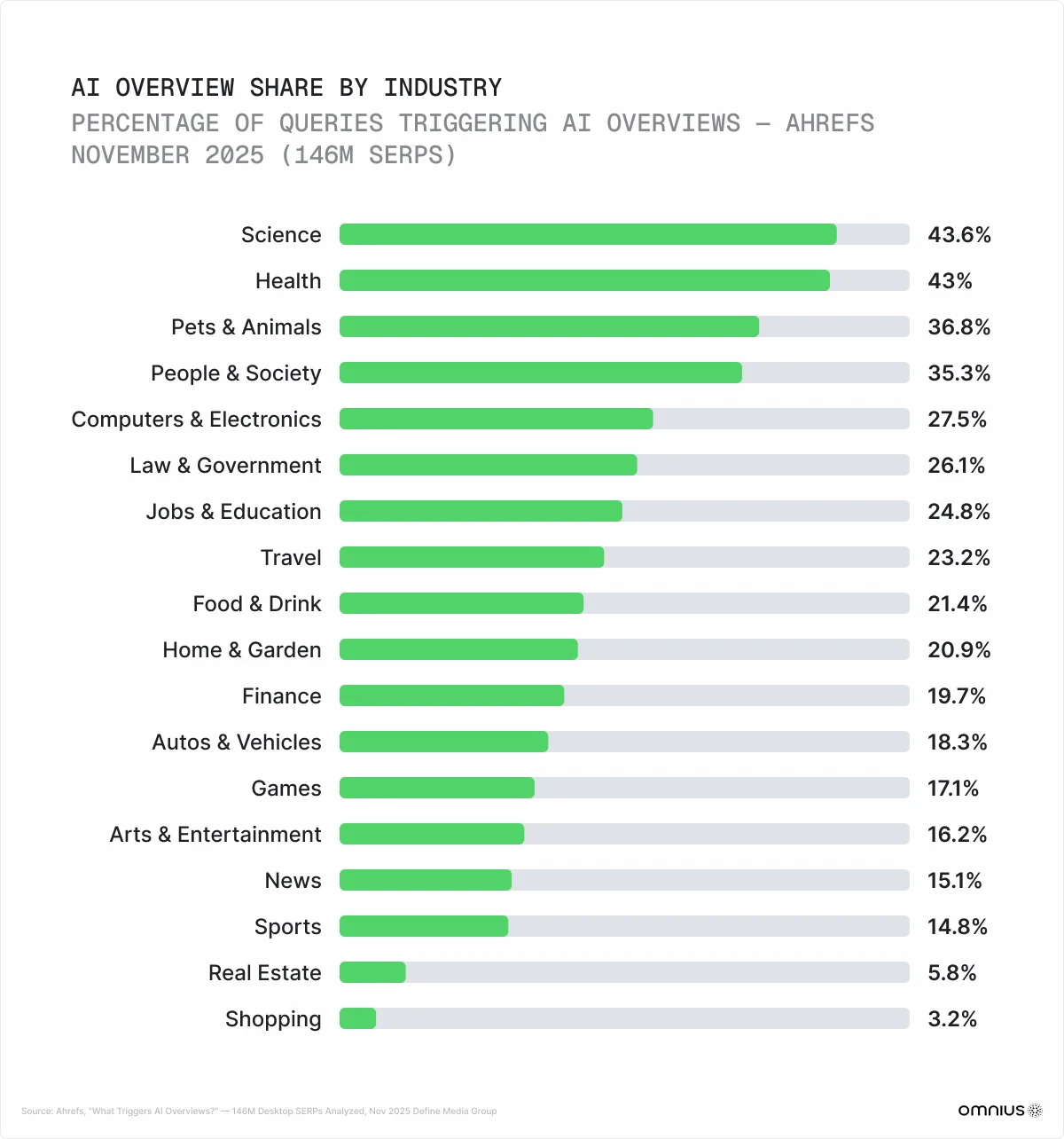

This is not a temporary adjustment, it is a permanent structural change to how Google routes traffic, and it's happening through different industries. The industry breakdown here provides essential nuance for brand planning.

Google deploys AI Overviews most aggressively where informational queries dominate: Science, Health, Pets, People and Society. Shopping (3.2% AIO penetration) and Real Estate (5.8%) are currently protected by Google’s commercial interest in maintaining click-through to paid listings.

With computers & electronics at 27.5% and Finance at 19.7%, it's definitely worth optimizing pages for AI Overviews.

However, with AI Mode explicitly designed to handle product recommendations across all keyword types, this protection is unlikely to persist beyond 2026.

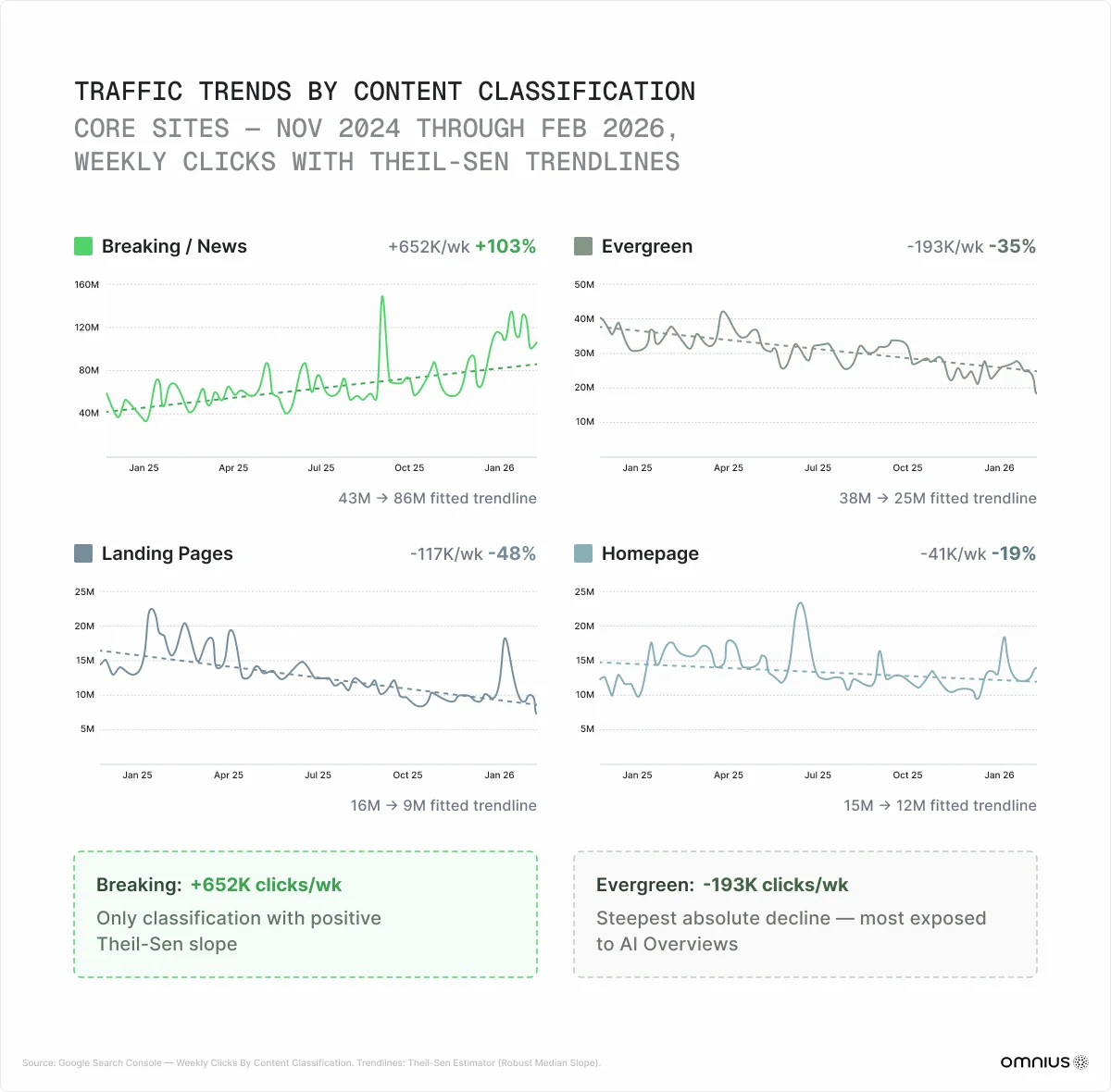

Here’s what these insightful statistics show us:

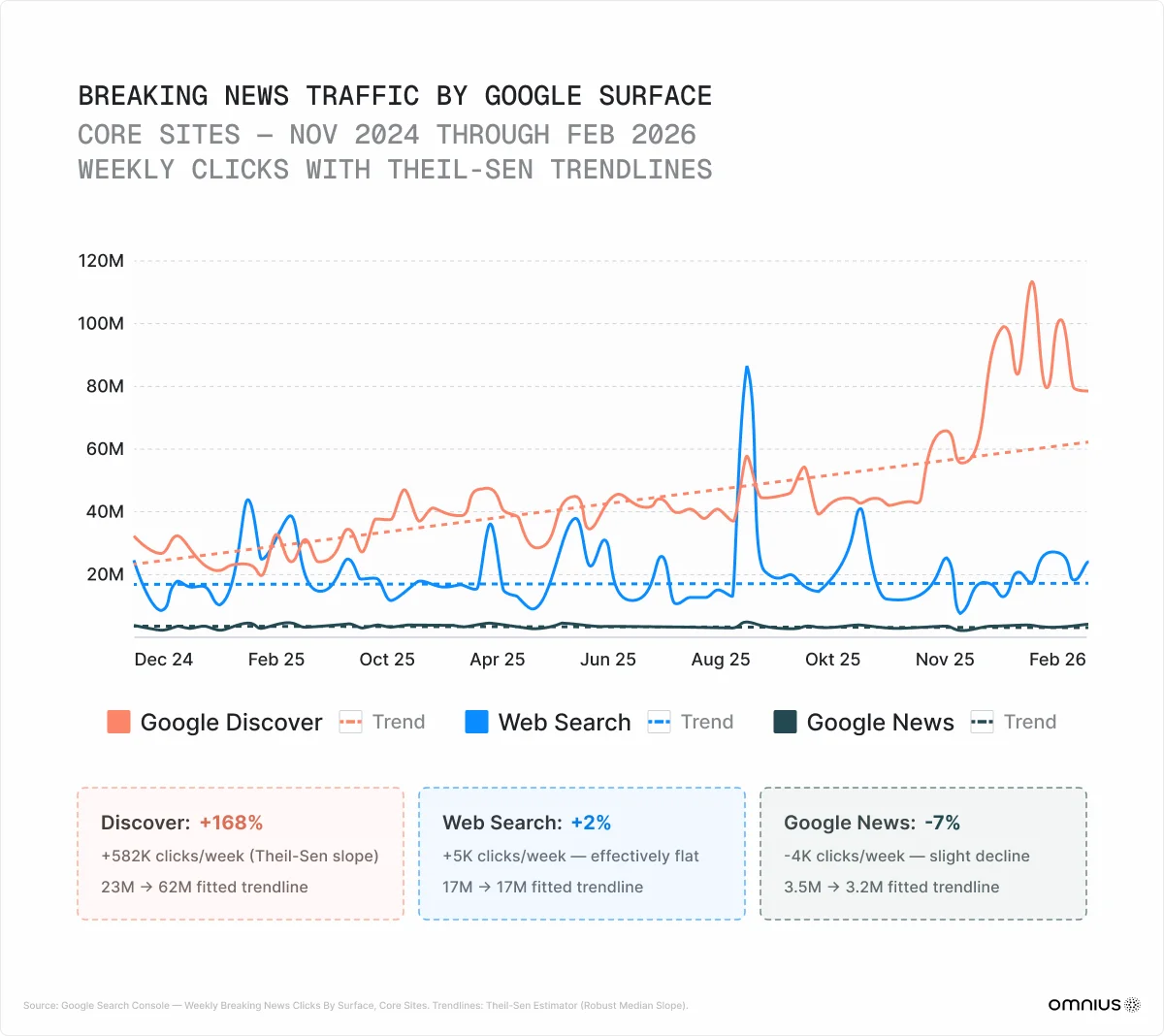

- Breaking News (+103%) is the sole content type with a positive trend.

- Evergreen decreased by −35%,

- Landing Pages decreased by −48%,

- Homepage decreased by −19%.

All but Breaking/News declined. This is the most actionable finding for content strategy teams.

Evergreen content, the backbone of most brand content strategies, is being systematically absorbed by AI Overviews. Breaking news, by contrast, cannot be pre-answered: it requires real-time sourcing and human editorial judgment that AI cannot replicate at speed.

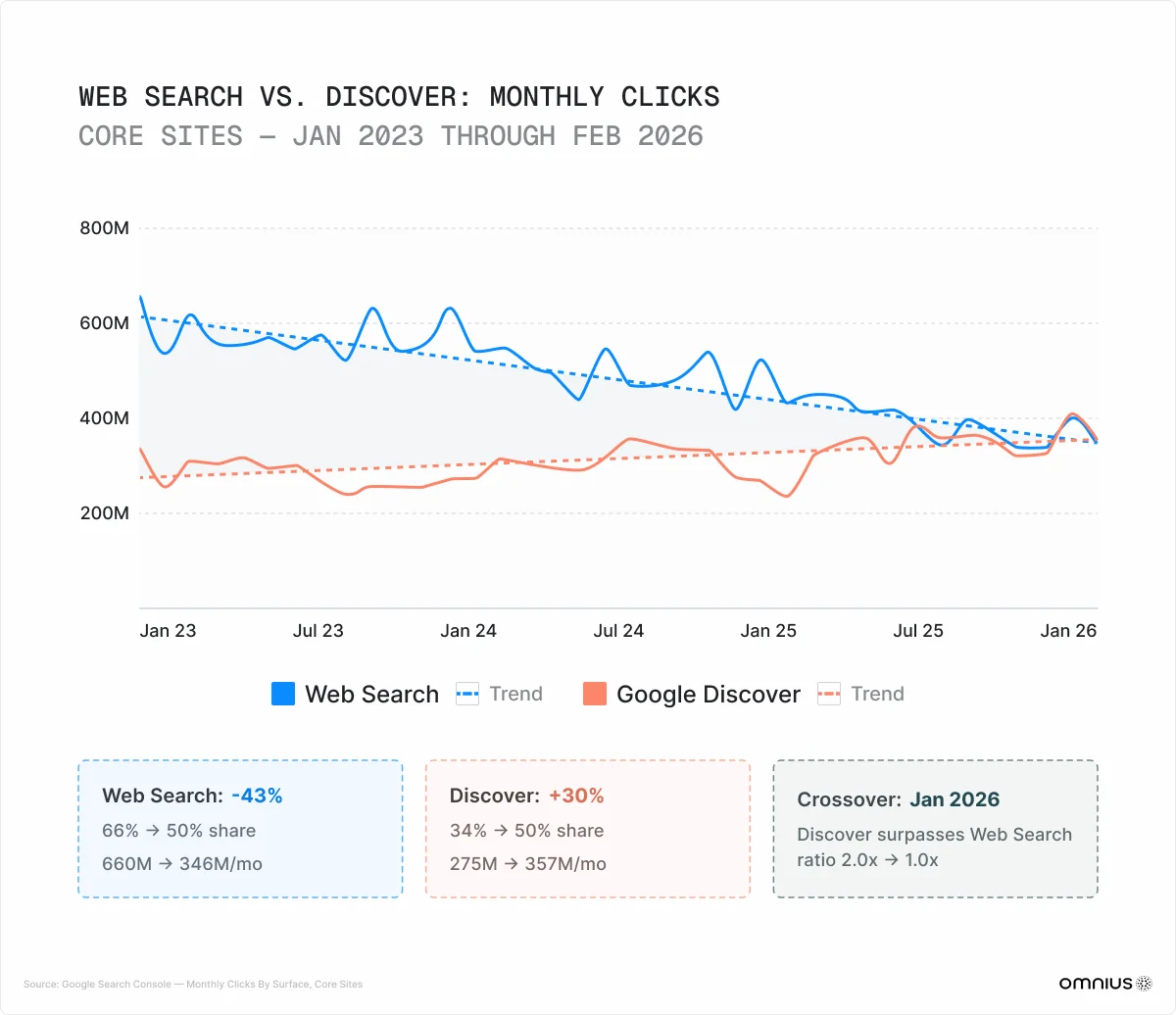

For the first time, January 2026 marked the first time Google Discover delivered more traffic to publishers than Google Web Search.

New stats are these:

- Web Search fell 43% (660M to 346M)

- Discover grew 30% (275M to 357M).

This crossover represents a profound shift in how Google routes users, from reactive (user-initiated queries) to proactive (algorithmically surfaced content).

Google Discover operates on a completely different algorithmic logic, as it rewards:

- recency,

- engagement signals,

- strong imagery, and

- topical consistency over keyword optimization and backlink authority.

Key insight: Google Discover is now equal to Google Search as a traffic channel for publishers, yet most brand content and SEO teams have no dedicated Discover optimization strategy. This represents an immediate, underexploited opportunity.

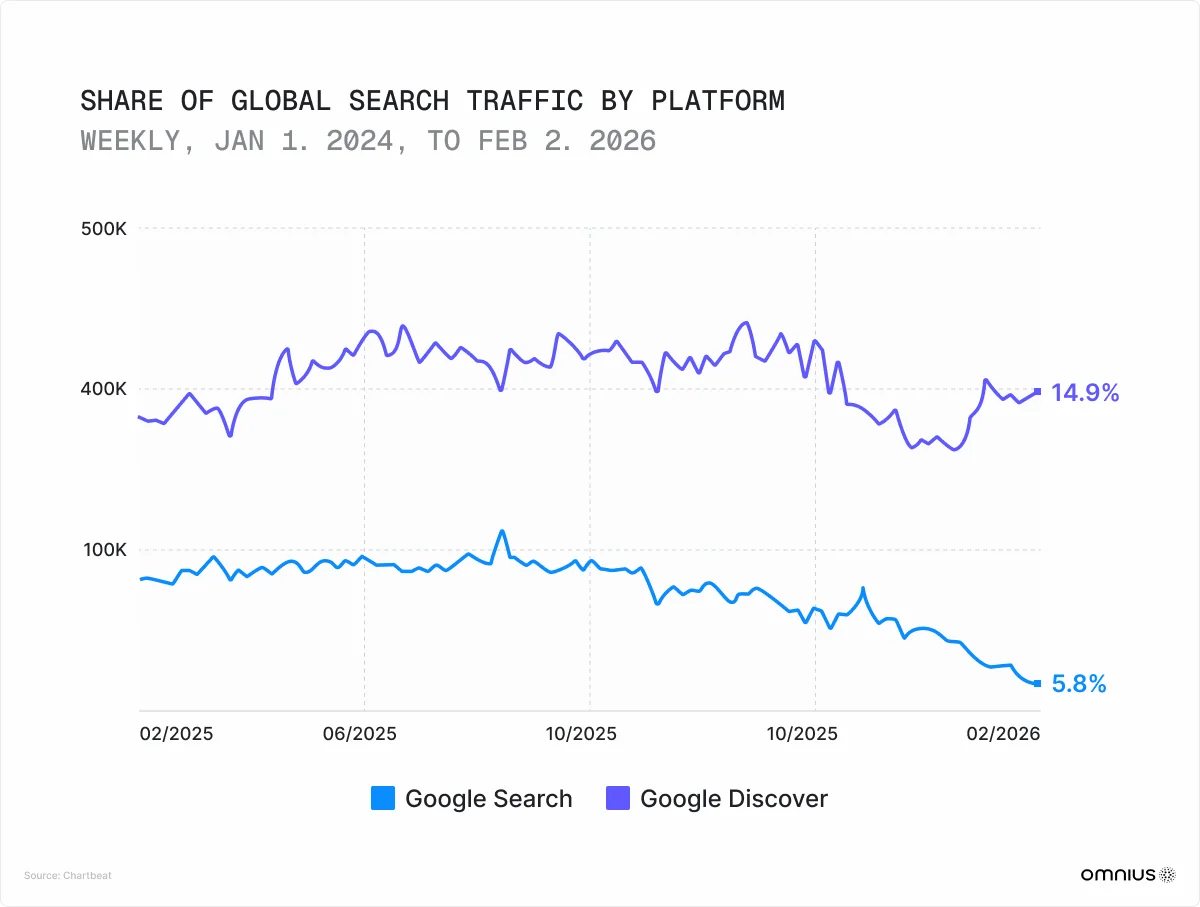

According to Chartbeat, Google Search’s referral share has nearly halved from ~9% to 5.8% in 14 months. Google Discover holds stable at 14.9%, now more than 2.5x larger than Search as a referral source.

The 2.5x gap between Discover (14.9%) and Search (5.8%) as referral traffic sources should fundamentally reorder editorial and content investment priorities.

Businesses still allocating the majority of their Google optimization budget to Web Search keyword targeting only are optimizing for the smaller and flatter channel.

And for the ones who started working on optimizing for AI visibility, it’s worth knowing 2 things:

1. The more niche a category, the easier it is to show up in the AI response brand list (and, conversely, broader categories mean higher difficulty)

2. The simpler the prompt, the more likely it will be that a few brands dominate the results (and, conversely, the more nuanced the prompt, the more brands appear, and the more "random" the results)

6. Search is Everywhere (Most Frequent Citations Across AI Platforms)

The Google vs. ChatGPT binary misses 80% of where discovery actually happens

Understanding which domains and source types are cited by AI platforms is not an academic exercise. It is the operational intelligence that determines where you must invest your third-party content strategy.

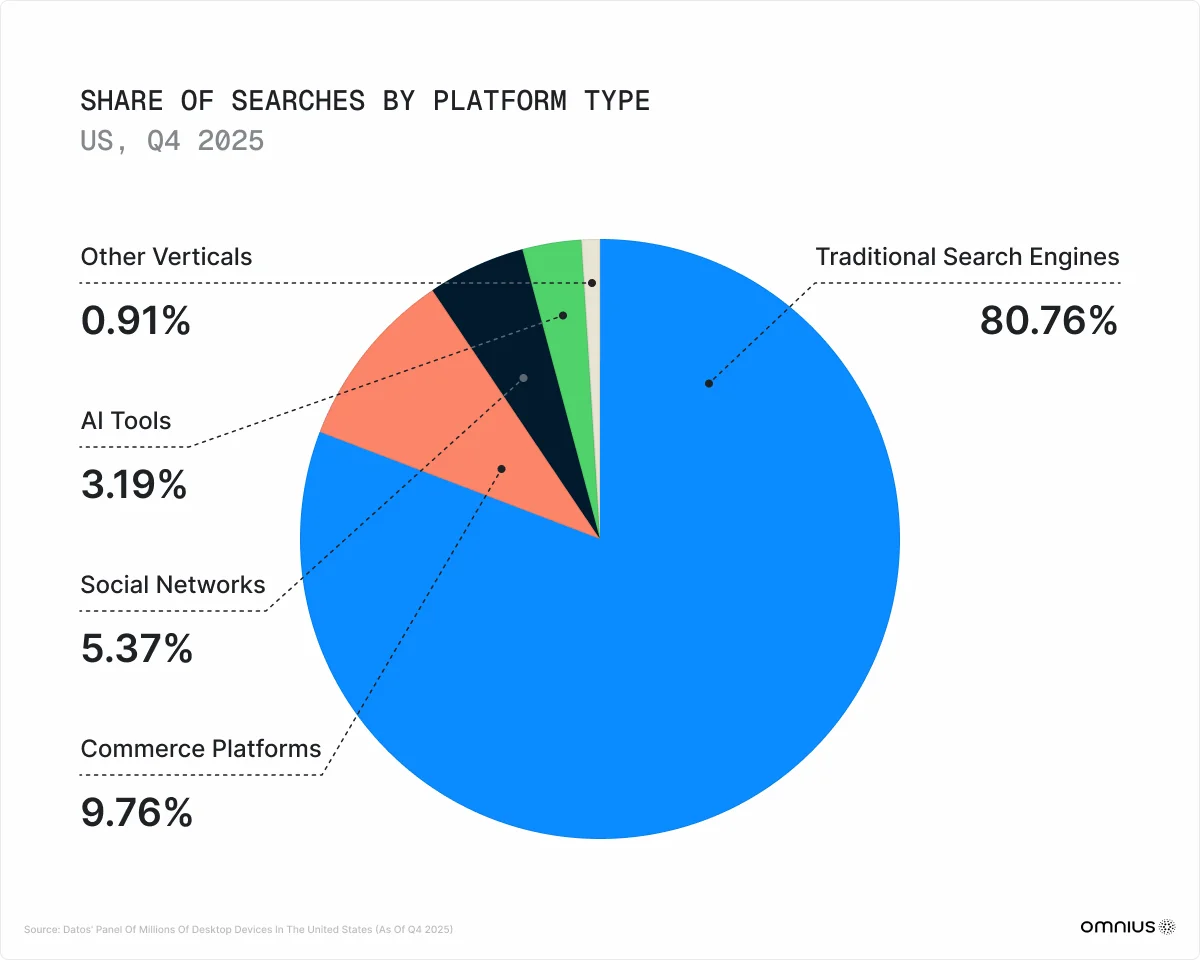

Research by SparkToro and Datos (a SemRush company), analyzing 41 major domains via desktop clickstream data, found that across those 41 sites, Google accounts for 73.7% of desktop searches - not the 90+% cited by narrower methodologies.

More significantly, Amazon (7.83%), Bing (4.31%), and YouTube (3.65%) each individually outpace ChatGPT’s 2.86% desktop search share.

Traditional search engines (80.76%) dominate, but commerce platforms (9.76%), social networks (5.37%), and AI tools (3.19%) are all meaningful discovery surfaces.

The 9.76% of desktop searches happening on commerce platforms, predominantly Amazon, represents more search activity than all AI tools combined.

A consumer searching for “best wireless headphones under $200” on Amazon is performing a purchase-intent query as relevant to brand strategy as the same query on Google.

The discovery, research, and comparison processes that precede a purchase decision are distributed across the entire web ecosystem, not concentrated in a single box on a Google SERP or a ChatGPT conversation.

For every visitor arriving at your owned website, hundreds are encountering your brand on Social (25.51%), Commerce (11.53%), News (8.25%), and other platforms outside your control.

This is the foundation of the Search Everywhere Optimization argument.

According to McKinsey, 44% of AI-powered search users say it’s their primary and preferred source of insight, topping traditional search (31%), retailer or brand websites (9%), and review sites (6%).

It is also worth noting a critical nuance: only 56% of ChatGPT visitors actually enter a prompt. The remaining 44% are passive, viewing shared conversations without inputting queries.

This means genuine search-equivalent engagement with ChatGPT is lower than raw visit counts imply, further strengthening the case for a diversified, multi-platform visibility strategy.

The second-tier story - Amazon, Bing, and YouTube is where a meaningful GEO diversification opportunity exists.

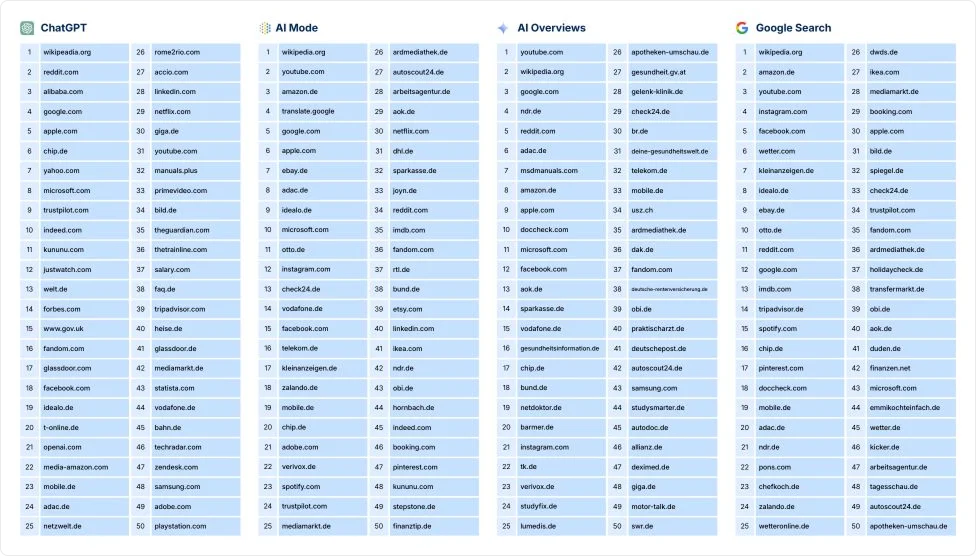

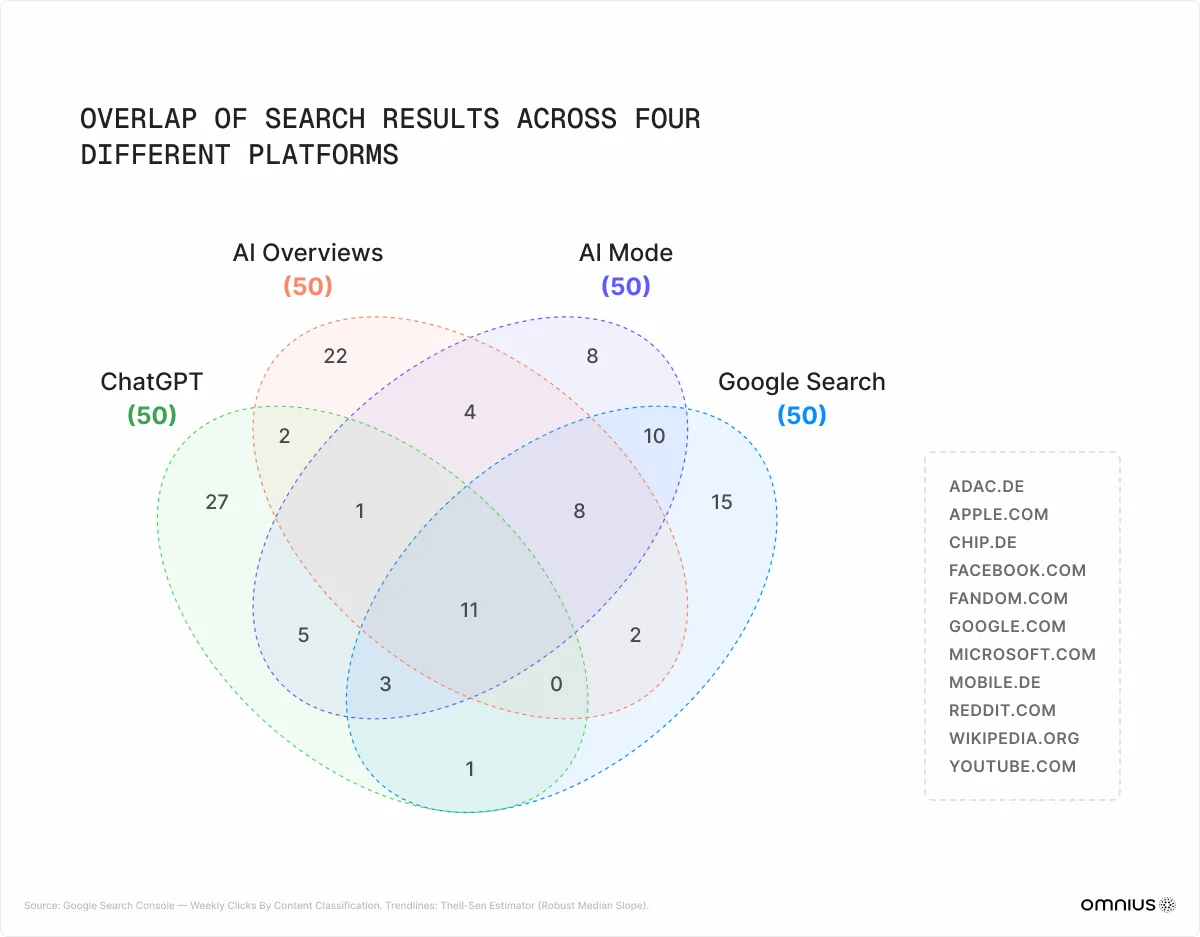

Platform-Level Citation Preferences: A Structural Comparison

The data below synthesizes three major citation studies covering 680M+ citations (OtterlyAI / Tryprofound), 78.6M searches (Ahrefs Brand Radar, June 2025), and 230,000+ prompts tracked weekly over 13 weeks (SemRush, Oct 2025).

The single most important finding in citation research: only 11% of domains are cited by both ChatGPT and Perplexity. Each AI platform operates as an independent citation ecosystem. A brand that is cited by Google AI Overviews has no statistical guarantee of being cited by ChatGPT, and vice versa.

Sources: OtterlyAI 1M+ citations 2025–26; Ahrefs Brand Radar 78.6M searches Jun 2025; Semrush 230K+ prompts Oct 2025; Tinuiti Q1 2026 AI Citation Trends Report

The Reddit Collapse and Resurgence Story

One of the most instructive episodes in citation research: in September 2025, ChatGPT's citation of Reddit collapsed from approximately 60% of responses to around 10% within weeks. The cause correlates with Google removing its num=100 search parameter, limiting how tools access deeper search results where Reddit typically appears. By January 2026, Reddit's citation share had grown at least 73% across all AI platforms from its October 2025 trough, and for Perplexity, 24% of all January citations came from Reddit alone.

The lesson is not that Reddit is reliable or unreliable. The lesson is that AI citation patterns are volatile, platform-specific, and can shift significantly within weeks based on infrastructure changes outside any brand's control.

Citation monitoring is not a quarterly activity - it must be continuous.

What AI Actually Prefers to Cite: Content Signals

Beyond domain-level analysis, research reveals specific content characteristics that increase citation probability across platforms:

- Statistics and data points increase AI visibility by 22% (The Digital Bloom / Princeton GEO research)

- Quotations and direct expert attribution boost visibility by 37% - AI systems prefer content with clear, citable voices

- 44.2% of all LLM citations come from the first 30% of content (the introduction) - lead with your most important claim, not a preamble (Growth Memo, Feb 2026)

- ChatGPT is 3.2x more likely to mention a brand than to cite it with a link - awareness without traffic is the default ChatGPT outcome

- Brand search volume is the strongest predictor of AI citation (0.334 correlation) - outweighing traditional backlink metrics

- 80% of sources cited in AI platforms do NOT appear in Google's top results - GEO and SEO require different source strategies

73% of B2B buyers now use AI tools in their research process, but platform preferences are sharply segmented: technical buyers gravitate to Perplexity (citation transparency), executives to ChatGPT (mainstream reach), and consumer researchers to Google AI Overviews (integrated search). Your citation strategy must account for all three audiences.

7. AI Overview Mechanics & the CTR Collapse

Understanding exactly how AI Overviews damage organic visibility

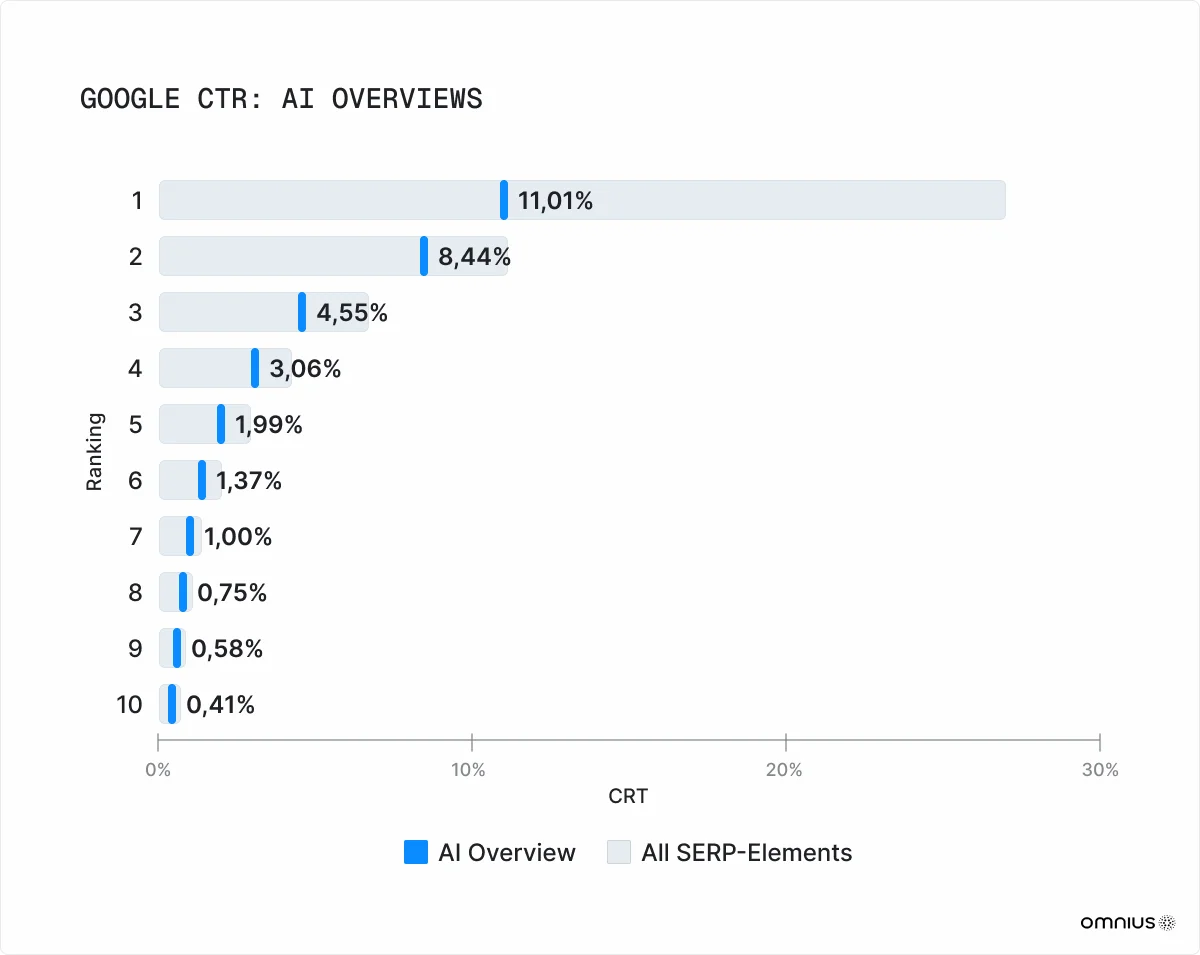

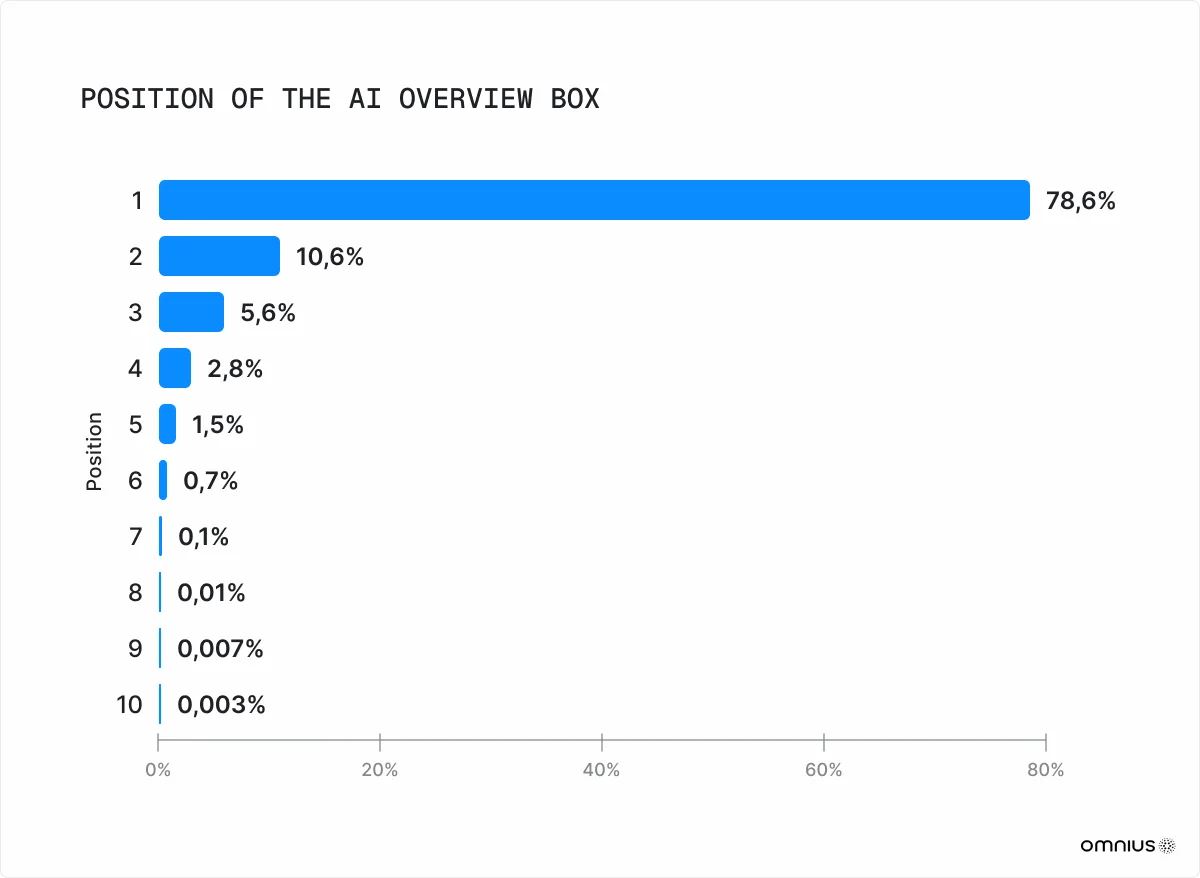

Google’s AI Overviews are not evenly distributed. SISTRIX analysis shows that 78.6% of AIOs appear at Position 1 - directly displacing the single most valuable organic real estate on the internet. When an AIO is present:

- Position 1 click-through rate falls from approximately 27% to just 11%, a reduction of nearly 60%.

- Position 2 drops to 8.44%.

- Position 10 to just 0.41%.

This defines the new organic economics of Google Search. Achieving the top organic ranking is now worth roughly the same as achieving Position 3 or 4 in a pre-AIO SERP. The traditional SEO goal of “ranking number one” has been fundamentally devalued.

The new goal: either earn citation inside the AIO, or optimize for transactional and breaking-news query types that remain AIO-free.

78.6% appear at Position 1, 10.6% at Position 2 - making AIO dominance of the search result page near-total.

This confirms the scale of SERP real estate displacement. With nearly 79% of AIOs occupying the first visible position, the practical implication for brands is that appearing in an AIO citation is now more valuable than achieving a traditional Position 1 organic ranking.

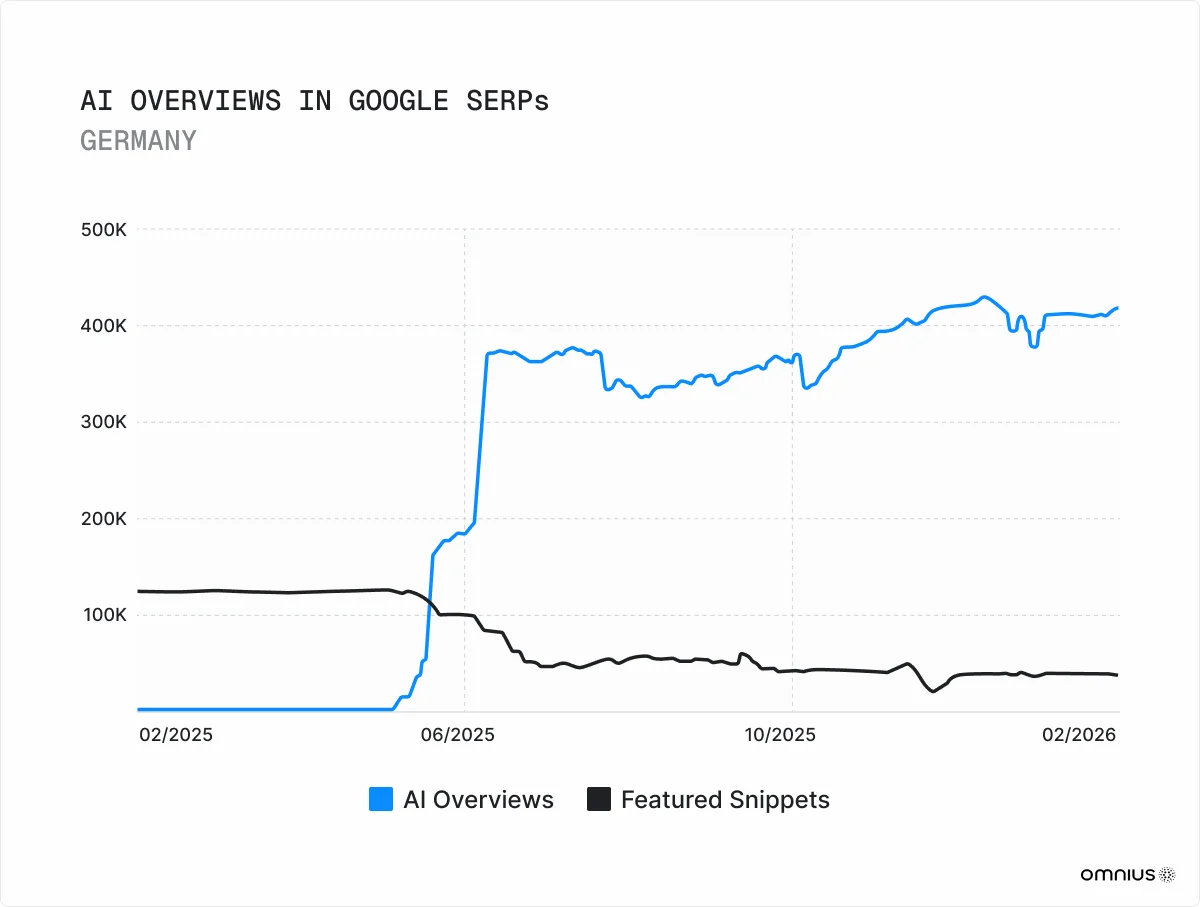

The German market data offers a preview of what is coming to every market where AIOs roll out. Featured snippets, which themselves were controversial for enabling zero-click searches, are now being wholesale replaced by a far more comprehensive AI-generated summary. The speed of this replacement (near-zero to 400,000 queries in approximately eight weeks) illustrates how rapidly Google can redraw the SERP landscape.

Given Google’s ability to surface Gemini at every touchpoint, Chrome, Android, Google Search, Gmail, Workspace - this trajectory is structurally different from any other challenger’s growth curve.

AI Search vs. Google: A Data Comparison

The most nuanced story in search data is not a competition, it is a division of labor. 98% of ChatGPT users still also use Google. But the types of queries allocated to each platform are diverging rapidly, creating a two-platform optimization imperative for every brand.

Volume: Where Each Platform Stands

Sources: Graphite/Similarweb, SparkToro/Datos, Am I Cited, Perplexity investor data, Q4 2025 / Q1 2026

The Query Type Division of Labor

Users do not experience Google and AI as competitors. Instead, they allocate different query types to each based on utility:

- Google-preferred queries: Quick navigational searches ("Facebook login"), simple factual lookups ("weather tomorrow"), local transactional intent ("pharmacy near me open now"), and one-tap brand navigations

- AI-preferred queries: Complex multi-part research ("explain the tradeoffs between React and Vue for a B2B SaaS product"), planning tasks ("help me plan a 10-day Japan itinerary"), synthesis requests ("summarize the five most important things to know about AI search for a Fintech business"), and comparison-heavy evaluation ("what are the best project management tools for a 50-person agency")

- Emerging AI-preferred territory: Product comparison, brand evaluation, vendor shortlisting - exactly the commercial middle-of-funnel that marketers value most

The most commercially significant shift is AI's intrusion into commercial middle-funnel queries. When B2B buyers ask ChatGPT, "what are the best CRM tools for a mid-market SaaS company?" they are making vendor shortlisting decisions inside an AI interface. Being absent from that answer is equivalent to being absent from a shortlisting meeting.

Zero-Click Rates: A Platform-by-Platform Comparison

The zero-click data reframes where optimization effort should be directed.

Sources: Semrush Sept 2025; Pew Research Center Jul 2025; Exposure Ninja / Am I Cited 2026

ChatGPT and Perplexity are actually more generous traffic referrers than Google AI Mode. When a brand is cited by a standalone AI chatbot, users are more likely to click through to verify or explore. The traffic threat is more acute from Google's own AI features than from external AI platforms.

8. AI Overviews vs. AI Mode

Two distinct Google features with fundamentally different strategic implications for brands

As Google accelerates its AI search transformation, you must distinguish between two products that are often conflated: AI Overviews and AI Mode. Confusing the two leads to misaligned optimization strategies, misread traffic data, and missed opportunities.

Figure 26: AI Overviews vs. AI Mode - a comparison

Note the critical distinction for AI Mode: “Strong brand” is the decisive variable - not content structure or technical SEO alone.

The comparison above reveals a critically important strategic truth: the optimization logic for AI Overviews and AI Mode is fundamentally different.

AI Overviews are a content and structure problem. Brands that produce well-structured, E-E-A-T-compliant content on topics where AIOs appear can earn citation inside the summary. The playbook is demanding but learnable.

AI Mode is a brand equity problem. Google’s AI Mode rewards brands with genuine market authority: rich third-party coverage, strong consumer sentiment across review platforms, deep Wikipedia-level knowledge graph presence, and extensive topical expertise that AI can draw on from many independent sources. A technically excellent website for a brand without earned market authority will not rank in AI Mode.

Key Insight: Businesses face a two-front optimization challenge: technical content excellence for AIO citation, and brand authority building for AI Mode recommendation. The second is harder, slower, and more expensive, but it is the decisive battleground of AI search in 2026 and beyond.

Google has already announced that AI Mode is being integrated more prominently at every touchpoint: the homepage, the Chrome address bar, and directly following AI Overviews as a “go deeper” link.

Here’s an example of their VP of product post announcement:

When Google consolidates its fragmented AI products into a unified input experience, AI Mode will be the default for high-intent queries, and brand authority will be the primary ranking signal.

The SEO/GEO Marketing Shift

AI search is not merely changing where consumers discover brands. It is restructuring the fundamental economics of customer acquisition, channel allocation, and conversion. The data below documents a shift that should immediately alter how you build 2026 and 2027 marketing budgets for your business.

AI Search Converts at 5–23x the Rate of Google Organic

The most commercially significant data point in AI search research: traffic arriving from AI platforms converts at 12–16% on average, compared to Google organic's 2.8% conversion rate. By AI platform:

Source: Superprompt / analysis across 12M+ website visits, 350+ businesses, 2025

The reason for this conversion premium is not an algorithmic accident. AI search users are completing the consideration phase inside the AI interface before they ever click through. When they arrive at your website, they are already informed, already partially convinced, and ready to act. The AI has functioned as a high-quality pre-sales consultant at zero marginal cost to the brand.

Customer lifetime value compounds the advantage: AI-sourced customers generate an average CLV of $1,847 vs $1,106 from Google organic - a 67% improvement. First-session conversion occurs in 73% of AI-traffic visitors, compared to just 23% from Google organic.

The CAC Inversion: Why Paid Search Economics Are Breaking

While AI search delivers superior conversion economics, traditional paid channels are deteriorating simultaneously:

- Overall CAC has surged 222% over eight years, driven by channel saturation, privacy regulation, and diminishing marginal returns from paid targeting

- Google Ads CPL reached $70.11 in 2025 (up 5.13% YoY), and the average B2B paid search CAC is $802 per customer (WordStream / Data-Mania)

- GEO delivers an average CAC of $559 across industries, with 27% higher conversion rates and 9.2% higher lead quality than traditional SEO

- B2B SaaS GEO CAC is as low as $249, which is the most efficient acquisition channel available for technical products with well-structured content

→ The implication is a structural reallocation signal: organic and AI-optimized channels are demonstrably outperforming paid channels on both acquisition cost and lead quality. Businesses that shift budget toward GEO now will compound that advantage as AI traffic volumes grow.

The Shift to Organic & AI Channels

The convergence of rising paid CAC and superior AI search conversion is accelerating a channel mix realignment that will define marketing budgets through 2028:

- 79% of B2B buyers expect to use AI-enhanced search within the next year; 70% already have some trust in generative AI search results (Marketri)

- 29% of B2B buyers now start research via AI tools more often than Google; this figure is accelerating

- 25.7% of marketers now plan to develop content specifically for AI citations (Exposure Ninja); only 22% are actively tracking AI visibility today

The channel logic is shifting from "rank and drive traffic" to "earn citation and capture informed intent." A brand that is mentioned favorably by ChatGPT in response to a purchase-relevant query is achieving a form of always-on, personalized, pre-qualified lead generation that no paid media format can replicate at equivalent economics.

Zero-Click Economics: The Visibility-Without-Traffic Model

A critical nuance in AI search economics is that brand value is being created even when no click occurs. 93% of Google AI Mode searches, and 43% of AI Overview searches end without a click, yet the brand cited has influenced a consumer decision. This creates a new metric imperative:

- AI Share of Voice (frequency of brand mention in relevant AI answers) becomes more important than click-based traffic metrics

- Branded search lift (increase in direct brand search following AI mention) is the primary proxy indicator that AI is driving awareness

- Direct traffic analysis (AI-influenced visits often appear as "direct" in GA4) needs to be re-attributed using AI traffic fingerprinting

- Conversion rate and CLV by channel must be tracked at the AI source level to demonstrate the outsized return on GEO investment

"For every visitor to your site, hundreds will get to know your brand on platforms you don’t control. The discovery, research, and comparison processes are happening there." — Rand Fishkin, SparkToro

9. The Business's Action Steps

Four moves to build a competitive advantage in AI search

The data converges on a clear conclusion: AI search is not a future consideration. The $750 billion in US revenue projected to flow through AI-powered search by 2028 is being pre-distributed to brands that act now. Only 16% of brands currently track AI search performance systematically, meaning the competitive window for first-mover advantage remains open, but it will not stay open long.

1. Diagnose Before You Invest

Conduct a rigorous GEO diagnostic across ChatGPT, Google AI Overview, Google AI Mode, Gemini, and Perplexity. Benchmark your share of voice in AI answers against competitors and against your own traditional SEO performance. Most industry leaders are already 20 to 50% behind their own SEO performance on GEO. Establish this baseline before allocating budget.

2. Rethink Your Source Ecosystem

Your brand website represents only 5 to 10% of the sources AI platforms use to generate answers about your category. In CPG and financial services, over 65% of AI answer sources are third-party publishers, UGC platforms, and affiliate sites. Map which sources AI models actually cite for your category, then build an influence strategy through PR, expert placements, community seeding, and partnership content.

3. Restructure Content for AI Legibility and Discover

Deploy a dual content strategy: reduce investment in commoditized evergreen content (most vulnerable to AIO absorption) and redirect resources toward (a) structured, authoritative content designed to earn citation inside AI Overviews, and (b) breaking and timely content optimized for Google Discover, which is now an equal traffic channel to Web Search. Clear headings, expert attribution, original data, and semantic precision are the new ranking signals for AI citation.

4. Build GEO as a Standing Capability, Not a Project

GEO requires ongoing cross-functional investment spanning marketing, SEO, PR, and customer experience. Establish dedicated GEO KPIs, tracking infrastructure aligned to LLM update cycles, and a testing cadence. The AI search landscape is evolving monthly, a one-time optimization initiative will have a shelf life measured in weeks, not quarters.

“The best businesses have always sought to meet consumers where they are. Today, those consumers are increasingly using AI-powered search. Brands have no choice but to adjust to this new reality.” - McKinsey & Company, October 2025

Looking ahead, AI platforms will evolve from answer engines into autonomous agents, comparing brands, evaluating options, and potentially completing purchases on behalf of users without a human click. Brands with strong, accurate representation in AI training sources today will occupy default positions in that agentic future.

.png)

.svg)

.svg)